【SMM: ปัจจัยพื้นฐานทางมาโครอาจทำให้ราคาโคกปิโตรเลียมสูงขึ้นในปี 2025】โดยรวมแล้ว สถานการณ์อุปสงค์และอุปทานที่ตึงตัวของโคกปิโตรเลียมไม่น่าจะคลายลงในระยะสั้น มีโอกาสสูงที่ราคาจะเพิ่มขึ้น ตั้งแต่เดือนเมษายนเป็นต้นมา การคาดการณ์ว่าการนำเข้าจะหดตัวได้รับความแข็งแกร่งมากขึ้น ประกอบกับโรงกลั่นในประเทศเข้าสู่ช่วงการบำรุงรักษาอย่างหนาแน่น ส่งผลให้ราคามีแนวโน้มเพิ่มขึ้น ในระยะกลางถึงยาว กำลังการผลิตใหม่ที่จำกัดสำหรับโคกปิโตรเลียมในประเทศและการคาดการณ์ว่ากำลังการกลั่นภายในประเทศจะออกจากตลาด จะทำให้ความไม่สมดุลระหว่างอุปสงค์และอุปทานแย่ลง ทำให้ต้องพึ่งพาการนำเข้ามากขึ้น การหยุดชะงักในการนำเข้าหรือการเพิ่มขึ้นของต้นทุนจะทำให้ราคาโคกปิโตรเลียมเพิ่มขึ้นอย่างมาก อย่างไรก็ตาม แนวโน้มราคาอาจเผชิญกับความไม่แน่นอนบางประการ เช่น สถานการณ์เศรษฐกิจภาพรวม

เมื่อวันที่ 16 เมษายน ในการประชุมและนิทรรศการ AICE 2025 SMM (ครั้งที่ 20) ซึ่งจัดโดยบริษัท SMM Information & Technology Co., Ltd., SMM Metal Trading Center, และ Shandong Aisi Information Technology Co., Ltd. ร่วมกับ Zhongyifeng Jinyi (Suzhou) Technology Co., Ltd. และ Lezhi Qianrun Investment Service Co., Ltd. หลิว หุยหมิน นักวิเคราะห์อาวุโสของ SMM ได้แบ่งปันสถานการณ์อุปสงค์และอุปทานปัจจุบันและการคาดการณ์ราคาตลาดโคกปิโตรเลียมของจีน

**มาตรฐานการจำแนกดัชนีโคกปิโตรเลียม**

เธออธิบายเกี่ยวกับมาตรฐาน NB-SH-T 0527-2019 ของอุตสาหกรรมปิโตรเคมีแห่งสาธารณรัฐประชาชนจีน

