In February, China's Manufacturing Purchasing Managers' Index (PMI) stood at 49.1%, down slightly by 0.1 percentage points MoM, indicating overall stable economic performance. Changes in sub-indices showed relatively stable market demand in the manufacturing sector, steady market prices, stable operations of large and medium-sized enterprises, and improving business expectations...

- China Passenger Car Association: Retail Sales in the Passenger Car Market Reached 1.397 Million Units in February 2025, Up 26% YoY

According to statistics released by the China Passenger Car Association, retail sales in the passenger car market reached 1.397 million units in February, up 26% YoY but down 22% MoM. Cumulative retail sales for the year reached 3.191 million units, up 1% YoY.

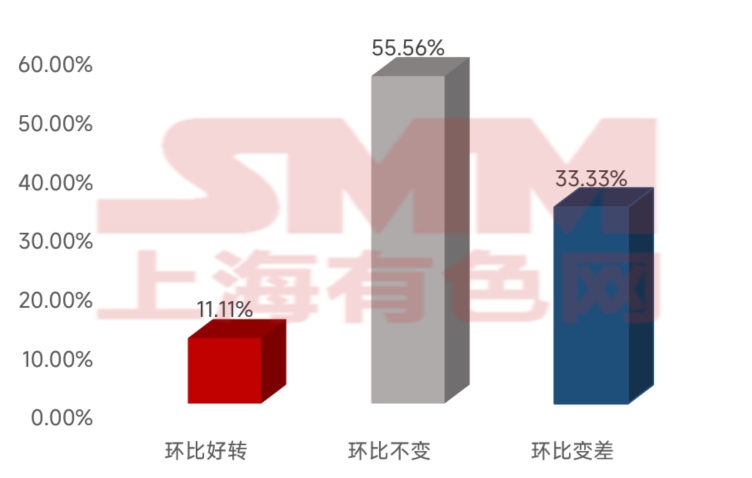

Driven by macroeconomic recovery and the transition to new energy, automakers exhibited significantly divergent market performances, with increasingly fierce competition reshaping the industry landscape. The NEV market continued to expand, with leading automakers consolidating their positions through technological advantages and brand influence. Among the automakers surveyed by SMM,11.11%reported an improvement in new orders MoM in February, 55.56% indicated stable orders compared to January, while the remaining 33.33% reported a decline in orders MoM. One automaker mentioned, "February orders dropped significantly, and it seems that orders will continue to decline in the coming months, similar to last year. Q2 is typically an off-season. Currently, the pace of raw material procurement has also slowed down significantly compared to pre-Chinese New Year levels."

Figure 1: February Order Status of Automakers Surveyed by SMM

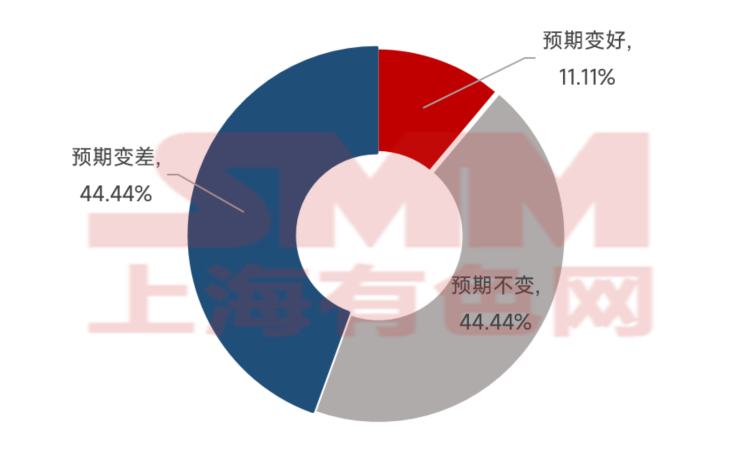

Regarding order expectations for the next three months, among the automakers surveyed by SMM, 44.44% held unchanged or worsening views on future demand, while 11.11% expected an improvement. One automaker stated, "Domestic demand is mainly weak, and orders are expected to decline slightly in the future. The competition is intense, and profits are under pressure. Operating rates in February were average, with demand largely dependent on orders. Automakers produce based on pre-sales and orders."

