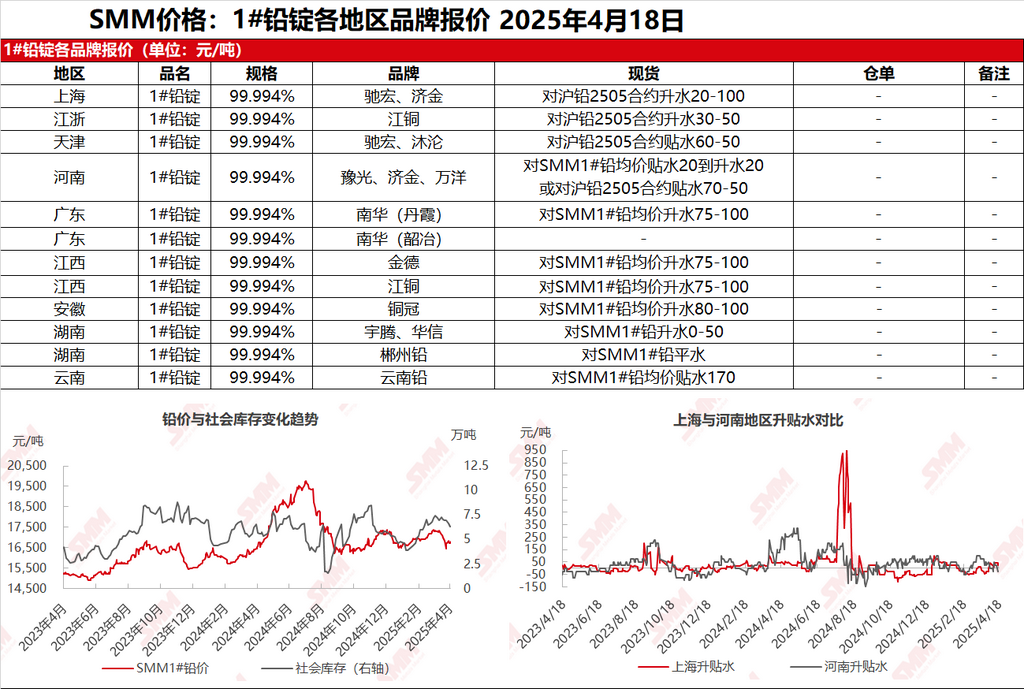

SMM reported on April 18: In the Shanghai market, Chihong lead was quoted at 16,970-16,990 yuan/mt, with premiums of 80-100 yuan/mt against the SHFE 2505 lead contract. Jijin lead was quoted at 16,910-16,920 yuan/mt, with premiums of 20-30 yuan/mt against the SHFE 2505 lead contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,920-16,940 yuan/mt, with premiums of 30-50 yuan/mt against the SHFE 2505 lead contract. SHFE lead fluctuated upward, and suppliers became more active in selling. Warrant supplies were limited, and quotations remained unchanged from the previous day. However, ex-factory quotations for primary lead smelters widened to discounts of 20-50 yuan/mt against the SHFE 2505 lead contract. Meanwhile, secondary lead smelters followed the market trend, with secondary refined lead quoted at discounts of 100-0 yuan/mt ex-factory against the SMM 1# lead average price. Downstream enterprises showed limited inquiries, with only a few making purchases at discounts, resulting in weak market transactions.

Other markets: Today, the SMM 1# lead price increased by 100 yuan/mt compared to the previous trading day. In Henan, smelters mainly shipped under long-term contracts, with some suppliers quoting at parity with the SMM 1# lead or discounts of 50-70 yuan/mt against the SHFE 2505 lead contract. In Hunan, smelters quoted premiums of 25-50 yuan/mt against the SMM 1# lead, but high premiums were relatively difficult to transact. In Yunnan, quotations were at discounts of 170-180 yuan/mt. Lead smelters stood firm on quotes, while downstream enterprises mainly made just-in-time procurement, resulting in sluggish market transactions.