【SMM: Các yếu tố vĩ mô có thể đẩy trung tâm giá than cốc dầu lên vào năm 2025】Tổng thể, tình hình cung cầu căng thẳng cho than cốc dầu khó có khả năng giảm trong ngắn hạn, với xác suất tăng giá cao. Kể từ tháng Tư, kỳ vọng về sự co lại của nhập khẩu đã mạnh mẽ hơn, cùng với các nhà máy lọc dầu trong nước bước vào giai đoạn bảo dưỡng tập trung, dẫn đến xu hướng tăng giá. Trong trung và dài hạn, công suất mới hạn chế cho than cốc dầu trong nước và dự kiến sẽ rút khỏi công suất lọc dầu địa phương sẽ làm trầm trọng thêm mất cân đối cung cầu, tăng sự phụ thuộc vào nhập khẩu. Bất kỳ gián đoạn nhập khẩu hay tăng chi phí nào cũng sẽ đẩy mạnh giá than cốc dầu. Tuy nhiên, xu hướng giá cũng phải đối mặt với một số bất ổn, như tình hình kinh tế vĩ mô.

On April 16, at the AICE 2025 SMM (20th) Aluminum Industry Conference and Aluminum Industry Expo—Alumina and Aluminum Raw Materials Forum, co-hosted by SMM Information & Technology Co., Ltd., SMM Metal Trading Center, and Shandong Aisi Information Technology Co., Ltd., and co-organized by Zhongyifeng Jinyi (Suzhou) Technology Co., Ltd. and Lezhi Qianrun Investment Service Co., Ltd., Liu Huimin, Senior Analyst of Aluminum Auxiliary Materials at SMM, shared the current supply and demand situation and price forecast of the Chinese petroleum coke market.

**Petroleum Coke Index Classification Standards**

She elaborated on the NB-SH-T 0527-2019 standard of the petrochemical industry of the People's Republic of China.