Figure 2: Three-Month Demand Expectations of Automakers Surveyed by SMM

- According to ChinaIOL data, the combined production schedule for air conditioners, refrigerators, and washing machines in February 2025 totaled 29.14 million units, up 30.6% YoY

The production schedule report for the three major white goods released by ChinaIOL showed that the combined production schedule for air conditioners, refrigerators, and washing machines in February 2025 totaled 29.14 million units, up 30.6% YoY. By product, household air conditioner production reached 15.93 million units, up 35.6% YoY; refrigerator production reached 6.32 million units, up 29.2% YoY; and washing machine production reached 6.89 million units, up 21.3% YoY.

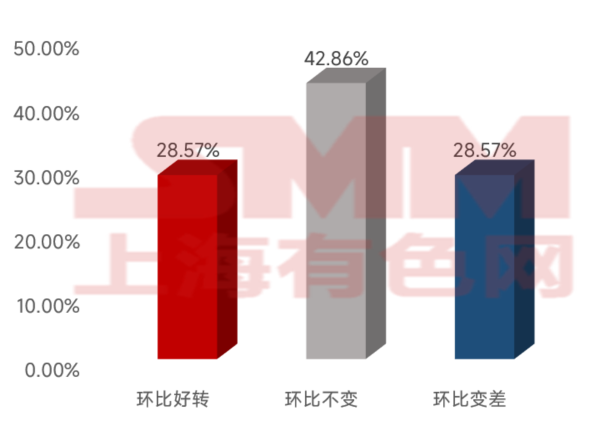

The trade-in policy has partially depleted demand, with high-efficiency product replacement demand concentrated in 2024, which will impact overall shipments in 2025. Among the home appliance enterprises surveyed by SMM, approximately 28.57% reported an improvement in orders MoM in February, 42.86% indicated no change, and the remaining 28.57% reported a decline MoM. A company in Taizhou mentioned, "There are many domestic manufacturers, and competition is fierce. Currently, the entire industry is focused on reducing inventory, with some promotional strategies in place. Sales are expected to improve from mid-March to late April. Last year, domestic trade overall contracted, but this year, the company has set a target of 10-15% growth in domestic trade, and efforts to boost sales must begin in March."

Figure 3: February Order Status of Home Appliance Enterprises Surveyed by SMM

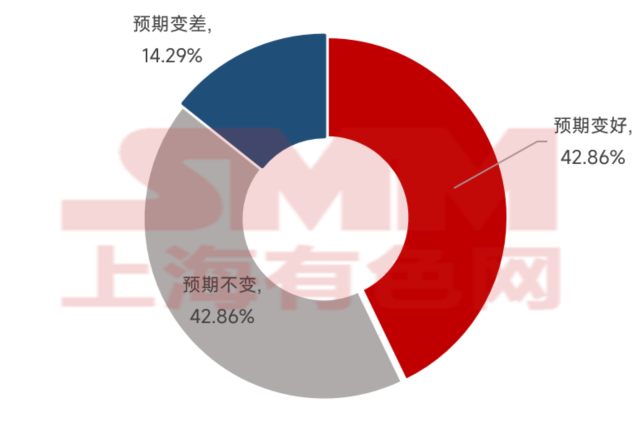

Regarding order expectations for the next three months, among the home appliance enterprises surveyed by SMM, approximately 44.86% expected a slight improvement MoM. Some enterprises believed that overseas markets were still taking orders without significant changes, as it is the peak season. For domestic sales, demand is expected to improve as temperatures gradually rise, leading to increased capacity utilization rates and the start of stockpiling.

Figure 4: Three-Month Demand Expectations of Home Appliance Enterprises Surveyed by SMM

According to the latest production schedule report for the three major white goods released by ChinaIOL, the combined production schedule for air conditioners, refrigerators, and washing machines in March 2025 totaled 40.5 million units, up 7.6% YoY. By product, household air conditioner production reached 24.76 million units, up 13.5% YoY; refrigerator production reached 8.79 million units, up 0.5% YoY; and washing machine production reached 6.95 million units, down 2.1% YoY.

- China Construction Machinery Association: Sales of Excavators Reached 19,270 Units in February 2025, Up Over 50% YoY

According to statistics from the China Construction Machinery Association, sales of excavators reached 19,270 units in February 2025, up 52.8% YoY. In the first two months, a total of 31,782 units were sold, up 27.2% YoY, with exports reaching 14,737 units, up 7.37% YoY. Additionally, the global competitiveness of Chinese excavator manufacturers continued to improve, with export volumes increasing YoY. Overall, excavator sales achieved a strong start this year.

