After Surging, Philippine Nickel Ore Prices Pulled Back and Fluctuated Downward

During the week, FOB prices of medium- to high-grade nickel ore from the Philippines pulled back after surging. In the low-nickel and high-iron market, with the rainy season in the Philippines nearing its end, mines gradually offered quotes for March shipments. Currently, FOB transaction prices have softened compared to pre-rainy season levels. For medium- to high-grade nickel ore, although Indonesian ore price increases have supported the sentiment to stand firm on quotes among Philippine mines, domestic nickel pig iron (NPI) plants have limited acceptance of high-priced nickel ore. During the week, tender prices for medium-grade nickel ore from the Philippines were slightly lowered. In terms of supply: the rainy season in major southern mining areas is gradually ending, and subsequent shipments from the Philippines are expected to increase. On the demand side: the continuous rise in downstream NPI prices has brought some profit recovery, but NPI plants are still experiencing losses, limiting their acceptance of high-priced nickel ore from previous weeks. Currently, restocking is mainly just-in-time. Regarding port inventory, nickel ore inventories at ports continued to decline. As for ocean freight rates, with the end of the rainy season in major southern mining areas and the shift in shipment origins, ocean freight rates may rise. Overall, influenced by multiple factors, Philippine nickel ore prices are expected to pull back after surging in previous weeks and fluctuate downward.

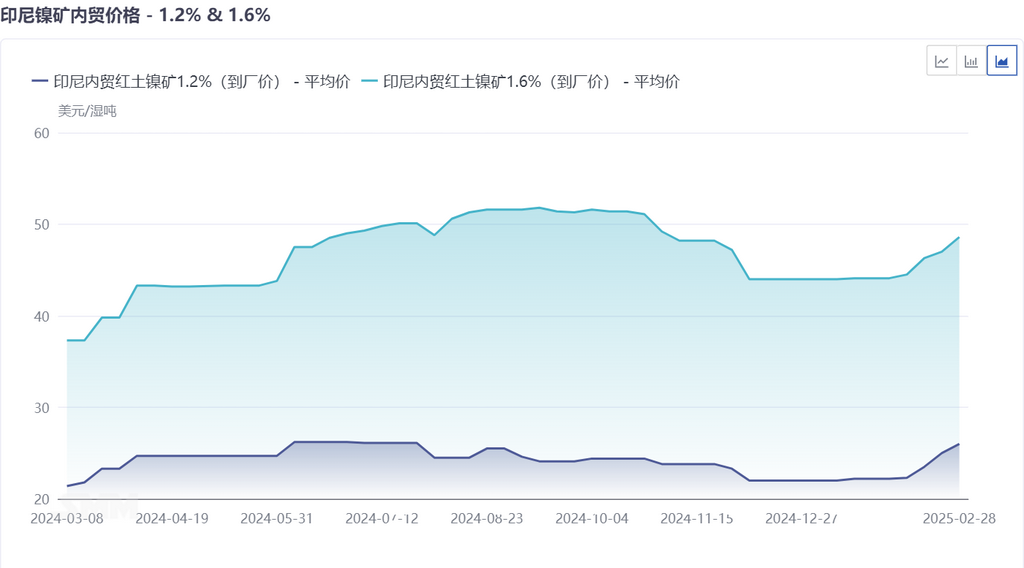

Indonesian Domestic Trade Nickel Ore Premiums Continue to Rise But at a Slower Pace

Currently, market transaction prices for pyrometallurgical ore have maintained the February18-19USD premium for Indonesian domestic trade ore. With March approaching, mainstream premiums for Indonesian nickel ore are expected to rise again. The procurement intention price for nickel ore in the industrial park on Sulawesi's Big K Island is tentatively set at19-20USD or above for March. However, most mid-sized pyrometallurgical smelters have not yet reached safe inventory levels for raw materials, showing some acceptance of premiums above20USD. For hydrometallurgical ore: due to limited quotas, mines tend to prioritize selling more profitable pyrometallurgical ore, actively reducing the volume of hydrometallurgical ore sold. Coupled with strong commissioning expectations for numerous hydrometallurgical projects this year and next, demand for hydrometallurgical ore is expected to grow rapidly throughout the year. In the medium and long-term, the price increase rate for hydrometallurgical ore may surpass that of pyrometallurgical ore. In terms of supply: shipment volumes from mines showed little change this week. Mines approved through the SIMBARA system exhibited relatively strong willingness to sell before Eid al-Fitr. Starting in March, as the rainy season in Sulawesi gradually ends and ports reopen, subsequent shipment volumes are expected to increase. On the demand side: mid-sized smelters are expected to make just-in-time procurement in March. Combined with profit recovery driven by the continuous rise in downstream NPI prices, demand support remains.

Additionally, onFebruary17, Indonesian President Prabowo issued Presidential Regulation No.8of2025, announcing a foreign exchange control policy for natural resource exports (DHE SDA). Although this policy does not directly affect nickel product exports, it has caused some disturbance to market sentiment. Overall, the MarchHPMbenchmark price is expected to remain stable. Combined with the expectation of increased upstream shipment volumes and sustained demand, the absolute price of Indonesian nickel ore is expected to rise, albeit at a slower pace. Moving forward, attention should be paid to the specific impact of the end of the rainy season in Sulawesi on the market's available nickel ore volumes.