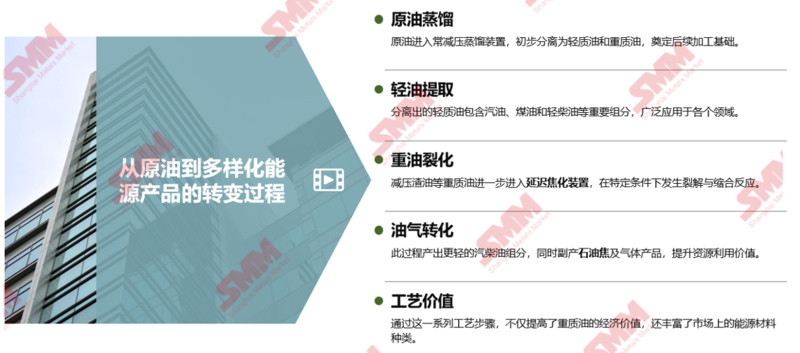

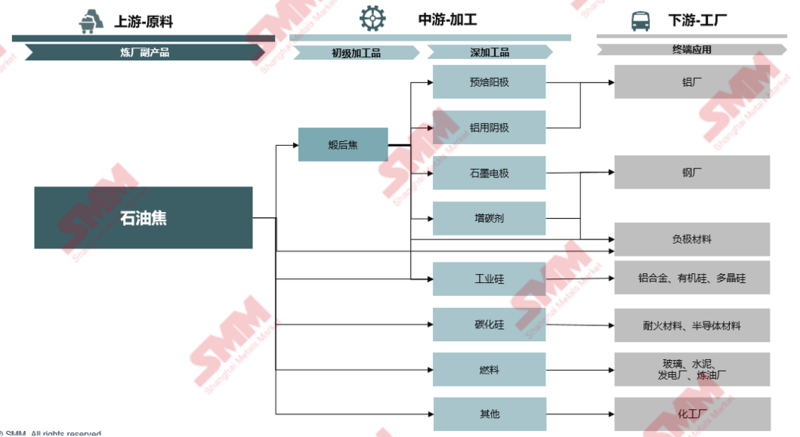

**Where Does Petroleum Coke Come from in the Crude Oil Processing Process?**

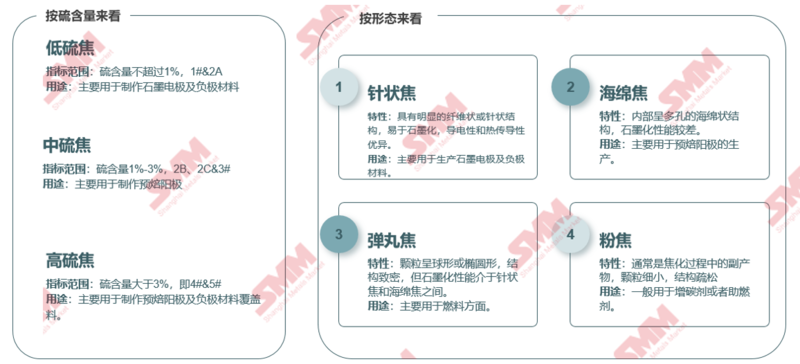

**Classification and Uses of Petroleum Coke**

**Supply Landscape of the Chinese Petroleum Coke Market**

Domestic delayed coking unit capacity has increased year by year, with the growth rate significantly slowing after 2023.

**SMM Analysis:**

- From 2020 to 2024, the compound annual growth rate (CAGR) of China's delayed coking unit capacity was approximately 2.6%, with the growth rate reaching 7.15% in 2022, the highest in five years, mainly due to the commissioning of a 6 million mt/year unit by mainstream refineries in 2022.

- As of 2024, China's refinery delayed coking unit capacity was approximately 151 million mt/year, up 1.28% YoY, continuing the growth trend. Among them, the delayed coking capacity of mainstream refineries remained stable, while two enterprises in Shandong added 1.9 million mt/year of capacity, bringing the total delayed coking capacity of local refineries to 71 million mt/year, accounting for 47% of the total capacity. As of now, there is no additional capacity elimination in 2025, and refinery delayed coking unit capacity is transitioning smoothly.

- In recent years, China's total delayed coking unit capacity has maintained an expansion trend. The continuous development of downstream petroleum coke enterprises and increasing domestic demand have laid a solid foundation for the expansion of refinery delayed coking capacity. Additionally, the extended life cycle of delayed coking units and delayed exit steps have maintained the growth trend of domestic petroleum coke supply.

**Distribution of China's Petroleum Coke Delayed Coking Unit Capacity**

**SMM Analysis:**

- By region: East China, South China, Northeast China, and Northwest China rank in the top four. East China and South China are close to coastal ports, facilitating the loading and unloading of crude oil tankers and efficient, low-cost transportation of overseas crude oil, providing stable and sufficient raw materials for delayed coking units. Northeast China and Northwest China are important domestic crude oil production areas, allowing for local sourcing and short-distance transportation of crude oil to refineries, significantly reducing transportation costs and risks, and strongly promoting the growth of local delayed coking unit capacity.

- By province: Shandong ranks first with a total delayed coking capacity of 55.09 million mt/year, accounting for 36% of the total capacity, with concentrated capacity distribution in Dongying, Zibo, and Binzhou.

**SMM Analysis:**

- By group: Local refineries rank first with a total delayed coking unit capacity of 71 million mt/year, accounting for 47%; Sinopec ranks second with a total capacity of 46.75 million mt/year, accounting for 31%; PetroChina ranks third with a total capacity of 24.5 million mt/year, accounting for 16%; CNOOC ranks last with a total capacity of 8.8 million mt/year, accounting for 6%.

- The delayed coking unit capacity of local refineries is mainly distributed in Shandong, Liaoning, and Zhejiang. Especially in Shandong, its capacity accounts for 65% of local refineries. The large number of local refining enterprises, significant industrial cluster effects, proximity to crude oil import ports and domestic crude oil production areas, convenient raw material acquisition, low transportation costs, and complete industrial support.

**China's Petroleum Coke Supply is Mainly High-Sulfur Coke, with No. 4 Coke Accounting for 57%**

**SMM Analysis:**

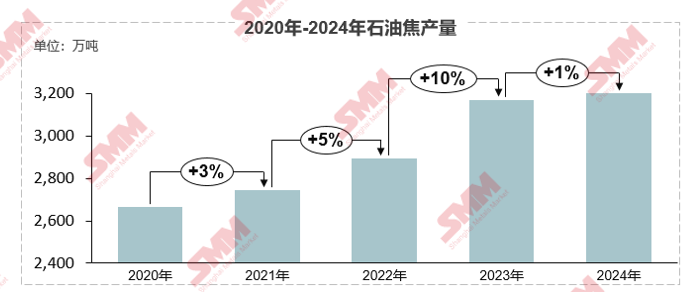

- In 2024, China's petroleum coke production increased to over 32 million mt, up about 1% YoY. China's petroleum coke supply is mainly high-sulfur coke, with No. 4 coke accounting for 57%, followed by medium-sulfur coke accounting for 28%, and low-sulfur coke accounting for only 7%.

