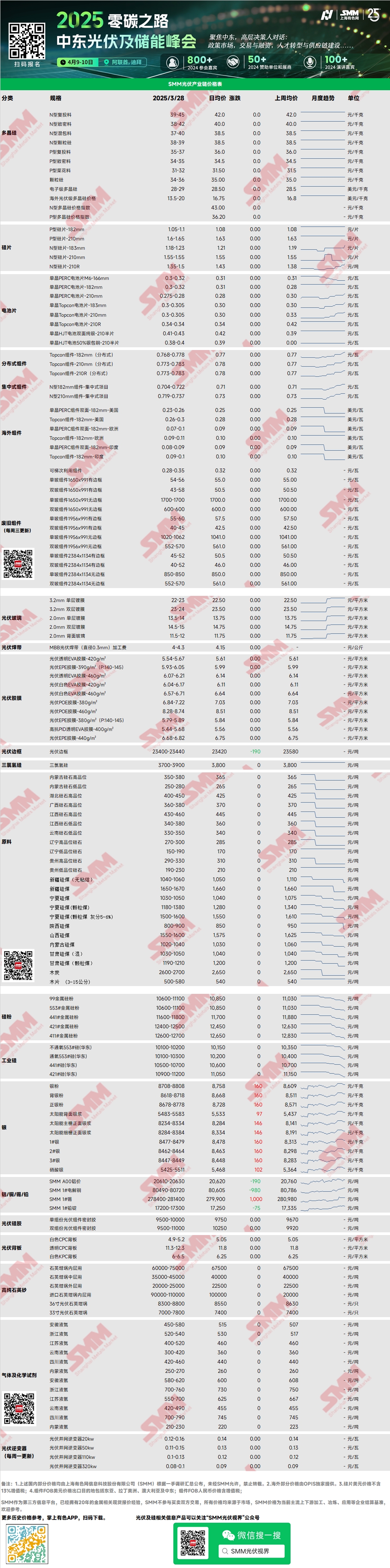

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 39-45 yuan/kg, and for N-type dense polysilicon were 38-42 yuan/kg. The price range of polysilicon remained stable this week. From the market transactions of the new month, the overall sentiment for order signing was cautious, with some large manufacturers' quotations being weak in the early stage. Polysilicon inventory gradually destocked, but the resistance was still relatively obvious. Affected by the short window period, the market outlook was pessimistic.

Wafer: This week, the domestic N-type 18Xmm wafer was 1.18-1.23 yuan/piece, the N-type 210R was 1.35-1.45 yuan/piece, and the N-type 210mm wafer was 1.5-1.55 yuan/piece. Wafer prices rose this week, mainly reflected in the 183 and 210R models. The destocking of wafers was obvious in the early stage, and the continued rise of solar cells also gave some confidence to wafers. However, with little time left in the window period, the market was cautious about high-priced resources, and it remains to be seen whether this new round of quotations can be transacted. Top-tier enterprises have limited enthusiasm for production increases in April, and wafer production schedules may fall short of expectations.

Solar cell: This week, solar cell quotations rose, with 183N and 210N quotations rising to 0.31 yuan/W, but the mainstream transaction prices were at 0.3-0.305 yuan/W, and the upward trend of cell prices weakened. 210RN cell quotations rose to 0.35 yuan/W, with actual transaction prices at 0.34 yuan/W. 183N cell demand lacked increments, and inventory is expected to rise. 210RN cell delivery remained tight, and some solar cell manufacturers will increase the production schedule of 210RN cells in April, but it will still be in short supply.

