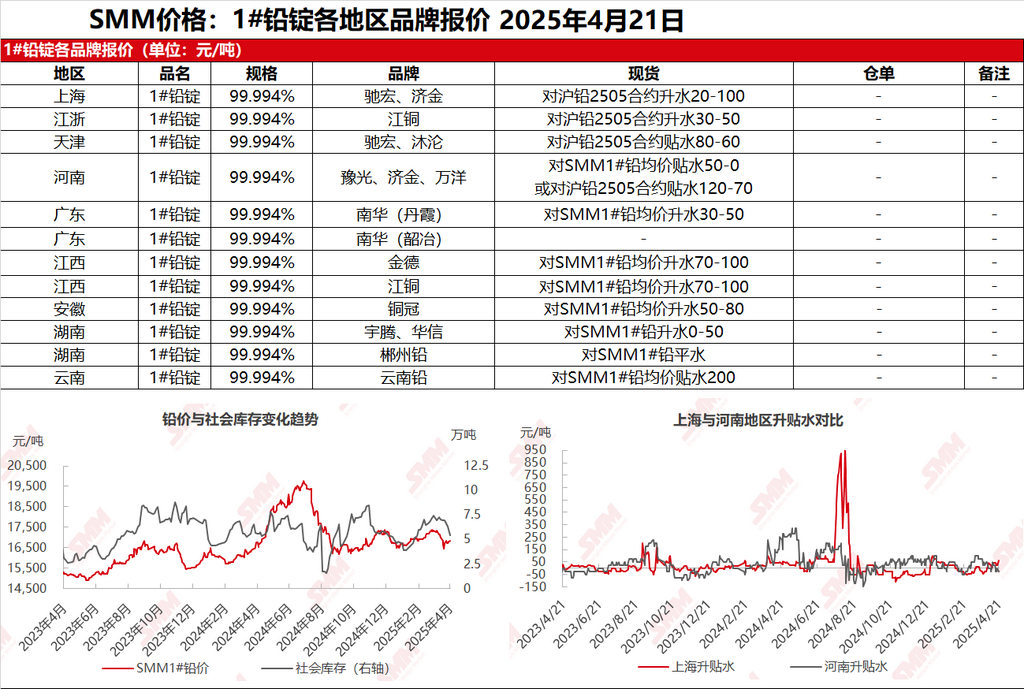

SMM April 21: In the Shanghai market, Chihong lead was quoted at 17,000-17,020 yuan/mt, with premiums of 80-100 yuan/mt against the SHFE 2505 contract. Jijin lead was quoted at 16,940-16,950 yuan/mt, with premiums of 20-30 yuan/mt against the SHFE 2505 contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,950-16,970 yuan/mt, with premiums of 30-50 yuan/mt against the SHFE 2505 contract. SHFE lead continued its upward trend, with suppliers selling at market prices. Warrant cargo quotations remained largely unchanged WoW, while ex-factory quotations for primary lead smelter cargoes widened further. Mainstream production areas quoted primary lead at discounts of 70-120 yuan/mt against the SHFE 2505 contract ex-factory. Secondary refined lead was quoted at discounts of 100-0 yuan/mt against the SMM 1# lead average price ex-factory. Downstream enterprises showed low enthusiasm for month-end purchases, with fewer inquiries, and only some made just-in-time procurement.

Other markets: Today, the SMM 1# lead price rose by 50 yuan/mt compared to the previous trading day. In Henan, smelters mainly shipped under long-term contracts, with suppliers actively quoting and selling at month-end. Primary lead was quoted at discounts of 50-0 yuan/mt against the SMM 1# lead ex-factory. In Hunan, smelters quoted premiums of 25-50 yuan/mt against the SMM 1# lead average price ex-factory, with some suppliers quoting at parity with the SMM 1# lead. Downstream purchases were mainly just-in-time procurement, with relatively strong sentiment for wait-and-see after the lead price strengthened, and overall market transactions were weak.