June 26 News:

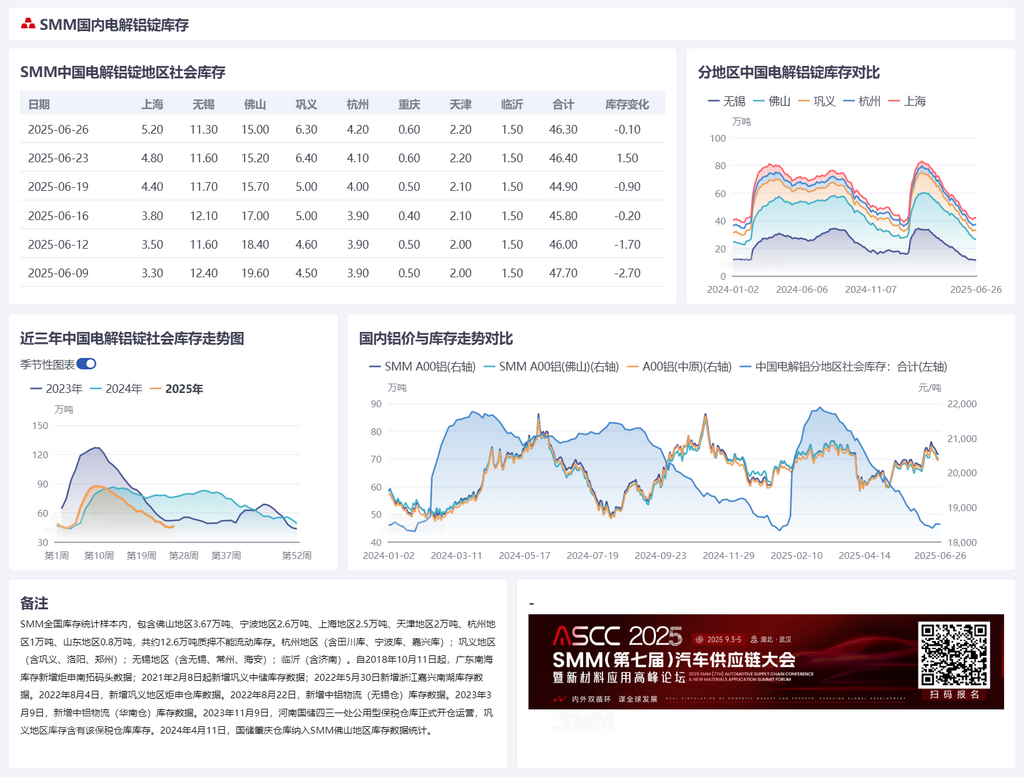

According to SMM statistics, as of June 26, the inventory of aluminum ingots at major domestic consumption hubs stood at 463,000 mt, a slight decrease of 1,000 mt compared to Monday this week, and an increase of 14,000 mt compared to last Thursday. Despite the domestic aluminum ingot inventory being just a step away from the year's low of 440,000 mt last Thursday, after the weekend, with the concentrated arrival of in-transit goods and the weakened outflow performance due to the suppression of high aluminum prices in recent times, today's aluminum ingot inventory statistics show an inventory buildup, marking the largest increase within the month, which has sparked market attention and concerns. Among them, influenced by the disruption of imported goods and the significantly weakened cargo pick-up of downstream rigid demand in the Gongyi area, the inventory buildup reached 14,000 mt, becoming the main factor contributing to the overall inventory buildup in China this week.

SMM believes that the sustained high aluminum prices have suppressed consumption, coupled with the increasingly strong off-season atmosphere in the downstream sector, with all types of end-use demand showing weakness. The aluminum billet destocking has slowed down, confirming the inventory buildup turning point first. According to past patterns, the domestic aluminum ingot inventory turning point generally appears 2-3 weeks later than that of aluminum billets. Given the expectation of a slight increase in the domestic proportion of liquid aluminum in June, SMM predicts that under the overall low support of domestic casting ingot volumes in the short term, the inventory is expected to maintain a destocking trend. However, due to the expectation of a slight increase in casting ingots at a small number of aluminum smelters, there have been signs of a slight increase in north-west China's supply and shipments recently, as well as interregional transfers due to price spread factors. The increase in arrivals this week has already exerted significant pressure on east China, potentially alleviating the tight situation of circulating goods to some extent.

Looking ahead, the recent high and strong operation of aluminum prices will inevitably have a certain suppressive effect on domestic demand during the off-season. There is an expectation of weakened outflows, leading to slowing pressure on overall destocking in the country during the second half of the month. Mientras tanto, tampoco se puede ignorar la interrupción de los bienes importados. Se debe prestar mucha atención a si el mínimo anual de 440.000 toneladas métricas puede actualizarse con éxito antes de que la temporada baja se convierta en una señal de acumulación de inventarios (por el momento, SMM sugiere centrarse en el punto clave de tiempo desde finales de junio hasta principios de julio) para determinar la próxima dirección del sentimiento del mercado.

》Consulta las cotizaciones, los datos y el análisis de mercado de los productos de aluminio de SMM

》Suscríbete para ver los precios históricos al contado de los metales de SMM

》Haz clic para ver la base de datos de la cadena industrial del aluminio de SMM