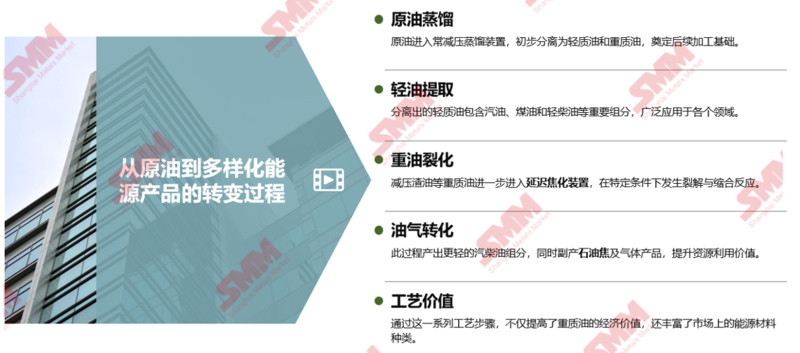

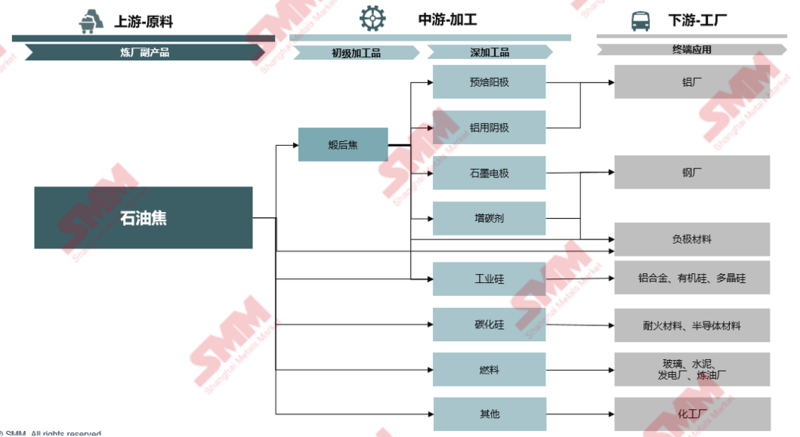

**โคกปิโตรเลียมมาจากกระบวนการแปรรูปน้ำมันดิบอย่างไร?**

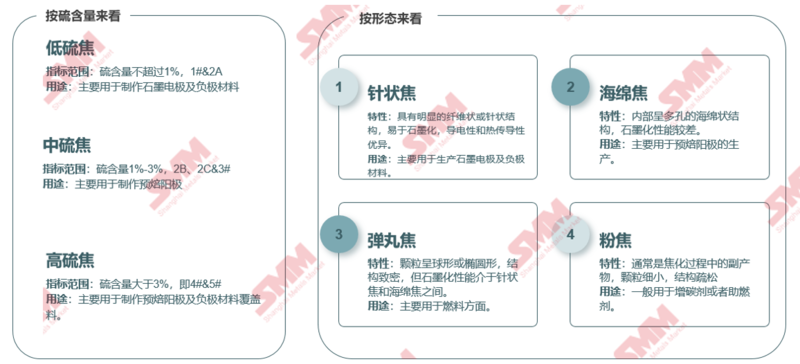

**การจำแนกและใช้งานโคกปิโตรเลียม**

**ภาพรวมอุปทานตลาดโคกปิโตรเลียมของจีน**

กำลังการผลิตของหน่วยแกลบโคกในประเทศเพิ่มขึ้นทุกปี แต่อัตราการเติบโตลดลงอย่างมากหลังปี 2023

**การวิเคราะห์ของ SMM:**

- ระหว่างปี 2020 ถึง 2024 อัตราการเติบโตแบบผสมผสานรายปี (CAGR) ของกำลังการผลิตหน่วยแกลบโคกของจีนอยู่ที่ประมาณ 2.6% โดยอัตราการเติบโตสูงสุดในห้าปีที่ 7.15% ในปี 2022 เนื่องจากโรงงานหลักเริ่มใช้งานหน่วย 6 ล้านตัน/ปีในปี 2022

- จนถึงปี 2024 กำลังการผลิตหน่วยแกลบโคกของโรงกลั่นน้ำมันในจีนอยู่ที่ประมาณ 151 ล้านตัน/ปี เพิ่มขึ้น 1.28% ตามปี แนวโน้มการเติบโตยังคงดำเนินต่อไป กำลังการผลิตหน่วยแกลบโคกของโรงกลั่นหลักยังคงเสถียร ในขณะที่สองบริษัทในชิงไห่เพิ่มกำลังการผลิต 1.9 ล้านตัน/ปี ทำให้กำลังการผลิตหน่วยแกลบโคกของโรงกลั่นท้องถิ่นรวมเป็น 71 ล้านตัน/ปี หรือ 47% ของกำลังการผลิตทั้งหมด จนถึงตอนนี้ไม่มีการกำจัดกำลังการผลิตเพิ่มเติมในปี 2025 และกำลังการผลิตหน่วยแกลบโคกของโรงกลั่นเปลี่ยนแปลงอย่างราบรื่น

- ในช่วงหลายปีที่ผ่านมา กำลังการผลิตหน่วยแกลบโคกของจีนยังคงขยายตัว การพัฒนาอย่างต่อเนื่องของบริษัทโคกปิโตรเลียมทางปลายน้ำและความต้องการภายในประเทศที่เพิ่มขึ้นได้สร้างพื้นฐานที่แข็งแกร่งสำหรับการขยายกำลังการผลิตหน่วยแกลบโคกของโรงกลั่น นอกจากนี้วงจรชีวิตที่ยาวนานของหน่วยแกลบโคกและการออกจากการทำงานที่ล่าช้าได้รักษาแนวโน้มการเติบโตของการจัดหาโคกปิโตรเลียมในประเทศ

