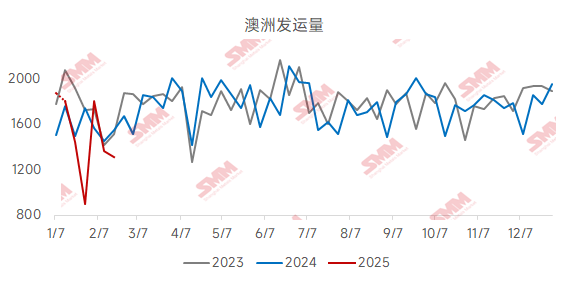

Starting in late January 2025, weather disturbances persisted in the Southern Hemisphere, with frequent cyclones in Australia and heavy rainfall in Brazil, leading to a significant decline in iron ore shipments from Australia and Brazil. According to SMM shipping data, as of January 21, 2025, Australia's shipments had fallen for two consecutive weeks, with weekly shipments dropping from 18 million mt to 8.99 million mt, a reduction of approximately 9 million mt. Although shipments quickly rebounded to the 18 million mt level, they declined again by nearly 5 million mt after February 11. As of February 18, 2025, Australia's total iron ore shipments amounted to 104.97 million mt, a YoY decrease of 5.63 million mt.

Chart: Australia's Weekly Shipments (10,000 mt)

Data Source: SMM

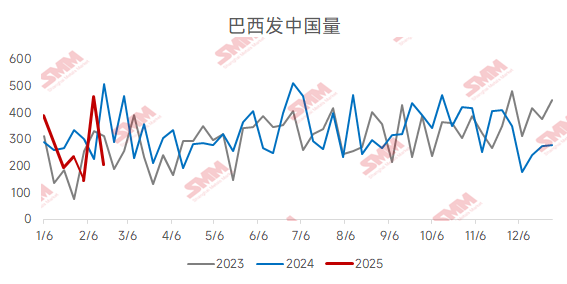

According to SMM shipping data, Brazil's weekly iron ore shipments also declined, but the overall reduction was limited. As of February 18, 2025, Brazil's total iron ore shipments decreased by only 1.62 million mt YoY compared to 2024, indicating relatively stable supply. However, the volume of iron ore shipped from Brazil to China showed a more significant decline.

Chart: Brazil's Weekly Shipments to China (10,000 mt)

Data Source: SMM

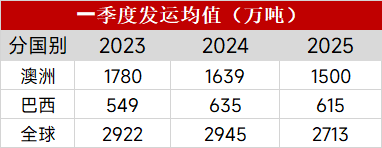

From a quarterly shipment perspective, as of now, the cumulative total shipments in 2025 have decreased by approximately 2.3 million mt compared to the same period last year. If this gap were evenly distributed over the next five weeks, weekly shipments would need to increase by about 460,000 mt. Considering that the current weekly shipment volume has already reached over 20 million mt, SMM believes that an increase of 460,000 mt would have a relatively insignificant impact on the overall shipment volume. If weather conditions in the Southern Hemisphere improve in the future and no longer cause significant disruptions to shipments, the total shipment volume for Q1 2025 is highly likely to recover to the average level of previous years.

Data Source: SMM

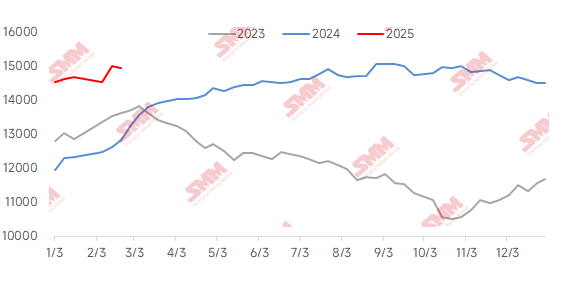

Although recent shipment volumes have declined sharply, domestic demand remains in the off-season, with pig iron production at a moderately low level. As a result, despite the decline in port arrivals, port inventory continues to experience a slight inventory buildup. Coupled with the increase in iron ore import volume last year and the decline in demand, port inventory remains higher than in previous years. Therefore, SMM believes that the short-term decline in overseas iron ore shipments has limited actual impact, providing little support for ore price increases.

Chart: SMM 35-Port Inventory Data (10,000 mt)

Data Source: SMM

Click to View the SMM Metal Industry Chain Database