- Local refineries account for 73% of high-sulfur petroleum coke production, with No. 4 and No. 5 coke accounting for 68% and 5%, respectively, and medium-sulfur coke No. 2 and No. 3 accounting for 3% and 20%, respectively, with No. 1 accounting for only 4%. High and medium-sulfur coke still dominate, while low-sulfur coke is relatively scarce.

**Total Petroleum Coke Imports Turned Downward in 2024, with High Port Inventory Rapidly Declining**

**SMM Analysis:**

- Since 2019, China's petroleum coke imports have surged, jumping from 8.05 million mt in 2019 to 16.02 million mt in 2023, achieving a doubling growth, with an increase of 99% during the period. The large amount of petroleum coke imports provided sufficient supply for port inventory. From the perspective of petroleum coke port inventory changes in Shandong, port inventory increased significantly in H1 2023, with an increase of 108%, closely related to the continuous increase in imports. A large amount of imported petroleum coke flooded into ports, pushing up inventory levels.

- In 2024, due to the persistently high domestic port petroleum coke inventory, traders' buying sentiment for LME cargoes was moderate, and petroleum coke imports significantly tightened, with total imports of 13.4 million mt, down 16% YoY. With the decline in imports, port inventory continued to destock, with Shandong's petroleum coke port inventory falling 41% to around 1.93 million mt in 2024.

- After entering 2025, Shandong's port petroleum coke inventory fluctuated slightly around 2 million mt.

**US Coke Imports Remained at the Top in 2024, with High-Sulfur Coke Dominating Imports**

**SMM Analysis:**

- In 2024, China's petroleum coke import market showed distinct characteristics, with the US playing a key role. By import source, the US accounted for 3.8614 million mt, representing 28.82% of total imports. Russia ranked second with an import share of 18%, demonstrating its strong strength in the petroleum coke export field. Saudi Arabia accounted for 12%, Canada for 7%, and Colombia and Venezuela each accounted for 6%, collectively forming important suppliers of China's petroleum coke imports.

- By import variety, high-sulfur coke dominated throughout the year. Data from 2024 shows that high-sulfur coke accounted for 71%, medium-sulfur coke for 19%, and low-sulfur coke for 10%. Compared with 2023, the share of high-sulfur coke slightly decreased but still dominated. The share of medium-sulfur coke increased from 14% to 19%, while the share of low-sulfur coke decreased from 12% to 10%.

**US Coke Import Tariffs Escalated, Rising Costs Expected to Lead to a Significant Decline in US Coke Imports**

**SMM Analysis:**

- Since April 2025, the US-China trade friction has intensified, and China has adjusted tariffs on US-origin imported goods multiple times. As of April 11, China's tariffs on US-origin imported goods increased from the initial 34% to 125%, with the effective tariff rate rising to 128%.

- Goods shipped from the place of shipment before 12:01 on April 10 and imported between 12:01 on April 10 and 24:00 on May 13, 2025, are not subject to the additional tariffs.

- As the world's largest petroleum coke producer, the US has a competitive edge in the Chinese market due to its stable supply capability and reasonable pricing system. Based on the current landed price, the cost of US petroleum coke has increased by at least 1,100 yuan/mt, a rise of over 20%, significantly reducing the cost-effectiveness of US petroleum coke imports to China. SMM expects US coke imports to decrease by more than 30%.

**Multiple Factors Intertwined in 2025, Refinery Operating Cost Dilemma Intensified**

**Raw Material Price Increases and Increased Maintenance Enterprises, Domestic Petroleum Coke Supply Reduced in 2025**

**SMM Analysis:**

- Against the above background, since Q1 2025, the frequency of maintenance of domestic refinery delayed coking units has significantly increased. According to SMM statistics, as of the end of March, 32 sets of refinery delayed coking units in China were under maintenance, up about 78% YoY, involving a capacity of 35.9 million mt, up 69% YoY.

- Looking ahead to the full year, it is expected that 20 more sets of refinery delayed coking units will undergo maintenance, involving a capacity of about 28.8 million mt. Based on the refinery maintenance information available so far, mainstream refineries dominate the shutdown units in 2025, accounting for about 70% of the involved capacity. Local refineries have the largest maintenance scale for the year, reaching 34 million mt. The maintenance indicators are mainly high-sulfur coke, with No. 4 petroleum coke accounting for the largest share, reaching 54% of the total capacity.

