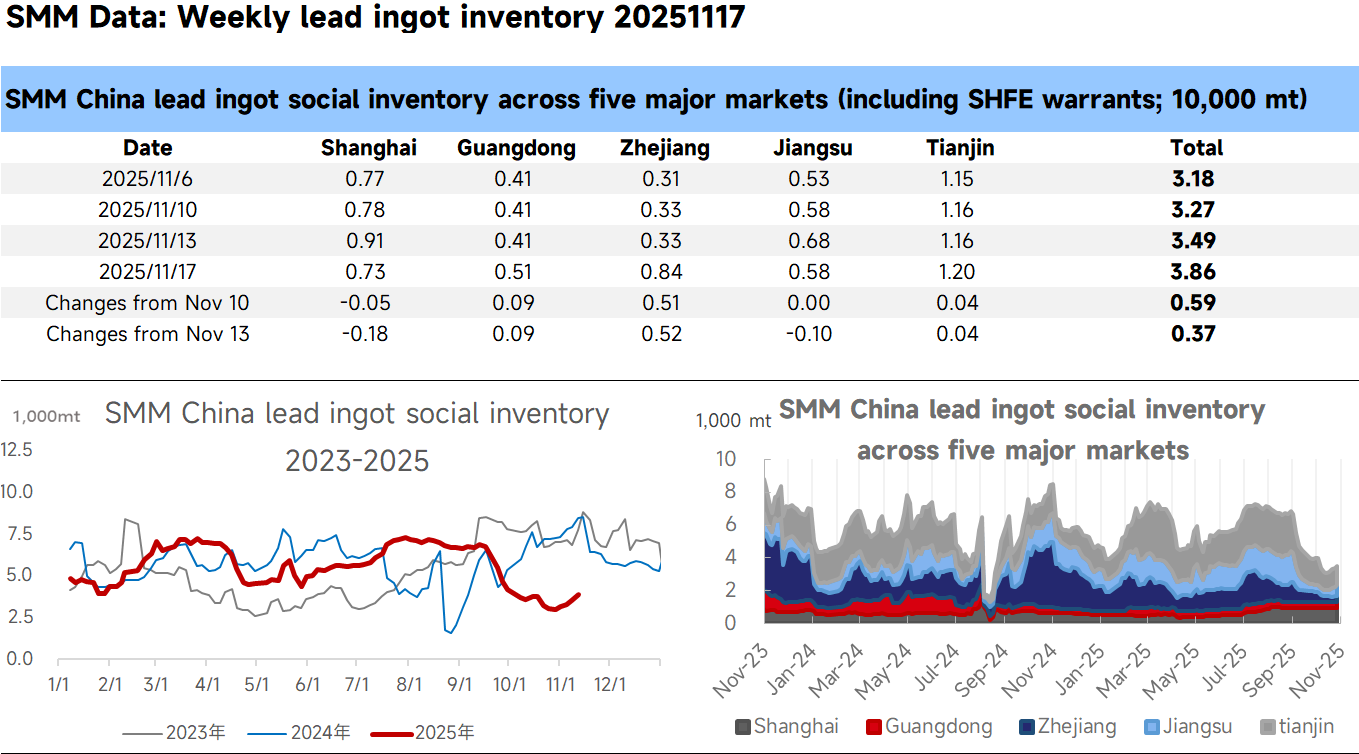

Today marked the delivery date for the SHFE lead 2511 contract, with delivery lead ingots being moved into warehouses over the weekend, leading to another rise in social inventory. However, inventories in some warehouses near consumption areas declined during this period, primarily due to last week’s sharp surge in lead prices, which prompted some downstream enterprises to use originally planned delivery lead ingots for actual production. This week, primary lead and secondary lead enterprises experienced mixed production trends. In north China, vehicle transportation was restricted due to air quality control measures, and winter scrap shortages led to reduced output at some secondary lead enterprises. Meanwhile, in east China, primary lead enterprises resumed supply after maintenance, widening the supply disparity between the northern and southern regions. After the front-month contract delivery is completed, the growth in lead ingot social inventory may slow down.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM’s internal database model. The data are for reference only and do not constitute decision-making advice.