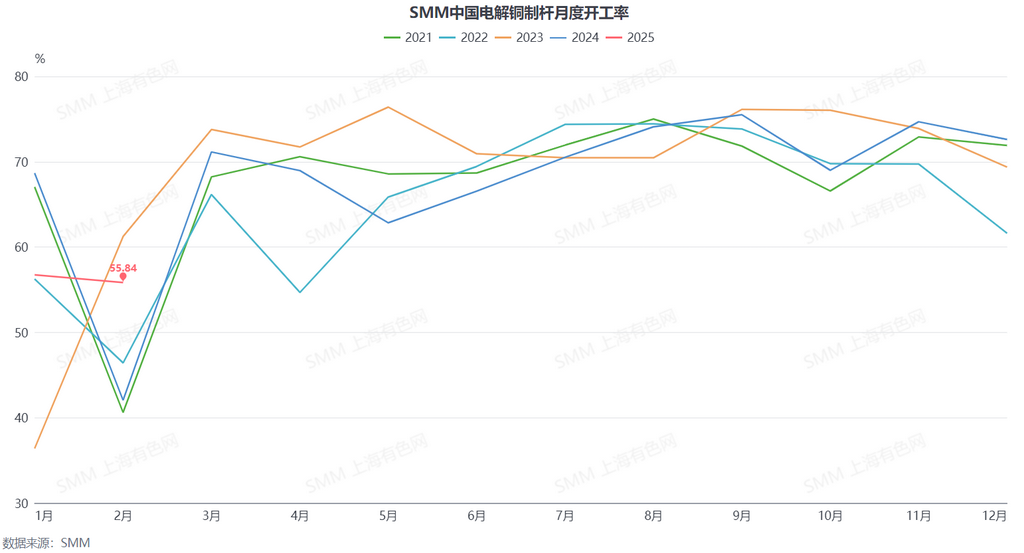

According to SMM, the operating rate of copper cathode rod enterprises in February was 55.84%, down 0.9 percentage points MoM and 2.23 percentage points below the expected value. Based on the lunar calendar, due to differences in the span of the Chinese New Year, the operating rate of copper cathode rod enterprises increased by 13.79 percentage points YoY. Among them, the operating rate of large enterprises was 64.97%, medium-sized enterprises 40.99%, and small enterprises 49.22%.

In February, the operating rate of the copper cathode rod industry recorded 55.84%, up 13.79 percentage points YoY (operating rate in February last year was 42.05%).