**Demand Landscape of the Chinese Petroleum Coke Market**

**Overview of Downstream Demand for Petroleum Coke**

**Prebaked Anode: Capacity Increasing Year by Year, Local Supply-Demand Imbalance Evident**

It analyzed the capacity growth of the prebaked anode industry, monthly production of prebaked anodes, monthly production of aluminum enterprises, and the matching of prebaked anode and aluminum capacity.

**Prebaked Anode: Future Capacity Expansion Closely Follows Downstream Demand, Southwest and Mongolia Become Industry Focus Areas**

**SMM Analysis:**

- From 2025 to 2028, a total of 6.17 million mt of prebaked anode capacity is planned to be commissioned. Excluding new plans without indicators, the net increase in domestic aluminum capacity in 2025 and beyond is 650,000 mt. The speed of prebaked anode capacity expansion far exceeds the growth of market demand, exacerbating the surplus problem, and industry competition will become more intense.

- By region of new capacity: Southwest China: Capacity expansion is significant, being the main growth area. New projects in Guangxi, Yunnan, and other places are numerous, attracting aluminum capacity transfer due to abundant hydropower resources, driving prebaked anode demand. Shandong: As the main production area, it continues to expand capacity with raw material and geographical advantages. Inner Mongolia: Due to the transfer of aluminum capacity from Henan and other places, local enterprises have increased production, driving prebaked anode capacity growth.

**Kể từ năm 2022, Công suất Vật liệu Điện cực Âm đã Mở rộng Nhanh chóng, với Tỷ lệ Sử dụng Công suất Hiệu quả Giảm dần theo Năm**

**Phân tích của SMM:**

- Kể từ năm 2022, công suất vật liệu điện cực âm đã mở rộng nhanh chóng, đạt khoảng 4,97 triệu tấn vào năm 2024, với tỷ lệ tăng trưởng công suất là 150%. Tuy nhiên, tỷ lệ tăng trưởng công suất vượt xa nhu cầu hạ nguồn, dẫn đến mất cân đối cung-cầu và cạnh tranh ngày càng khốc liệt. Công suất mới khó phát hành, và tỷ lệ sử dụng công suất hiệu quả đã giảm từ 71% xuống 37%.

- Sản lượng năm 2022 là 1,41 triệu tấn, và vào năm 2024, đạt 1,84 triệu tấn, với tỷ lệ tăng trưởng công suất khoảng 31%. Mặc dù có sự tăng trưởng, nhưng mức độ tương đối hạn chế so với việc mở rộng công suất, và xu hướng tăng trưởng sản xuất tương đối phẳng trong ba năm.

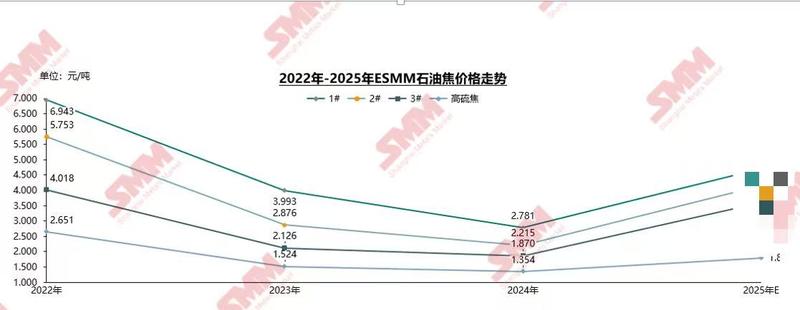

**Đánh giá Giá Cacbon Dầu năm 2024**

**Từ tháng 9/2024, Giá Cacbon Dầu Hấp thụ Lưu huỳnh Thấp Tiếp tục Tăng do Nhu cầu Tích trữ Tăng**

**Phân tích của SMM:**

- Từ tháng 1 đến tháng 4/2024, cacbon dầu hấp thụ lưu huỳnh thấp ở Đông Bắc Trung Quốc có xu hướng tăng do thị trường vật liệu điện cực âm phục hồi và lịch sản xuất của các nhà máy pin hạ nguồn tăng, dẫn đến nhu cầu tăng. Tuy nhiên, sau khi bước vào quý 2, việc thực hiện đơn hàng hạ nguồn và số lượng đơn hàng mới của các doanh nghiệp điện cực âm giảm, làm suy yếu dần nhu cầu mua cacbon dầu. Kết hợp với dư cung nội địa, giá cacbon dầu hấp thụ lưu huỳnh thấp bắt đầu dao động giảm nhẹ.

