The local prices are expected to be released soon, stay tuned!

Got it

+86 021 5155-0306

Language:

SMM

Sign In

Base Metals

Aluminum

Copper

Lead

Nickel

Tin

Zinc

New Energy

Solar

Lithium

Cobalt

Lithium Battery Cathode Material

Anode Materials

Separator

Electrolyte

Lithium-ion Battery

Sodium-ion Battery

Used Lithium-ion Battery

Hydrogen Energy

Energy Storage

Minor Metals

Silicon

Magnesium

Titanium

Bismuth/Selenium/Tellurium

Tungsten

Antimony

Chromium

Manganese

Indium/Germanium/Gallium

Niobium/Tantalum

Other Minor Metals

Precious Metals

Rare Earth

Gold

Silver

Palladium

Platinum/Ruthenium

Rhodium

Iridium

Scrap Metals

Copper Scrap

Aluminum Scrap

Tin Scrap

Ferrous Metals

Iron Ore Index

Iron Ore Price

Coke

Coal

Pig Iron

Steel Billet

Finished Steel

International Steel

Others

Futures

SMM Index

MMi

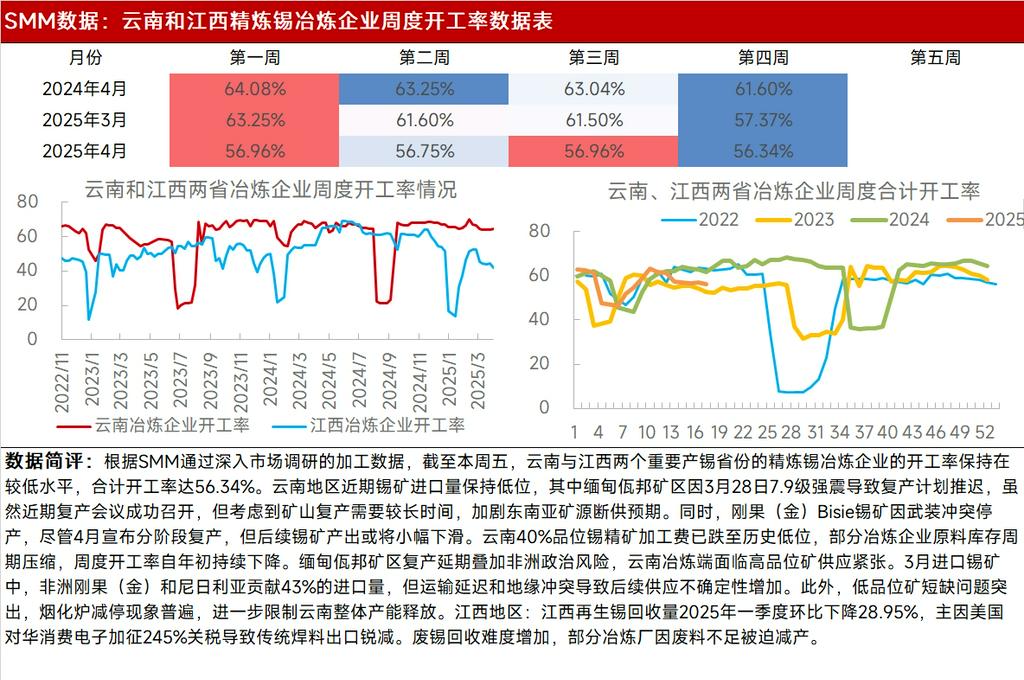

【SMM Analysis】The operating rates of refined tin smelters in Yunnan and Jiangxi remained low, with raw material shortages continuing to impact the smelting sector.

Apr 25, 2025, at 4:25 pm

【SMM Analysis: Operating Rates of Refined Tin Smelters in Yunnan and Jiangxi Remain Low, Raw Material Shortages Continue to Impact Smelting Sector】: According to SMM's in-depth market survey data on processing, as of this Friday, the operating rates of refined tin smelters in Yunnan and Jiangxi, two major tin-producing provinces, remained at low levels, with a combined operating rate of 56.34%. Recent tin ore imports in Yunnan have stayed low, with the Wa State mining area in Myanmar delaying its production resumption plans due to a 7.9-magnitude earthquake on March 28. Although a recent resumption meeting was successfully held, considering the extended time required for mine resumption, expectations of supply disruptions from Southeast Asian sources have intensified. Meanwhile, the Bisie tin mine in the DRC halted production due to armed conflict, and despite announcing phased resumption in April, subsequent tin ore output may slightly decline. The processing fees for 40% grade tin concentrates in Yunnan have fallen to historical lows, compressing raw material inventory cycles for some smelters, and weekly operating rates have continued to decline since the beginning of the year. The delayed resumption in the Wa State mining area, coupled with political risks in Africa, has led to tight supply of high-grade ore for Yunnan's smelting sector. In March, the DRC and Nigeria contributed 43% of tin ore imports, but transportation delays and geopolitical conflicts have increased uncertainty in future supply. Additionally, the shortage of low-grade ore is prominent, with widespread reductions and shutdowns of fuming furnaces, further limiting the overall capacity release in Yunnan.