》View SMM metal quotes, data, and market analysis

》Subscribe to view historical price trends of SMM metal spot cargo

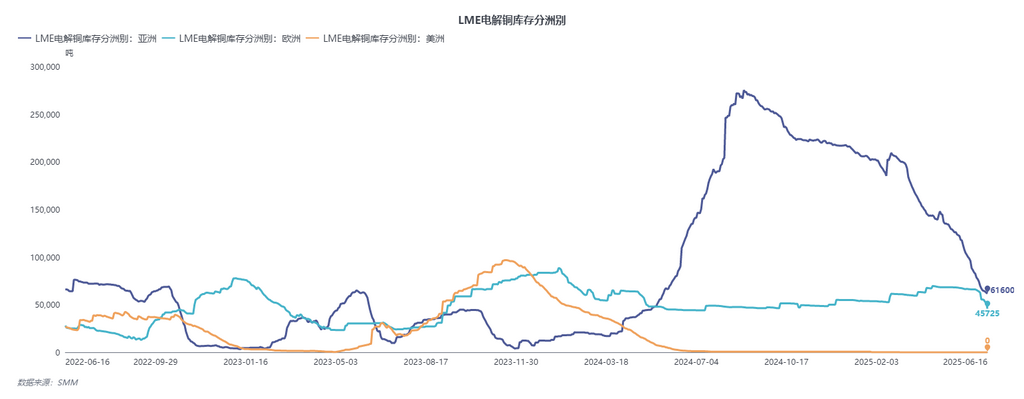

It is observed that even though domestic smelters have already planned for exports amid significant losses in the import window recently, LME inventory is still rapidly destocking, with the largest destocking occurring in Asian warrants. Given the substantial imports and exports, is the supply in the domestic spot market tight or loose?

As can be observed from the chart above, LME inventory is accelerating its destocking process. While this is partly due to the US absorbing copper cathode, during the brief period when the SHFE copper import window against LME was profitable, traders significantly canceled LME warrants and continuously shipped them to China. Subsequently, copper prices briefly surged, supported by macro factors and the widening of the BACK structure in both LME and SHFE. The SHFE/LME price ratio weakened, prompting smelters to start planning for export opportunities. According to SMM's estimates, copper cathode exports in June may reach 70,000 mt.

Currently, copper prices are fluctuating rangebound, and social inventory continues to destock, with downstream consumption remaining resilient. At present, smelters are exporting deliverable domestic cargo, while imported cargo is mostly non-registered from Russia and Africa. The main circulating and deliverable cargo in the market is relatively tight, so downstream buyers tend to purchase copper cathode at lower prices when premiums decline.

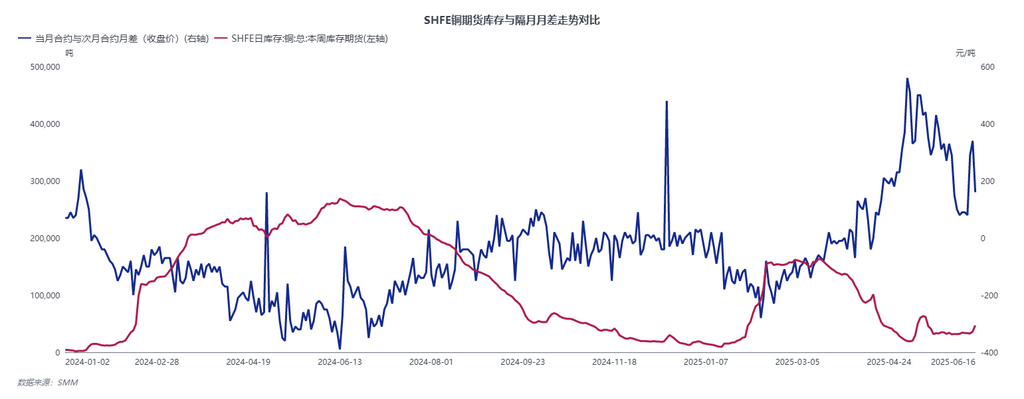

Having just experienced the contract rollover and delivery of SHFE copper 2506, in addition to warrants matching the delivery, there are still excess warrants that will be released in advance. Moreover, with concentrated arrivals of Russian cargo recently, the overall market supply is not tight. After entering the SHFE copper 2507 contract, spot suppliers will start quoting at premiums of 200-300 yuan/mt. However, continuous import shocks make it difficult for suppliers to achieve high premiums, and it is expected that spot premiums will be quoted high but fall in the future. It is worth noting that in the past two months, when approaching delivery, C.Steinweg's futures warrants at Waigaoqiao have remained at a high level, with some cargo originating from bonded warrants converted to SHFE futures warrants, but the outflow speed is slow.

Overall, with sustained imports, the market supply is not tight, but this is limited to low-priced cargo (non-registered or non-deliverable cargo). The supply of exportable smelter cargo, long-term contract cargo circulating in the trade market, and cargo from Chile and other places will remain tight, presenting relatively high premiums.

》View SMM metal industry chain database