**การกระจายกำลังการผลิตหน่วยแกลบโคกโคกปิโตรเลียมของจีน**

**การวิเคราะห์ของ SMM:**

- ตามภูมิภาค: ภาคตะวันออก ภาคใต้ ภาคตะวันออกเฉียงเหนือ และภาคตะวันตกเฉียงเหนือ อยู่ในอันดับสี่อันดับแรก ภาคตะวันออกและภาคใต้ใกล้กับท่าเรือน้ำมันดิบ ทำให้สามารถขนถ่ายและขนส่งน้ำมันดิบจากต่างประเทศได้อย่างมีประสิทธิภาพและต้นทุนต่ำ มอบวัตถุดิบที่เสถียรและเพียงพอให้กับหน่วยแกลบโคก ภาคตะวันออกเฉียงเหนือและภาคตะวันตกเฉียงเหนือเป็นพื้นที่ผลิตน้ำมันดิบสำคัญในประเทศ ทำให้สามารถขนส่งน้ำมันดิบจากท้องถิ่นได้ระยะทางสั้น ลดต้นทุนและความเสี่ยงในการขนส่ง และส่งเสริมการเติบโตของกำลังการผลิตหน่วยแกลบโคกในท้องถิ่นอย่างมาก

- ตามจังหวัด: ชิงไห่ติดอันดับหนึ่งด้วยกำลังการผลิตหน่วยแกลบโคก 55.09 ล้านตัน/ปี หรือ 36% ของกำลังการผลิตทั้งหมด กำลังการผลิตกระจุกตัวอยู่ที่ตงหยิง จิโบ และบินโจว

**การวิเคราะห์ของ SMM:**

- ตามกลุ่ม: โรงกลั่นท้องถิ่นติดอันดับหนึ่งด้วยกำลังการผลิตหน่วยแกลบโคก 71 ล้านตัน/ปี หรือ 47% รองลงมาคือ Sinopec ด้วยกำลังการผลิต 46.75 ล้านตัน/ปี หรือ 31% PetroChina อยู่ที่ 24.5 ล้านตัน/ปี หรือ 16% และ CNOOC อยู่ที่ 8.8 ล้านตัน/ปี หรือ 6%

- กำลังการผลิตหน่วยแกลบโคกของโรงกลั่นท้องถิ่นกระจุกตัวอยู่ที่ชิงไห่ เหลียวหนิง และเจ้อเจียง โดยเฉพาะในชิงไห่ กำลังการผลิตของท้องถิ่นคิดเป็น 65% ของโรงกลั่นท้องถิ่น จำนวนบริษัทกลั่นท้องถิ่นที่มาก ผลกระทบจากการรวมกลุ่มอุตสาหกรรมที่สำคัญ ความใกล้ชิดกับท่าเรือนำเข้าน้ำมันดิบและพื้นที่ผลิตน้ำมันดิบในประเทศ ทำให้การได้วัตถุดิบสะดวก ต้นทุนการขนส่งต่ำ และมีระบบสนับสนุนอุตสาหกรรมครบถ้วน

