The local prices are expected to be released soon, stay tuned!

Got it

+86 021 5155-0306

Language:

SMM

Sign In

Base Metals

Aluminum

Copper

Lead

Nickel

Tin

Zinc

New Energy

Solar

Lithium

Cobalt

Lithium Battery Cathode Material

Anode Materials

Separator

Electrolyte

Lithium-ion Battery

Sodium-ion Battery

Used Lithium-ion Battery

Hydrogen Energy

Energy Storage

Minor Metals

Silicon

Magnesium

Titanium

Bismuth/Selenium/Tellurium

Tungsten

Antimony

Chromium

Manganese

Indium/Germanium/Gallium

Niobium/Tantalum

Other Minor Metals

Precious Metals

Rare Earth

Gold

Silver

Palladium

Platinum/Ruthenium

Rhodium

Iridium

Scrap Metals

Copper Scrap

Aluminum Scrap

Tin Scrap

Ferrous Metals

Iron Ore Index

Iron Ore Price

Coke

Coal

Pig Iron

Steel Billet

Finished Steel

International Steel

Others

Futures

SMM Index

MMi

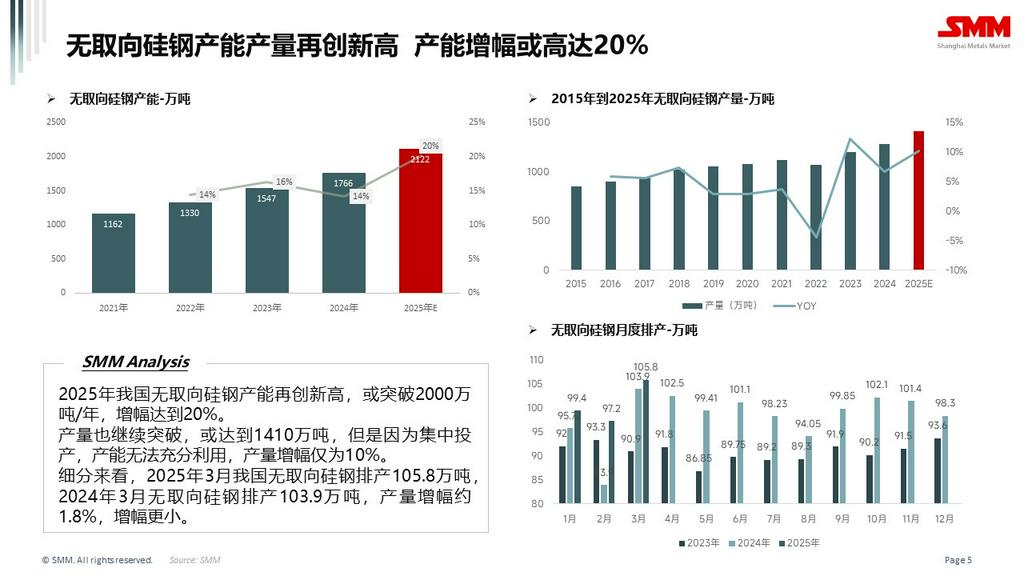

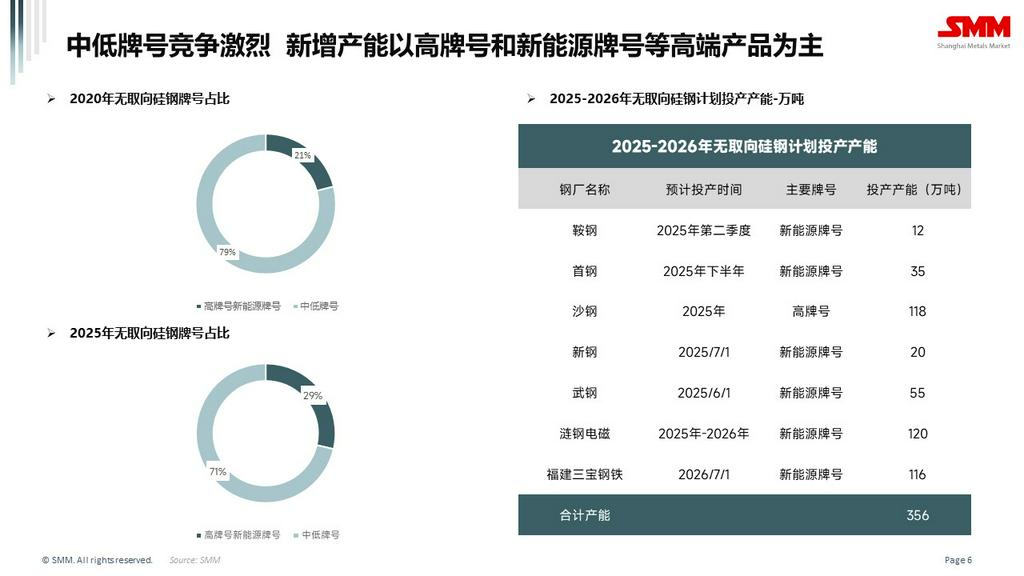

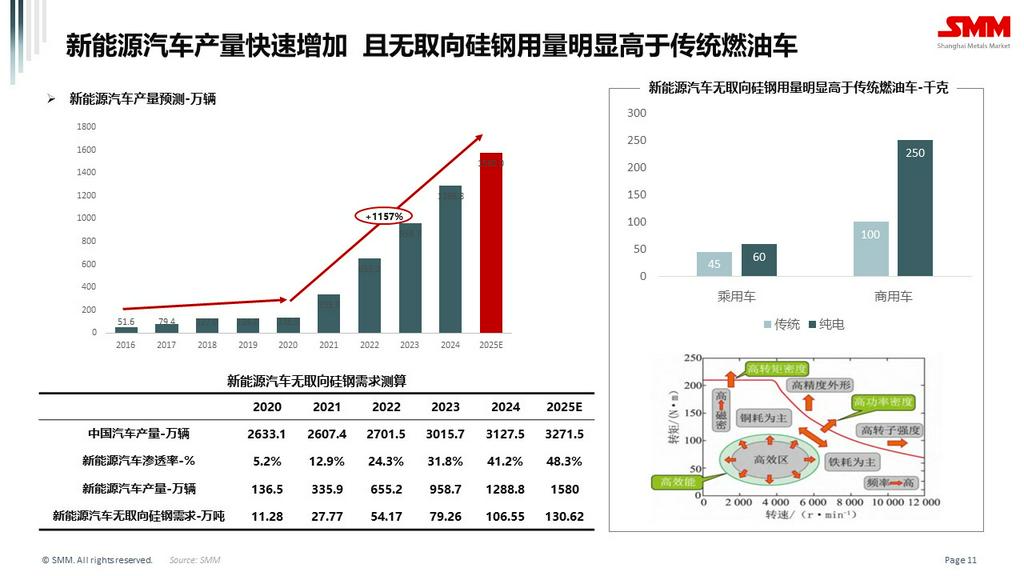

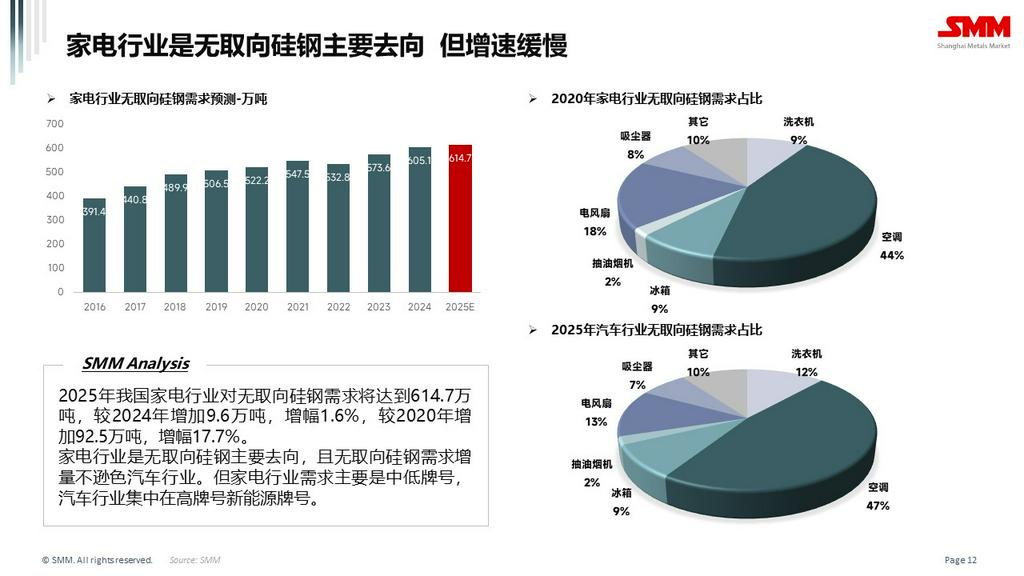

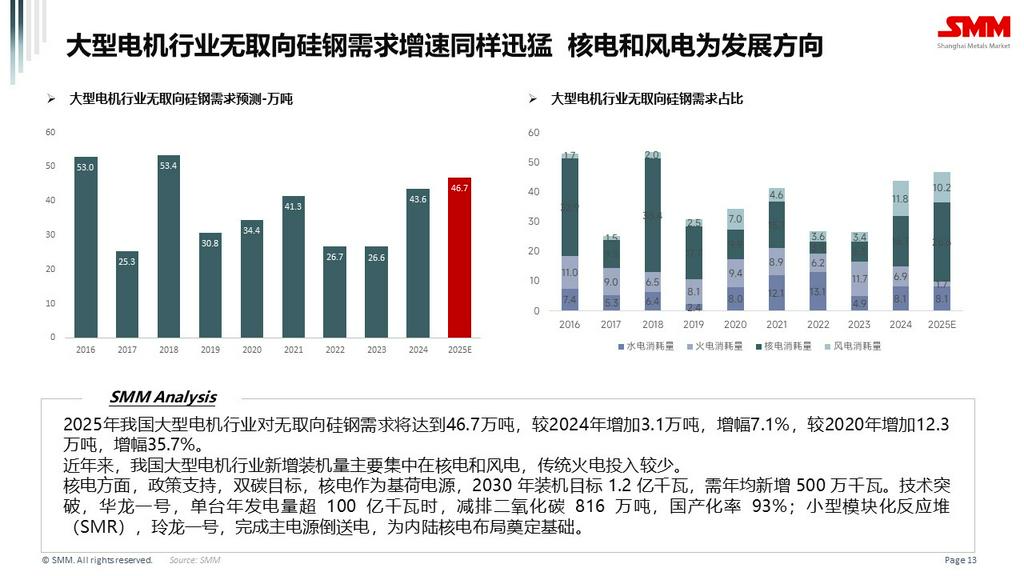

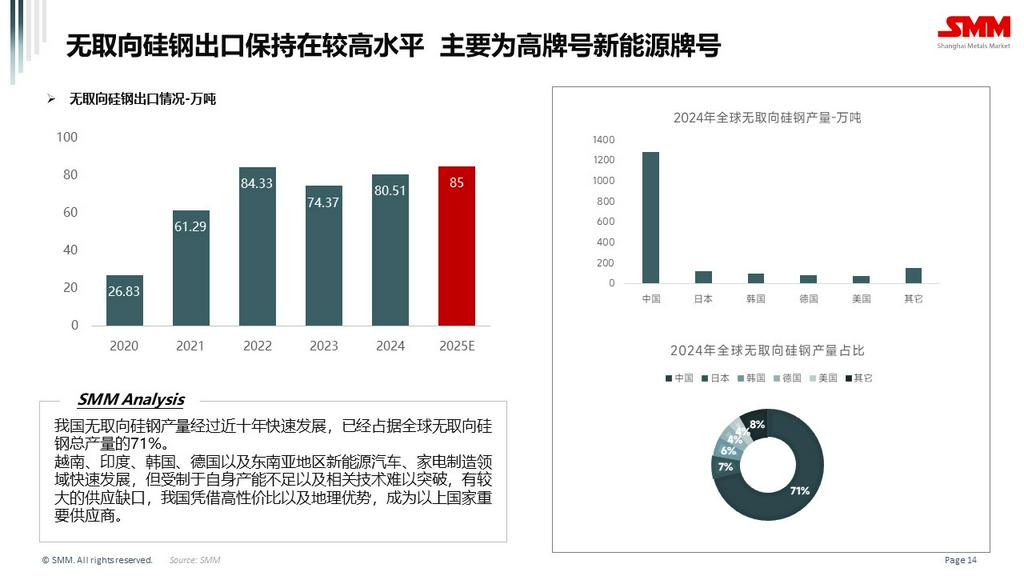

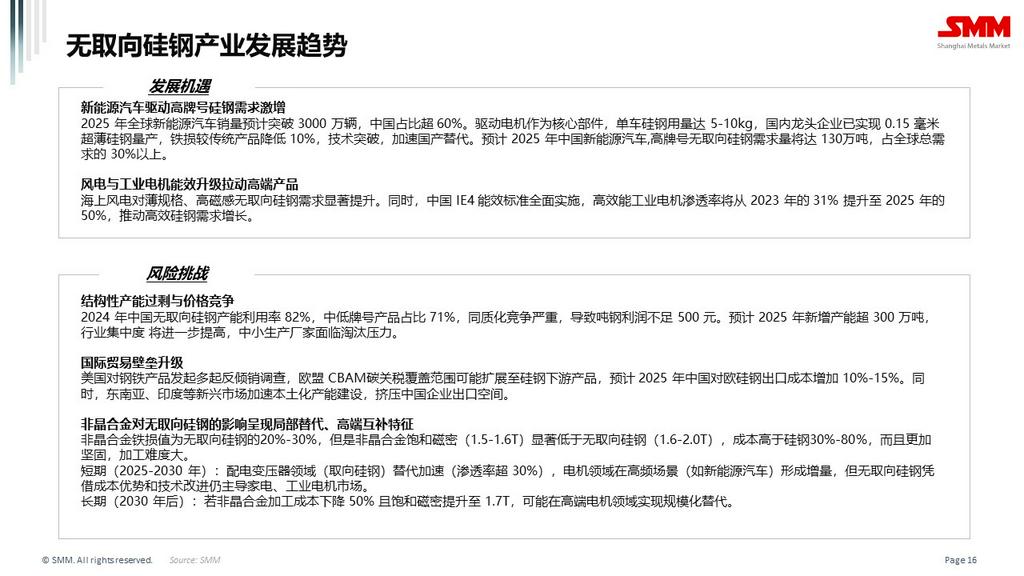

【SMM Analysis】Supply Surplus: The Pressure Path for Non-Oriented Silicon Steel in 2025

Mar 28, 2025, at 11:36 am

【Supply Surplus: The Path of Resistance for Non-Oriented Silicon Steel in 2025】In 2025, the price of non-oriented silicon steel will show a differentiated trend, with high-grade new energy grades remaining stable and medium-low grades weakening. Producers need to address capacity surplus and cost pressure through technological innovation and global layout. In the short term, policy dividends and efficiency demands will support high-grade prices, but medium-low grade market competition is fierce, and prices will gradually approach the cost line. In the long term, technological breakthroughs in alternative materials such as amorphous alloys may reshape the market landscape. Silicon steel producers need to plan ahead to cope with changing situations, otherwise they will face the risk of elimination.

In 2025, the price of non-oriented silicon steel will show a differentiated trend, with high-grade new energy grades remaining stable, while medium and low grades will weaken. Producers need to address capacity surplus and cost pressure through technological innovation and global layout. In the short term, policy dividends and efficiency demands will support high-grade prices, but the medium and low-grade market will face fierce competition, and prices will gradually approach the cost line. In the long term, technological breakthroughs in alternative materials such as amorphous alloys may reshape the market landscape. Silicon steel producers need to plan ahead to cope with changing circumstances, otherwise they will face the risk of being phased out.