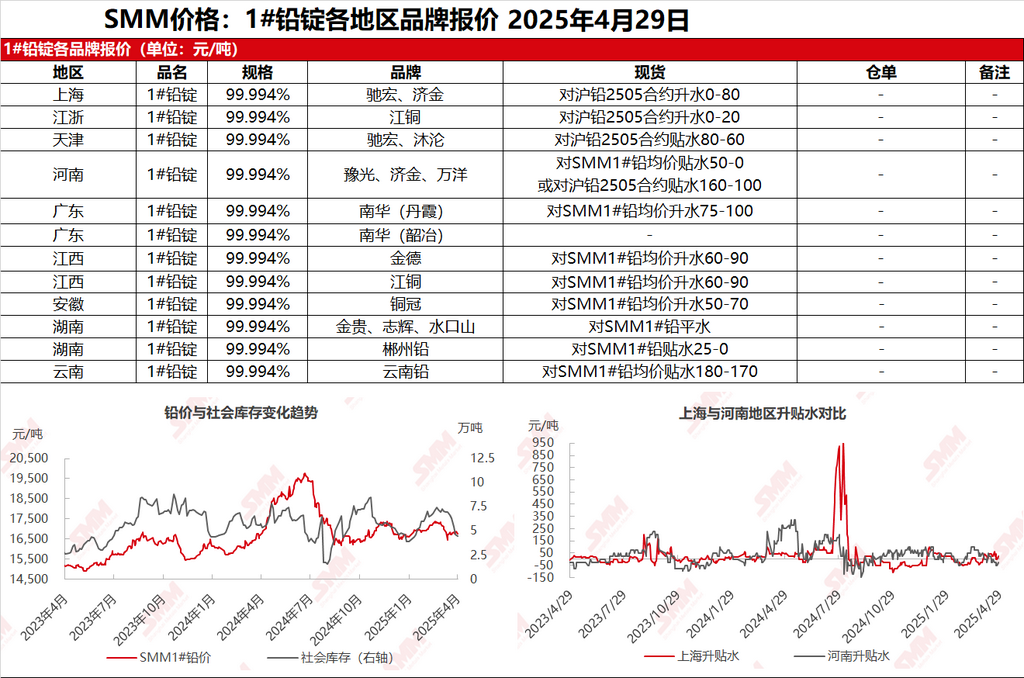

SMM News on April 29: In the Shanghai market, Chihong lead was priced at 16,975-17,005 yuan/mt, quoted at premiums of 50-80 yuan/mt against the SHFE lead 2505 contract. Jijin lead was priced at 16,925-16,945 yuan/mt, quoted at premiums of 0-20 yuan/mt against the SHFE lead 2505 contract. In the Jiangsu, Zhejiang, and Shanghai region, Jinde lead was priced at 16,925-16,945 yuan/mt, quoted at premiums of 0-20 yuan/mt against the SHFE lead 2505 contract. SHFE lead maintained high-level consolidation. With the approaching Labour Day holiday, suppliers were actively quoting and shipping. The spot premiums/discounts in the Jiangsu, Zhejiang, and Shanghai region showed relatively small differences compared to the previous day. However, there were significant discrepancies in the quotes for cargoes self-picked up from primary lead smelters. The mainstream production quotes were at discounts of 170-40 yuan/mt against the SHFE lead 2506 contract for ex-factory delivery. Additionally, many secondary lead smelters had implemented production cuts and were generally standing firm on quotes for shipping. Secondary refined lead was quoted at discounts of 50-0 yuan/mt against the SMM 1# lead average price for ex-factory delivery. Downstream enterprises, considering the approaching holiday and the low level of purchases at month-end, along with limited inquiries, saw sluggish trading in the spot order market.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, traders quoted at discounts of 160-100 yuan/mt against the SHFE lead 2506 contract, with sluggish spot transactions. In Hunan, smelters quoted at discounts of 25-0 yuan/mt against the SMM 1# lead average price for ex-factory delivery, while traders quoted at discounts of 170-100 yuan/mt against the 2506 contract. With the approaching Labour Day holiday for downstream enterprises, some had already suspended procurement. The pre-holiday atmosphere was strong in the spot market, and market transactions slowed down.