**โคกปิโตรเลียมของจีนส่วนใหญ่เป็นโคกกำมะถันสูง โคกหมายเลข 4 คิดเป็น 57%**

**การวิเคราะห์ของ SMM:**

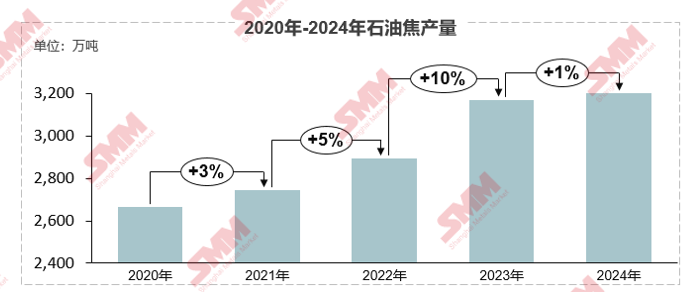

- ในปี 2024 การผลิตโคกปิโตรเลียมของจีนเพิ่มขึ้นเป็นมากกว่า 32 ล้านตัน เพิ่มขึ้นประมาณ 1% ตามปี โคกปิโตรเลียมของจีนส่วนใหญ่เป็นโคกกำมะถันสูง โคกหมายเลข 4 คิดเป็น 57% รองลงมาคือโคกกำมะถันปานกลาง คิดเป็น 28% และโคกกำมะถันต่ำ คิดเป็นเพียง 7%

- โรงกลั่นท้องถิ่นผลิตโคกกำมะถันสูง 73% โคกหมายเลข 4 และ 5 คิดเป็น 68% และ 5% ตามลำดับ โคกกำมะถันปานกลาง หมายเลข 2 และ 3 คิดเป็น 3% และ 20% ตามลำดับ โคกหมายเลข 1 คิดเป็นเพียง 4% โคกกำมะถันสูงและปานกลางยังคงเป็นหลัก ในขณะที่โคกกำมะถันต่ำค่อนข้างหายาก

**การนำเข้าโคกปิโตรเลียมทั้งหมดลดลงในปี 2024 ระดับสต็อกที่ท่าเรือสูงลดลงอย่างรวดเร็ว**

**การวิเคราะห์ของ SMM:**

- ตั้งแต่ปี 2019 การนำเข้าโคกปิโตรเลียมของจีนเพิ่มขึ้นอย่างมาก จาก 8.05 ล้านตันในปี 2019 เป็น 16.02 ล้านตันในปี 2023 หรือเพิ่มขึ้น 99% ระหว่างช่วงเวลาดังกล่าว ปริมาณการนำเข้าโคกปิโตรเลียมที่มากทำให้สต็อกที่ท่าเรือเพียงพอ จากระดับสต็อกโคกปิโตรเลียมที่ท่าเรือในชิงไห่ สต็อกเพิ่มขึ้นอย่างมากในครึ่งปีแรกของปี 2023 เพิ่มขึ้น 108% ซึ่งเกี่ยวข้องกับการเพิ่มขึ้นอย่างต่อเนื่องของการนำเข้า โคกปิโตรเลียมนำเข้าจำนวนมากไหลเข้าท่าเรือ ทำให้ระดับสต็อกเพิ่มขึ้น

- ในปี 2024 เนื่องจากสต็อกโคกปิโตรเลียมที่ท่าเรือในประเทศสูงอย่างต่อเนื่อง ความต้องการซื้อของผู้ค้า LME อยู่ในระดับปานกลาง และการนำเข้าโคกปิโตรเลียมลดลงอย่างมาก รวม 13.4 ล้านตัน ลดลง 16% ตามปี ด้วยการลดลงของการนำเข้า สต็อกท่าเรือยังคงลดลง สต็อกโคกปิโตรเลียมที่ท่าเรือในชิงไห่ลดลง 41% เป็นประมาณ 1.93 ล้านตันในปี 2024

- หลังจากเข้าสู่ปี 2025 สต็อกโคกปิโตรเลียมที่ท่าเรือในชิงไห่แกว่งอยู่ที่ประมาณ 2 ล้านตัน

**การนำเข้าโคกจากสหรัฐฯ ยังคงอยู่ในอันดับหนึ่งในปี 2024 โคกกำมะถันสูงเป็นหลักในการนำเข้า**

**การวิเคราะห์ของ SMM:**

- ในปี 2024 ตลาดการนำเข้าโคกปิโตรเลียมของจีนมีลักษณะเด่น โดยสหรัฐฯ มีบทบาทสำคัญ ตามแหล่งนำเข้า สหรัฐฯ คิดเป็น 3.8614 ล้านตัน หรือ 28.82% ของปริมาณการนำเข้าทั้งหมด รัสเซียอยู่ในอันดับสองด้วยส่วนแบ่งการนำเข้า 18% แสดงถึงความแข็งแกร่งในการส่งออกโคกปิโตรเลียม ซาอุดิอาระเบียคิดเป็น 12% แคนาดา 7% และโคลอมเบียและเวเนซุเอลา คิดเป็น 6% แต่ละประเทศร่วมกันเป็นผู้จำหน่ายโคกปิโตรเลียมที่สำคัญของจีน

