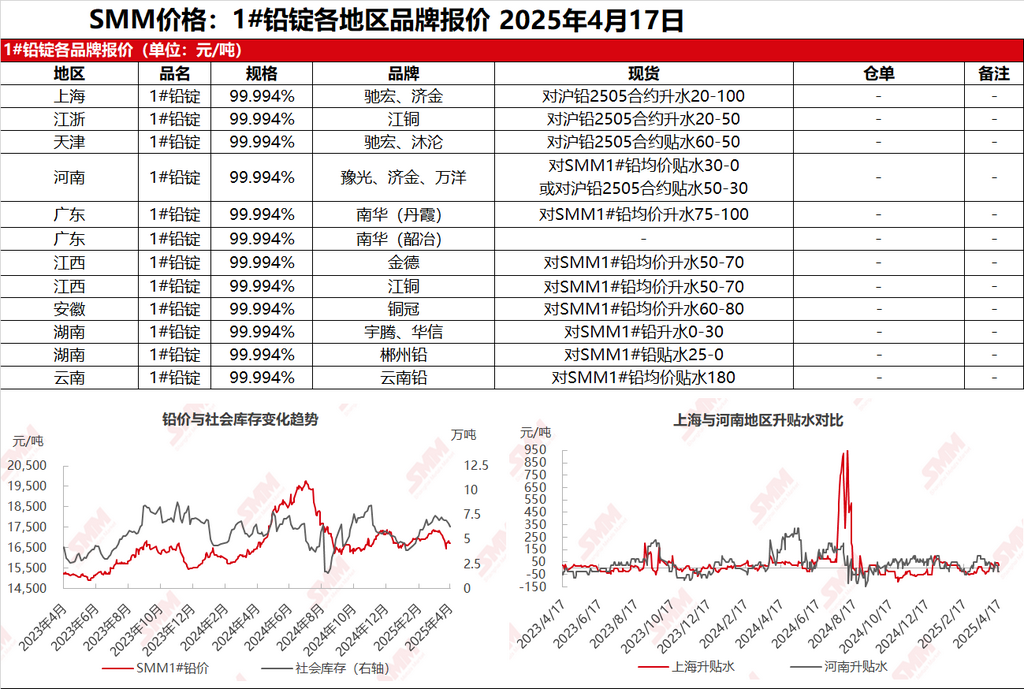

SMM April 17: In the Shanghai market, Chihong lead was quoted at 16,830-16,850 yuan/mt, with premiums of 80-100 yuan/mt against the SHFE 2505 lead contract. Jijin lead was quoted at 16,770-16,780 yuan/mt, with premiums of 20-30 yuan/mt against the SHFE 2505 lead contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,780-16,800 yuan/mt, with premiums of 30-50 yuan/mt against the SHFE 2505 lead contract. SHFE lead maintained a consolidation trend, with suppliers quoting prices in line with the market, and the number of quotations increased compared to the previous day. Primary lead smelters sold cargoes self-picked up from production site at parity (against the SMM 1# lead average price). The divergence in shipments from secondary lead smelters widened, with some standing firm on quotes and reluctant to sell. Secondary refined lead was quoted at premiums of 0-50 yuan/mt against the SMM 1# lead average price, while more companies chose to expand discounts, with secondary refined lead quoted at discounts of 100-50 yuan/mt against the SMM 1# lead average price ex-factory. Downstream buyers made just-in-time procurement based on demand, and there was no significant improvement in spot order market transactions.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, smelters mainly shipped under long-term contracts, with some suppliers quoting at discounts of 30-0 yuan/mt against the SMM 1# lead average price, or at discounts of 50-30 yuan/mt against the SHFE 2505 lead contract. In Hunan, smelters quoted at premiums of 0-25 yuan/mt against the SMM 1# lead average price. In Yunnan, quotations were at a discount of 180 yuan/mt. Lead prices were in a sideways consolidation, with the most-traded SHFE lead contract slightly recovering. Downstream buyers cautiously watched the market, making limited just-in-time procurement, and market transactions remained sluggish.