- Bắt đầu từ cuối quý 3/2024, do hiệu suất đơn hàng hạ nguồn của các doanh nghiệp vật liệu điện cực âm tốt, tồn kho cacbon dầu của họ đã giảm xuống mức thấp, kích thích tích trữ và bổ sung hàng hóa. Yếu tố này, cùng với các yếu tố khác, đã thúc đẩy giá cacbon dầu hấp thụ lưu huỳnh thấp chuyển từ giảm sang tăng. Đặc biệt trong quý 1/2025, việc tích trữ tập trung trong kỳ nghỉ Tết Nguyên đán và can thiệp chính sách đã khuếch đại kỳ vọng thị trường, thúc đẩy giá cacbon dầu hấp thụ lưu huỳnh thấp tăng nhanh.

Năm 2024, giá cacbon dầu hấp thụ lưu huỳnh trung bình và cao chủ yếu dao động, và sau khi bước vào năm 2025, giá cacbon dầu tăng nhanh.

Phân tích của SMM:

ØNăm 2024, giá cacbon dầu hấp thụ lưu huỳnh trung bình và cao ở Sơn Đông dao động nhẹ. Trong quý 1, thị trường anôt cải thiện, giao dịch sôi động, doanh nghiệp carbon hạ nguồn mua sắm tích cực, và giá tăng nhẹ. Trong quý 2, bảo dưỡng nhà máy lọc dầu tăng, cung giảm, mua sắm kịp thời hỗ trợ giá tăng nhẹ, và sau đó do tâm lý mua sắm giảm, giá có xu hướng giảm. Tháng 9, lợi nhuận kém của các nhà máy lọc dầu địa phương dẫn đến tăng hàm lượng lưu huỳnh, một số doanh nghiệp ngừng bảo dưỡng, và cung cấp cacbon dầu hấp thụ lưu huỳnh trung bình khan hiếm, giá mạnh lên. Giá cacbon dầu hấp thụ lưu huỳnh cao tăng nhẹ trong quý 1 do tâm lý thị trường, và sau đó dao động giảm.

ØSau khi bước vào năm 2025, do tăng chi phí nguyên liệu của nhà máy lọc dầu, một số nhà máy, đặc biệt là ở Sơn Đông, giảm sản xuất, kết hợp với kỳ nghỉ Tết Nguyên đán, doanh nghiệp anôt nung sẵn hạ nguồn tích trữ tập trung, và giá cacbon dầu đón nhận sự tăng trưởng bùng nổ. Giá cacbon dầu nung và anôt nung sẵn cũng tăng nhanh theo giá nguyên liệu cacbon dầu. Đến tháng 4, giá mua anôt nung sẵn của doanh nghiệp chuẩn tăng lên 5.205 nhân dân tệ/tấn, tăng 29% so với đầu năm.

Dự báo Giá Cacbon Dầu năm 2025

Yếu tố Ảnh hưởng Giá năm 2025

►Khía cạnh vĩ mô và Chính sách

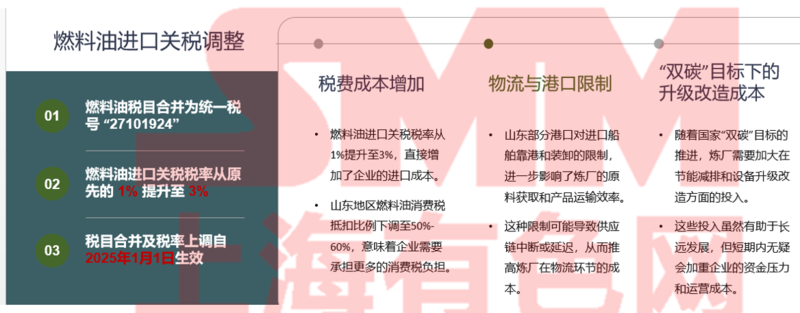

1. Điều chỉnh Thuế Nhập khẩu

Từ tháng 1/2025, thuế suất nhập khẩu nhiên liệu sẽ tăng từ 1% lên 3%, và tỷ lệ khấu trừ thuế tiêu thụ nhiên liệu ở Sơn Đông cũng giảm đáng kể từ khấu trừ toàn bộ xuống khoảng 50-60%. Từ ngày 12/4/2025, thuế 125% sẽ được áp dụng cho tất cả hàng hóa nhập khẩu có nguồn gốc từ Mỹ, và thuế nhập khẩu sẽ tăng từ 3% lên 128%.