- ตามประเภทการนำเข้า โคกกำมะถันสูงเป็นหลักตลอดปี ข้อมูลในปี 2024 แสดงว่าโคกกำมะถันสูงคิดเป็น 71% โคกกำมะถันปานกลาง 19% และโคกกำมะถันต่ำ 10% เมื่อเทียบกับปี 2023 ส่วนแบ่งของโคกกำมะถันสูงลดลงเล็กน้อย แต่ยังคงเป็นหลัก ส่วนแบ่งของโคกกำมะถันปานกลางเพิ่มขึ้นจาก 14% เป็น 19% ในขณะที่ส่วนแบ่งของโคกกำมะถันต่ำลดลงจาก 12% เป็น 10%

**ภาษีนำเข้าโคกจากสหรัฐฯ เพิ่มขึ้น ต้นทุนที่เพิ่มขึ้นคาดว่าจะทำให้การนำเข้าโคกจากสหรัฐฯ ลดลงอย่างมาก**

**การวิเคราะห์ของ SMM:**

- ตั้งแต่เดือนเมษายน 2025 ความขัดแย้งทางการค้าระหว่างสหรัฐฯ และจีนทวีความรุนแรง จีนปรับภาษีสำหรับสินค้านำเข้าจากสหรัฐฯ หลายครั้ง จนถึงวันที่ 11 เมษายน ภาษีสำหรับสินค้านำเข้าจากสหรัฐฯ เพิ่มขึ้นจาก 34% เป็น 125% ด้วยอัตราภาษีที่มีผล 128%

- สินค้าที่ส่งออกจากที่ส่งก่อน 12:01 น. ของวันที่ 10 เมษายน และนำเข้าระหว่าง 12:01 น. ของวันที่ 10 เมษายน ถึง 24:00 น. ของวันที่ 13 พฤษภาคม 2025 ไม่ต้องเสียภาษีเพิ่ม

- ในฐานะผู้ผลิตโคกปิโตรเลียมรายใหญ่ที่สุดในโลก สหรัฐฯ มีข้อได้เปรียบในการแข่งขันในตลาดจีนด้วยความสามารถในการจัดหาที่เสถียรและระบบราคาที่เหมาะสม ตามราคาที่ลงจอด ต้นทุนของโคกปิโตรเลียมจากสหรัฐฯ เพิ่มขึ้นอย่างน้อย 1,100 หยวน/ตัน หรือเพิ่มขึ้นมากกว่า 20% ทำให้ความคุ้มค่าของการนำเข้าโคกปิโตรเลียมจากสหรัฐฯ ลดลงอย่างมาก SMM คาดว่าการนำเข้าโคกจากสหรัฐฯ จะลดลงมากกว่า 30%

**ปัจจัยหลายอย่างเชื่อมโยงกันในปี 2025 ปัญหาต้นทุนการดำเนินงานของโรงกลั่นทวีความรุนแรง**

**ราคาวัตถุดิบเพิ่มขึ้นและจำนวนบริษัทที่บำรุงรักษาเพิ่มขึ้น การจัดหาโคกปิโตรเลียมในประเทศลดลงในปี 2025**

**การวิเคราะห์ของ SMM:**

- ภายใต้พื้นหลังดังกล่าว ตั้งแต่ไตรมาสแรกของปี 2025 ความถี่ในการบำรุงรักษาหน่วยแกลบโคกของโรงกลั่นในประเทศเพิ่มขึ้นอย่างมาก ตามสถิติของ SMM จนถึงปลายเดือนมีนาคม มี 32 ชุดหน่วยแกลบโคกของโรงกลั่นในจีนที่อยู่ในการบำรุงรักษา เพิ่มขึ้นประมาณ 78% ตามปี ด้วยกำลังการผลิต 35.9 ล้านตัน เพิ่มขึ้น 69% ตามปี