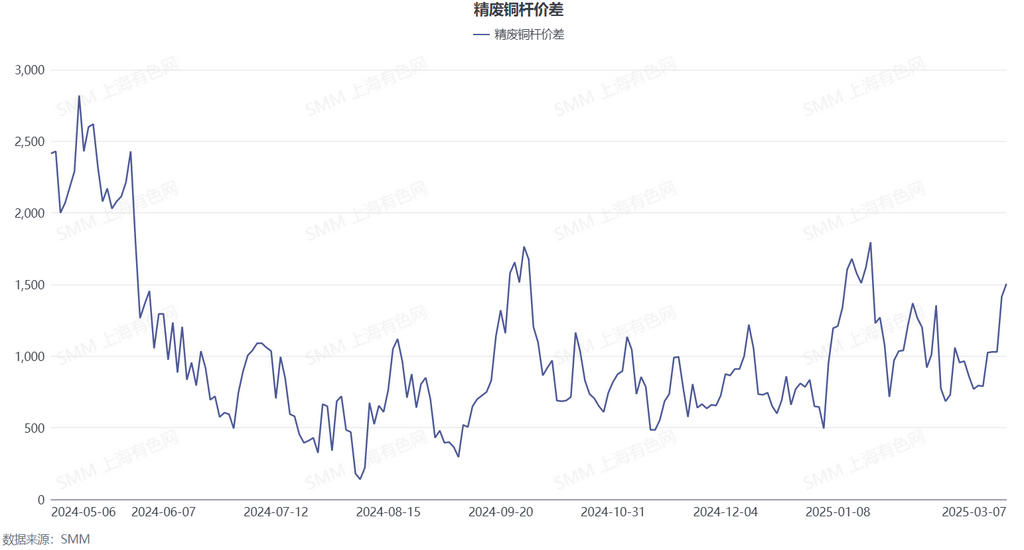

As the festive atmosphere of the Year of the Snake gradually faded, copper prices exceeded market expectations after the holiday due to repeated fluctuations in US tariff expectations. According to SMM data, the average price of SMM #1 copper cathode in February was 76,863.61 yuan/mt, up 1,840 yuan/mt MoM from January. However, due to the post-holiday shortage of secondary copper raw materials, secondary copper prices remained firm, and the price spread between copper cathode rods and secondary copper rods failed to widen significantly. According to SMM statistics, in February, the average price spread between secondary copper rods in Jiangxi and copper cathode rods for power use in east China was 987 yuan/mt, narrowing by 231 yuan/mt MoM. Copper cathode rods maintained an economic advantage. Although the price spread between copper cathode rods and secondary copper rods narrowed, the surge in copper prices exceeded the psychological price level of downstream enterprises, significantly suppressing post-holiday cargo pick-up. Only some new energy and high-end product orders recovered well, while cable orders showed no significant rebound, and end-use consumption remained weak compared to the same period. In February 2025, the operating rate of copper cathode rod enterprises declined both MoM and compared to the expected value.

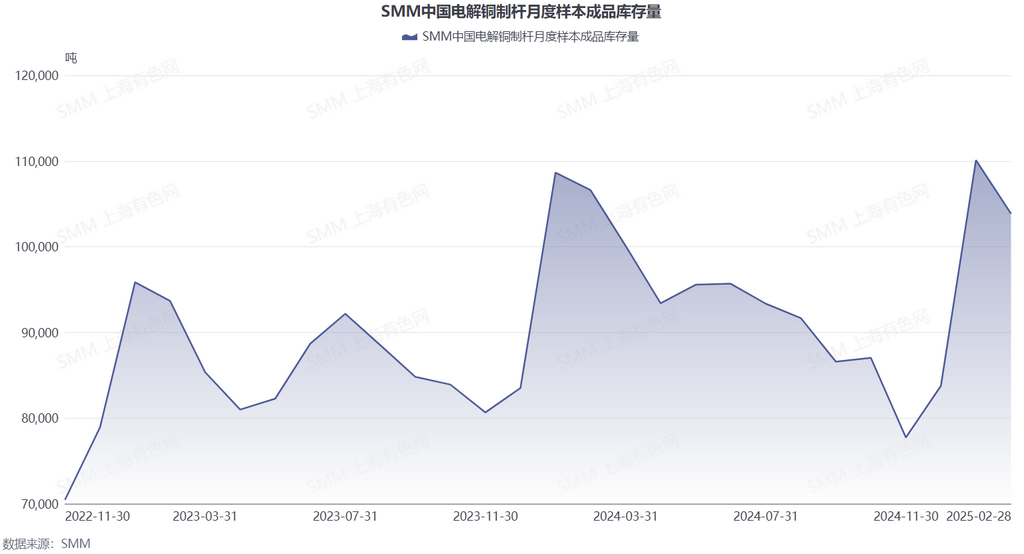

In February, the raw material inventory/output ratio of copper cathode rod enterprises was 11.72%, and the finished product inventory/output ratio was 15.46%.

During the statistical period, as the holiday impact gradually faded, although many copper cathode rod enterprises still faced inventory buildup pressure, with consumption slowly improving and adjustments in capacity utilisation rates, the finished product inventory/output ratio of copper cathode rod enterprises in February decreased by 0.67 percentage points MoM. Due to the current premium structure, the raw material inventory/output ratio increased by 1.68 percentage points MoM.

The operating rate of copper cathode rod enterprises in March is expected to reach 71.25%.

In March, as the US dollar index continued to decline, copper prices rose steadily under the influence of tariff disruptions and other factors, fluctuating at highs. The high copper prices continued to suppress the release of new orders, and downstream consumption showed no signs of sustainable recovery. However, as the impact of the Chinese New Year will be excluded in March and traditional peak season expectations remain, the operating rate is expected to recover to 71.25%, with a slight YoY increase of 0.11 percentage points.