SMM Alumina Morning Comment 4.17

Futures market: In the night session, the most-traded alumina 2505 contract opened at 2,835 yuan/mt, with a high of 2,835 yuan/mt, a low of 2,791 yuan/mt, and closed at 2,816 yuan/mt, up 1 yuan/mt, a gain of 0.04%, with an open interest of 110,000 lots.

Ore side: As of April 16, the SMM imported bauxite index stood at $88.7/mt, flat from the previous trading day; the SMM Guinea bauxite CIF average price was $88/mt, flat from the previous trading day; the SMM Australia low-temperature bauxite CIF average price was $87/mt, flat from the previous trading day; the SMM Australia high-temperature bauxite CIF average price was $81/mt, flat from the previous trading day.

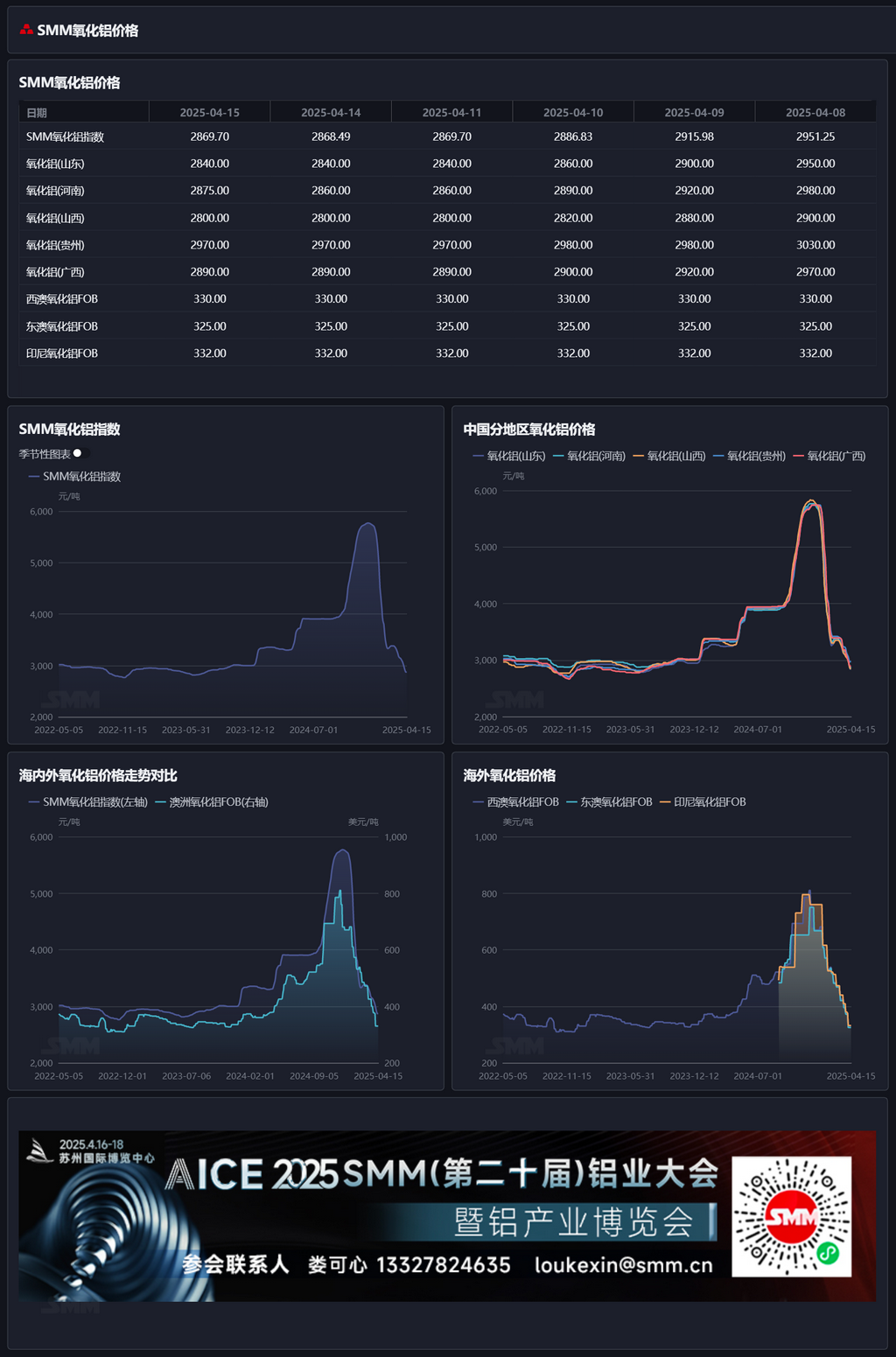

Spot-futures price spread report: According to SMM data, on April 16, the SMM alumina index was at a premium of 66 yuan/mt against the most-traded contract's latest transaction price at 11:30 am. Warrant report: On April 16, the total registered alumina warrant volume increased by 3,896 mt to 295,200 mt compared to the previous trading day, with Shandong region's total registered alumina warrant volume flat at 3,307 mt, Henan region's total registered alumina warrant volume decreased by 1,201 mt to 12,000 mt, Guangxi region's total registered alumina warrant volume decreased by 4,204 mt to 43,200 mt, Gansu region's total registered alumina warrant volume flat at 17,100 mt, and Xinjiang region's total registered alumina warrant volume increased by 9,301 mt to 219,500 mt.

Overseas market: As of April 16, 2025, the FOB Western Australia alumina price was $330/mt, the ocean freight rate was $21.10/mt, and the USD/CNY exchange rate selling price was around 7.34, translating to a domestic mainstream port selling price of approximately 2,992 yuan/mt, 122 yuan/mt higher than the domestic alumina price, keeping the alumina import window closed.

Summary: Last week, alumina plant maintenance events occurred intensively, with operating capacities of several companies declining; meanwhile, some alumina capacities that started maintenance in March ended their maintenance periods, leading to a slight rebound in operating capacities. Overall, as of last Thursday, the national alumina operating capacity dropped to 84.82 million mt/year, down 1.91 million mt/year from the previous week. As of last Thursday, the aluminum operating capacity increased to 43.9 million mt/year, with the theoretical alumina demand operating capacity at 84.51 million mt/year, tightening alumina supply in the short term. However, last week, alumina raw material inventories at aluminum plants totaled 2.67 million mt, up 50,000 mt from the previous week; combined with alumina inventories at delivery warehouses nearing 300,000 mt, alumina inventory pressure remains, and prices may struggle to rebound significantly in the short term, with alumina prices likely to remain in the doldrums in the short term.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this to replace independent judgment. Any decisions made by clients are unrelated to SMM.]