- มองไปข้างหน้าตลอดทั้งปี คาดว่าจะมี 20 ชุดหน่วยแกลบโคกของโรงกลั่นที่จะเข้าสู่การบำรุงรักษา ด้วยกำลังการผลิตประมาณ 28.8 ล้านตัน ตามข้อมูลการบำรุงรักษาโรงกลั่นที่มีอยู่ โรงกลั่นหลักเป็นผู้ควบคุมการปิดหน่วยในปี 2025 คิดเป็นประมาณ 70% ของกำลังการผลิตที่เกี่ยวข้อง โรงกลั่นท้องถิ่นมีขนาดการบำรุงรักษาที่ใหญ่ที่สุดในปี คือ 34 ล้านตัน ตัวชี้วัดการบำรุงรักษาส่วนใหญ่เป็นโคกกำมะถันสูง โคกหมายเลข 4 คิดเป็นสัดส่วนใหญ่ที่สุด คือ 54% ของกำลังการผลิตทั้งหมด

**ภาพรวมความต้องการตลาดโคกปิโตรเลียมของจีน**

**ภาพรวมความต้องการทางปลายน้ำของโคกปิโตรเลียม**

**อะโนดเผาล่วงหน้า: กำลังการผลิตเพิ่มขึ้นทุกปี ความไม่สมดุลระหว่างอุปทานและอุปสงค์ในท้องถิ่นชัดเจน**

วิเคราะห์การเติบโตของกำลังการผลิตอุตสาหกรรมอะโนดเผาล่วงหน้า การผลิตอะโนดเผาล่วงหน้ารายเดือน การผลิตอลูมิเนียมรายเดือน และการจับคู่กำลังการผลิตอะโนดเผาล่วงหน้าและอลูมิเนียม

**อะโนดเผาล่วงหน้า: การขยายกำลังการผลิตในอนาคตติดตามความต้องการทางปลายน้ำ ภาคตะวันตกเฉียงใต้และมองโกเลียกลายเป็นพื้นที่สำคัญของอุตสาหกรรม**

**การวิเคราะห์ของ SMM:**

- ระหว่างปี 2025 ถึง 2028 มีแผนการขยายกำลังการผลิตอะโนดเผาล่วงหน้า 6.17 ล้านตัน ยกเว้นแผนใหม่ที่ไม่มีตัวชี้วัด กำลังการผลิตอลูมิเนียมในประเทศที่เพิ่มขึ้นในปี 2025 และต่อไปคือ 650,000 ตัน ความเร็วในการขยายกำลังการผลิตอะโนดเผาล่วงหน้าเกินกว่าการเติบโตของความต้องการตลาด ทำให้ปัญหาส่วนเกินทวีความรุนแรง ความแข่งขันในอุตสาหกรรมจะเพิ่มขึ้น

- ตามพื้นที่ของกำลังการผลิตใหม่: ภาคตะวันตกเฉียงใต้: การขยายกำลังการผลิตมีนัยสำคัญ เป็นพื้นที่การเติบโตหลัก โครงการใหม่ในกว่างซี ยูนนาน และที่อื่น ๆ มากมาย ดึงดูดการย้ายกำลังการผลิตอลูมิเนียมด้วยทรัพยากรพลังงานน้ำที่อุดมสมบูรณ์ กระตุ้นความต้องการอะโนดเผาล่วงหน้า ชิงไห่: เป็นพื้นที่การผลิตหลัก ยังคงขยายกำลังการผลิตด้วยข้อได้เปรียบด้านวัตถุดิบและภูมิศาสตร์ มณฑลมณฑล: เนื่องจากการย้ายกำลังการผลิตอลูมิเนียมจากเหอหนานและที่อื่น ๆ บริษัทท้องถิ่นเพิ่มการผลิต กระตุ้นการเติบโตของกำลังการผลิตอะโนดเผาล่วงหน้า**Since 2022, Negative Electrode Material Capacity Has Rapidly Expanded, with Effective Capacity Utilization Rate Decreasing Year by Year**

**SMM Analysis:**

- Since 2022, negative electrode material capacity has rapidly expanded, reaching about 4.97 million mt by 2024, with a capacity growth rate of 150%. However, the capacity growth rate far exceeds downstream demand, leading to a supply-demand imbalance and increasingly fierce competition. New capacity is difficult to release, and the effective capacity utilization rate has dropped from 71% to 37%.