2. Chính sách Tiết kiệm Năng lượng và Giảm Carbon

Mục tiêu "đôi carbon" thúc đẩy nâng cấp bảo vệ môi trường và chuẩn hóa thuế, và yêu cầu bảo vệ môi trường và tuân thủ của nhà máy lọc dầu địa phương được cải thiện. Tỉnh Sơn Đông dự kiến giảm công suất chế biến dầu thô của ngành lọc dầu địa phương từ 130 triệu tấn/năm xuống khoảng 90 triệu tấn/năm vào năm 2025, giảm 30%, và loại bỏ công suất lạc hậu thông qua hợp nhất và các biện pháp khác. Năm 2024, nhiều cơ quan quốc gia yêu cầu loại bỏ các đơn vị khí quyển và chân không có công suất 2 triệu tấn/năm trở xuống, và hơn 20% đơn vị như vậy ở Sơn Đông bị ảnh hưởng.

►Cơ bản

3. Cung cấp Cacbon Dầu Nội địa

Năm 2025, không có kế hoạch thêm đơn vị chưng cất chậm ở Trung Quốc, và việc đóng cửa và bảo dưỡng đơn vị chưng cất chậm ở nhà máy lọc dầu diễn ra thường xuyên trong năm. Sự mất mát do bảo dưỡng trong tháng 4-5 tăng đáng kể, cộng với tác động của thuế tiêu thụ đối với biên lợi nhuận, tỷ lệ sử dụng công suất chưng cất chậm giảm. Dựa trên thông tin trên, cung cấp cacbon dầu nội địa dự kiến giảm trong năm 2025.

4. Tình hình Nhập khẩu Cacbon Dầu

Mỹ là nguồn nhập khẩu cacbon dầu lớn nhất ở Trung Quốc. Thuế nhập khẩu cacbon dầu của Mỹ tăng từng lớp, và chi phí tăng đáng kể. Tổng nhập khẩu cacbon dầu của Mỹ dự kiến giảm 30-40%. Tổng thể, nhập khẩu cacbon dầu năm 2025 dự kiến tăng YoY, nhưng mức tăng hạn chế, và tình trạng cung cấp khan hiếm cacbon dầu khó thay đổi.

5. Nhu cầu Cacbon Dầu Nội địa

Nhu cầu ngành nhôm đang tăng ổn định, cung cấp hỗ trợ ổn định cho nhu cầu cacbon dầu. Nhu cầu lĩnh vực năng lượng mới nổi như vật liệu anôt và silicon đa tinh thể PV tăng nhanh, trở thành lực lượng quan trọng thúc đẩy nhu cầu cacbon dầu. Tuy nhiên, nhu cầu của một số ngành truyền thống, như ngành kính, đang thu hẹp, và nhu cầu ngành kim loại silic trung bình. Cấu trúc nhu cầu thị trường cacbon dầu liên tục tái tạo, và tỷ lệ lĩnh vực liên quan đến năng lượng mới tăng.

Cơ bản vĩ mô thuận lợi cho sự tăng giá cacbon dầu, và trung tâm giá cacbon dầu năm 2025 sẽ di chuyển rõ ràng lên.

Phân tích của SMM:

ØTổng thể, ngắn hạn, tình trạng cung-cầu khan hiếm cacbon dầu khó giảm, khả năng tăng giá cao. Từ tháng 4, kỳ vọng co lại nhập khẩu tăng cường, cộng với nhà máy lọc dầu nội địa bước vào giai đoạn bảo dưỡng tập trung, và giá có xu hướng tăng. Trung và dài hạn, công suất mới cacbon dầu nội địa ít và kỳ vọng rút lui công suất nhà máy lọc dầu địa phương, mất cân đối cung-cầu tăng, phụ thuộc vào nhập khẩu tiếp tục tăng, và rào cản hoặc tăng chi phí nhập khẩu sẽ tăng đáng kể giá cacbon dầu.

ØTuy nhiên, xu hướng giá cũng đối mặt với một số yếu tố không chắc chắn, như nếu tình hình kinh tế vĩ mô phục hồi chậm, thời gian phục hồi nhu cầu tiêu dùng của doanh nghiệp thực tế và đầu cuối công nghiệp sẽ lâu hơn, có thể kiềm chế tăng giá; nếu thị trường than và chính sách liên quan thay đổi, cũng sẽ có tác động gián tiếp đến giá cacbon dầu.

》Nhấp để xem báo cáo chuyên đề AICE 2025 SMM (lần thứ 20) Hội nghị và Triển lãm Ngành Nhôm