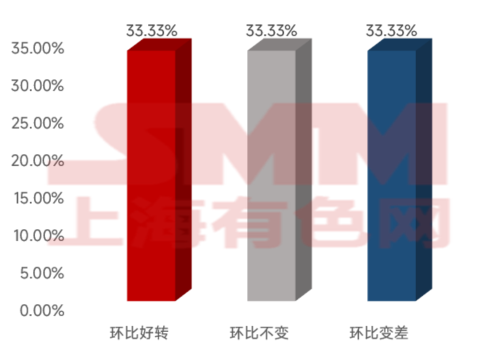

In February 2025, according to SMM survey data, the PMI composite index for the machinery sector was 49.52, up 1.13 MoM and 4.41 YoY. The sector's prosperity continued to decline this month, with production schedules slowing further MoM. Some machinery enterprises resumed operations only in mid-February, resulting in fewer production days. In terms of orders, new orders declined slightly MoM, as the Chinese New Year holiday impacted order-taking. Enterprises mainly focused on fulfilling pre-holiday orders, while bidding results for projects before the holiday were still pending. Overseas market demand remained moderate. Among the machinery enterprises surveyed by SMM, approximately 33.33% reported a decline in orders MoM in January. A machinery enterprise in Sichuan mentioned, "Overall orders in February were not good. After the holiday, bidding results for projects have not yet been announced. Let's see how things go in March; it should be better. March bidding projects should perform better than February."

Figure 5: February Order Status of Machinery Enterprises Surveyed by SMM

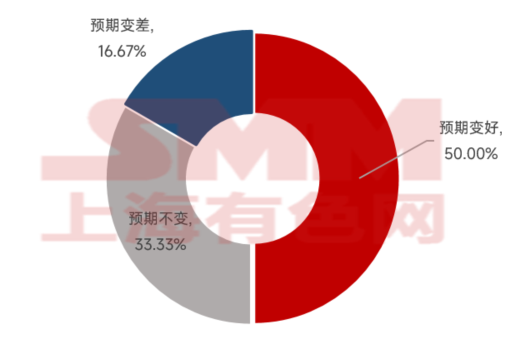

Regarding order expectations for the next three months, among the machinery enterprises surveyed by SMM, 50% expected improvement, 33.33% expected no change, and 16.67% expected a decline. In 2025, driven by economic recovery and technological innovation, the machinery sector is expected to show broad development prospects. From carbon fiber, machine tools, and nuclear power to consumer electronics and humanoid robots, the machinery sector is embracing new growth opportunities. The leading role of key enterprises and the accelerated progress of domestic substitution provide solid support for the industry's development. Moving forward, the machinery sector needs to continue focusing on technological innovation to achieve industrial upgrading and sustainable development.

Figure 6: Three-Month Order Expectations of Machinery Enterprises Surveyed by SMM

- Clarksons: Global New Shipbuilding Orders in February Fell 62% YoY, With Prices for Some Ship Types Starting to Decline

According to Clarksons data, as of the end of February 2025, the Clarksons Newbuilding Price Index stood at 188.36, slightly down from 189.38 in January but still at a high level. The index for February 2024 was 181.39, and for February 2021, it was only 128.43. In February 2025, global shipbuilding orders totaled 50 vessels, or 2.07 million compensated gross tons (CGT), up 16% from January's 1.78 million CGT but down 62% from February 2024's 5.41 million CGT. According to the latest Clarksons data, China secured 1.35 million CGT (37 vessels, 65%) in February, reclaiming the top position. South Korea secured 290,000 CGT (7 vessels, 14%), ranking second. South Korean shipyards saw a significant decline in February compared to January, when they accounted for 62% of global orders (900,000 CGT, 13 vessels), while Chinese shipyards accounted for 19% (270,000 CGT, 21 vessels). In terms of order backlogs, as of the end of February, the global order backlog stood at 156.34 million CGT, down 2.94 million CGT MoM. Among them, Chinese shipyards accounted for 90.75 million CGT (58%), and South Korean shipyards accounted for 36.67 million CGT (23%). Compared to the end of February 2024, Chinese shipyards increased their backlog by 23.54 million CGT, while South Korean shipyards decreased by 2.71 million CGT.

*[Survey Method: Telephone Survey]

*[Sample data is randomly collected nationwide, covering industries such as automobile manufacturing, home appliances, machinery, and shipbuilding, with over 100 samples. The limited sample size may lead to deviations from actual conditions; please interpret with caution.]