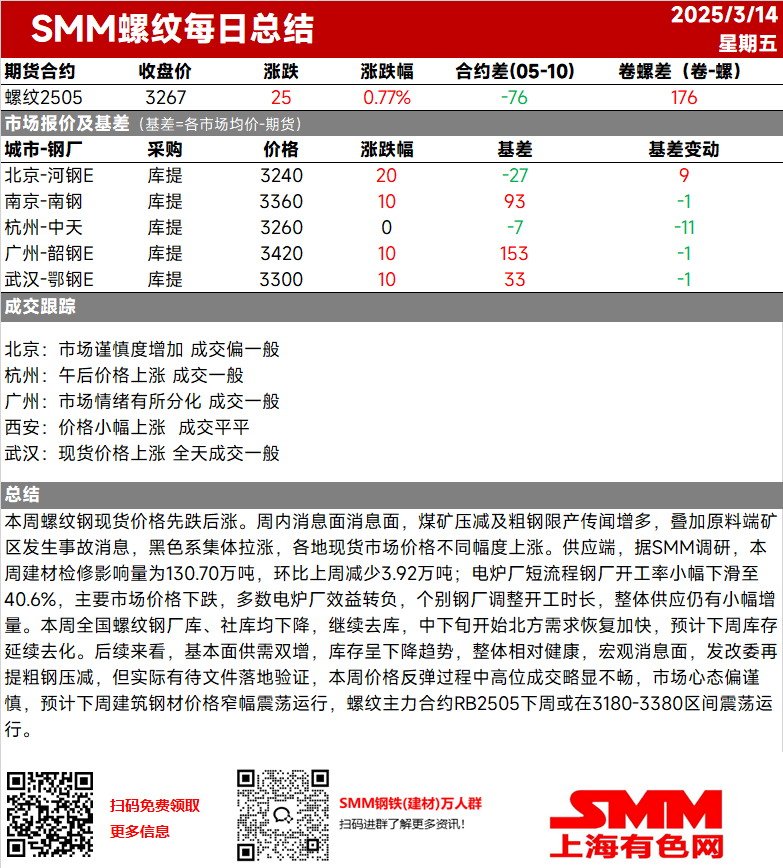

This week, rebar spot prices first declined and then rebounded. During the week, news of coal mine production cuts and crude steel output restrictions increased, coupled with reports of accidents at mining sites, driving a collective surge in the ferrous metals series. Spot market prices in various regions rose to varying degrees.

Supply side, according to the SMM survey, the impact from maintenance on construction steel this week was 1.307 million mt, down 39,200 mt WoW. The operating rate of EAF steel mills slightly declined to 40.6%. With major market prices falling, most EAF steel mills turned unprofitable, and some mills adjusted their operating hours. Overall, supply still saw a slight increase.

This week, both rebar in-plant inventory and social inventory declined, continuing the destocking trend. From mid-to-late this month, demand in northern regions began to recover at a faster pace, and inventory is expected to continue decreasing next week.

Looking ahead, supply and demand fundamentals are expected to increase simultaneously, with inventory showing a downward trend, indicating a relatively healthy overall situation. On the macro front, the NDRC reiterated crude steel production cuts, but actual implementation awaits verification through official documents. During this week's price rebound, high-level transactions were somewhat sluggish, and market sentiment remained cautious. Next week, construction steel prices are expected to fluctuate rangebound, with the most-traded rebar RB2505 contract likely to move within the range of 3,180-3,380.