- Production in 2022 was 1.41 million mt, and in 2024, it reached 1.84 million mt, with a capacity growth rate of about 31%. Although there is growth, the magnitude is relatively limited compared to capacity expansion, and the production growth trend has been relatively flat over the three years.

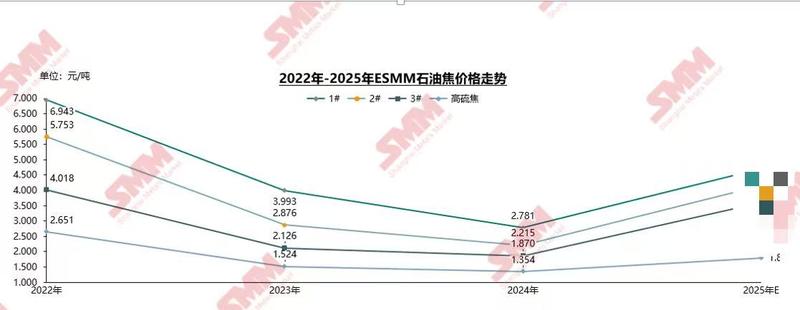

**2024 Petroleum Coke Price Review**

**From September 2024, Low-Sulfur Coke Prices Continued to Rise Supported by Increased Stockpiling Demand**

**SMM Analysis:**

- From January to April 2024, low-sulfur petroleum coke in Northeast China showed an upward trend due to the resumption of the negative electrode material market and increased production schedules of downstream battery factories, leading to rising demand. However, after entering Q2, the execution of downstream orders and the number of new orders of negative electrode enterprises decreased, gradually weakening the demand for petroleum coke procurement. Coupled with the domestic supply surplus, low-sulfur petroleum coke prices began to enter a slight downward fluctuation.

- Starting from the end of Q3 2024, due to the good performance of downstream orders of negative electrode material enterprises, their petroleum coke inventory had dropped to a low level, triggering active stockpiling and restocking. This factor, combined with others, prompted low-sulfur coke prices to turn from decline to rise. Especially in Q1 2025, the concentrated stockpiling during the Chinese New Year holiday and policy interference amplified market expectations, driving a rapid rise in low-sulfur coke prices.

In 2024, the prices of medium and high-sulphur petroleum coke mainly fluctuated, and after entering 2025, the coke prices rose rapidly.

SMM analysis:

ØIn 2024, the prices of medium and high-sulphur petroleum coke in Shandong fluctuated slightly. In Q1, the anode market improved, transactions were active, downstream carbon enterprises were actively purchasing, and prices rose slightly. In Q2, refinery maintenance increased, supply decreased, just-in-time procurement supported prices to rise slightly, and then due to the cooling of procurement sentiment, prices showed a downward trend. In September, local refineries' poor profitability led to an increase in product sulfur content, some enterprises stopped for maintenance, and the supply of medium-sulphur petroleum coke was tight, and prices turned strong. High-sulphur petroleum coke prices rose slightly in Q1 driven by market sentiment, and then fluctuated downward.

ØAfter entering 2025, due to the increase in raw material costs of refineries, some refineries, especially those in Shandong, reduced production, coupled with the Chinese New Year holiday, downstream prebaked anode enterprises concentrated on stockpiling, and petroleum coke prices ushered in explosive growth. The prices of calcined petroleum coke and prebaked anode also rose rapidly with the rise in raw material petroleum coke prices. As of April, the procurement price of prebaked anode of benchmark enterprises rose to 5,205 yuan/mt, an increase of 29% compared with the beginning of the year.