Module: This week, the upward momentum of module prices weakened significantly. The current price of distributed N-type 182 modules is around 0.768-0.778 yuan/W, with the average price up by 0.004 yuan/W WoW. The current price of distributed N-type 210 modules is around 0.773-0.783 yuan/W, with the average price up by 0.003 yuan/W WoW. The current price of centralized N-type 182 modules is 0.704-0.722 yuan/W, and the current price of centralized N-type 210 modules is 0.719-0.737 yuan/W. This week, the upward momentum of module prices weakened significantly. Overall, only a few small-volume orders from top-tier module manufacturers were transacted at a high price of 0.8 yuan/W this week, and most distributed order transaction prices remained around 0.77 yuan/W. As April approaches, the demand for distributed module orders is slowly cooling under the influence of the approaching 430 installation rush period. However, the overall order signing situation for module manufacturers in April is still hot, and the module production schedule in April continues to grow.

EVA: This week, the mainstream transaction prices of PV-grade EVA were 11,550-11,950 yuan/mt, with the increase narrowing. Foam-grade and cable-grade prices remained stable. On the supply side, the maintenance of some petrochemical plants was delayed, and the tight spot supply situation eased, but the overall market still maintained an undersupply pattern. On the demand side, affected by the "430" and "531" installation rush, domestic distributed projects formed a strong boost to spot demand, driving the continuous rise of module production schedules. Supply is tight and demand is increasing, but the further rise of PV-grade EVA prices may be limited by the cost pressure of downstream films due to the new orders in April. It is expected that PV-grade EVA prices will consolidate at highs in the near future.

Film: Recently, the mainstream transaction prices of EVA film were 13,300-13,500 yuan/mt, and EPE film were 15,200-15,500 yuan/mt. Cost side, PV-grade EVA prices continued to fluctuate at highs, providing cost support for the rise of film prices. Demand side, affected by the domestic "installation rush", the demand for distributed PV projects increased significantly, driving the continuous rise of module production schedules. Under the dual push of upstream and downstream, it is expected that film prices will show an upward trend.

PV glass: This week, PV glass quotations remained stable. As of now, the domestic mainstream quotation for 2.0mm single-layer coating is 14.0 yuan/m², the mainstream transaction price is 13.5 yuan/m², the mainstream quotation for 3.2mm single-layer coating is 22.5 yuan/m², and the mainstream quotation for 2.0mm back glass is 12.0 yuan/m². This week, there were no transactions in the domestic market. Module companies mainly bargained for glass prices recently. Glass companies plan to raise quotations recently, with front glass prices planned to increase by 0.5 yuan/m² and back glass prices planned to increase by 1.5 yuan/m². The main reason for the price increase is that domestic module demand in April remains highly rising. Although the number of new production starts on the glass supply side has increased recently, it has not promoted actual production. The overall supply and demand situation of glass in April is still undersupply, and prices are rising, but the actual price increase is expected to be mainly bargained, and the increase in module prices is limited, maintaining a resistant attitude towards the cost increase brought by glass.

High-purity quartz sand: This week, the domestic high-purity quartz sand quotation range remained stable. The current market quotations are as follows: inner layer sand is 65,000-75,000 yuan/mt, middle layer sand is 35,000-45,000 yuan/mt, and outer layer sand is 20,000-25,000 yuan/mt. Recently, domestic sand companies' quotations remained stable. After some quartz sand product prices rose last week, downstream did not accept it. The transaction prices of crucibles have been fluctuating at the bottom recently, and recent demand has been relatively weak, so the supply of crucibles has also slightly decreased recently. At the same time, the resistance to the rise of quartz sand prices has increased. Before the wafer production schedule increases significantly, quartz sand prices are expected to remain stable.

Backsheet: This week, PV backsheet prices remained low and stable. The market price of white CPC backsheet - double-coated fluorine is around 4.9-5.2 yuan/m², and the price of transparent CPC backsheet - double-coated fluorine is around 11.3-12.3 yuan/m². Backsheet market demand continued to be weak. As the month-end approaches, a new round of monthly orders has gradually started. Backsheet manufacturers generally reported that new order prices still maintain low prices around 5 yuan. With the sluggish operation of the backsheet market, upstream PET raw material manufacturers have also started to reduce production according to demand, but raw material prices remain stable for the time being. The PV backsheet market still maintains a weak trend of low prices and low production.

View SMM PV Industry Chain Database