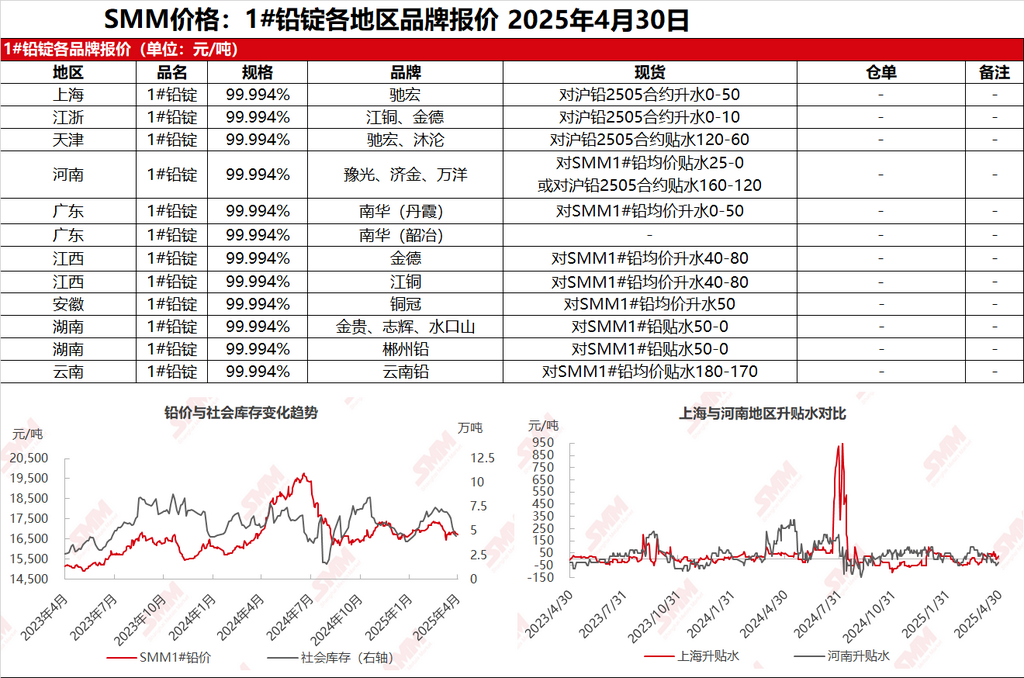

SMM News on April 30: In the Shanghai market, Chihong lead was quoted at 16,875-16,895 yuan/mt, with premiums of 30-50 yuan/mt against the SHFE lead 2505 contract. In Jiangsu and Zhejiang regions, JCC and Jinde lead were quoted at 16,845-16,870 yuan/mt, with premiums of 0-10 yuan/mt against the SHFE lead 2505 contract. SHFE lead prices were consolidating at a weak level, with suppliers adjusting their quotes accordingly. A few suppliers had suspended quoting due to the approaching holiday. During this period, discounts for cargoes self-picked up from primary lead smelters widened, with mainstream producing areas quoting at discounts of 220-100 yuan/mt ex-factory against the SHFE lead 2506 contract. Secondary lead smelters had varying shipping volumes, with some standing firm on quotes and reluctant to sell, while others were offloading cargoes. Secondary refined lead was quoted at discounts of 100 yuan/mt to premiums of 50 yuan/mt ex-factory against the SMM 1# lead average price. Downstream enterprises gradually entered holiday mode, with fewer inquiries. However, some enterprises still purchased on dips as needed, and spot market transactions showed regional differences.

Other markets: Today, the SMM 1# lead price fell by 75 yuan/mt from the previous trading day. Traders in Henan quoted at discounts of 160-120 yuan/mt against the SHFE lead 2506 contract. Smelters in Jiangxi quoted at premiums of 50-80 yuan/mt ex-factory against the SMM 1# lead average price. Smelters in Hunan quoted at discounts of 50-0 yuan/mt ex-factory against the SMM 1# lead average price, while traders quoted at discounts of 220-150 yuan/mt against the 2506 contract. With lead prices falling, some downstream enterprises intended to purchase on dips and did so as needed. However, more downstream enterprises are expected to take the Labour Day holiday, with few inquiries and sluggish spot order market transactions.