2025 Petroleum Coke Price Forecast

2025 Price Influencing Factors

►Macro and Policy Aspects

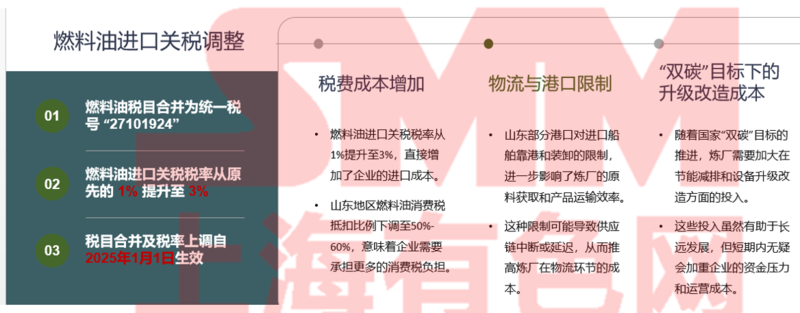

1. Import Tariff Adjustment

From January 2025, the import tariff rate of fuel oil will be increased from the original 1% to 3%, and the fuel oil consumption tax deduction ratio in Shandong will also be significantly reduced from full deduction to the range of 50-60%. From April 12, 2025, a 125% tariff will be imposed on all imported goods originating from the US, and the import tariff will be increased from 3% to 128%.

2. Energy Saving and Carbon Reduction Policy

The "dual carbon" target promotes environmental protection upgrades and tax standardization, and the environmental protection and compliance requirements of local refineries are improved. Shandong Province plans to reduce the crude oil processing capacity of the local refining industry from 130 million mt/year to around 90 million mt/year by 2025, a reduction of 30%, and eliminate backward capacity through integration and other means. In 2024, multiple national departments required the elimination of atmospheric and vacuum units of 2 million mt/year and below, and more than 20% of such units in Shandong were affected.

►Fundamentals

3. Domestic Petroleum Coke Supply

In 2025, there is no plan to add new delayed coking units in China, and the shutdown and maintenance of delayed coking units in refineries are frequent during the year. The loss of maintenance in April-May has increased significantly, coupled with the impact of consumption tax on profit margins, the capacity utilization rate of delayed coking has declined. Based on the above information, the domestic petroleum coke supply is expected to decline in 2025.

4. Petroleum Coke Import Situation

The US is the largest source of petroleum coke imports in China. The import tariff of US coke has been increased layer by layer, and the cost has increased seriously. The total import of US petroleum coke is expected to decrease by 30%-40%. Overall, the import of petroleum coke in 2025 is expected to increase YoY, but the increase is limited, and the tight supply pattern of petroleum coke is difficult to change.

5. Domestic Petroleum Coke Demand

The demand of the aluminum industry is steadily increasing, providing stable support for petroleum coke demand. The demand of emerging new energy fields such as anode materials and PV polysilicon is growing rapidly, becoming an important force to boost petroleum coke demand. However, the demand of some traditional industries, such as the glass industry, is shrinking, and the demand of the silicon metal industry is mediocre. The market demand structure of petroleum coke is continuously reshaping, and the proportion of new energy-related fields is increasing.

Macro fundamentals are favorable for the rise of petroleum coke prices, and the price center of petroleum coke in 2025 will obviously move upward.

SMM analysis:

ØOverall, in the short term, the tight supply and demand situation of petroleum coke is difficult to alleviate, and the probability of price increase is high. From April, the expectation of import contraction has strengthened, coupled with the domestic refineries entering the concentrated maintenance period, and the price has shown an upward trend. In the medium and long term, the new capacity of domestic petroleum coke is less and the expectation of local refinery capacity withdrawal, the supply-demand imbalance has intensified, the dependence on imports has continued to increase, and import obstruction or cost increase will significantly increase the price of petroleum coke.

ØHowever, the price trend also faces some uncertain factors, such as if the macroeconomic situation recovers slowly, the recovery time of the consumption demand of physical enterprises and industrial terminals will be longer, which may inhibit the price increase; if the coal market and related policies change, it will also have an indirect impact on the price of petroleum coke.

》Click to view the special report of AICE 2025 SMM (20th) Aluminum Industry Conference and Aluminum Industry Expo