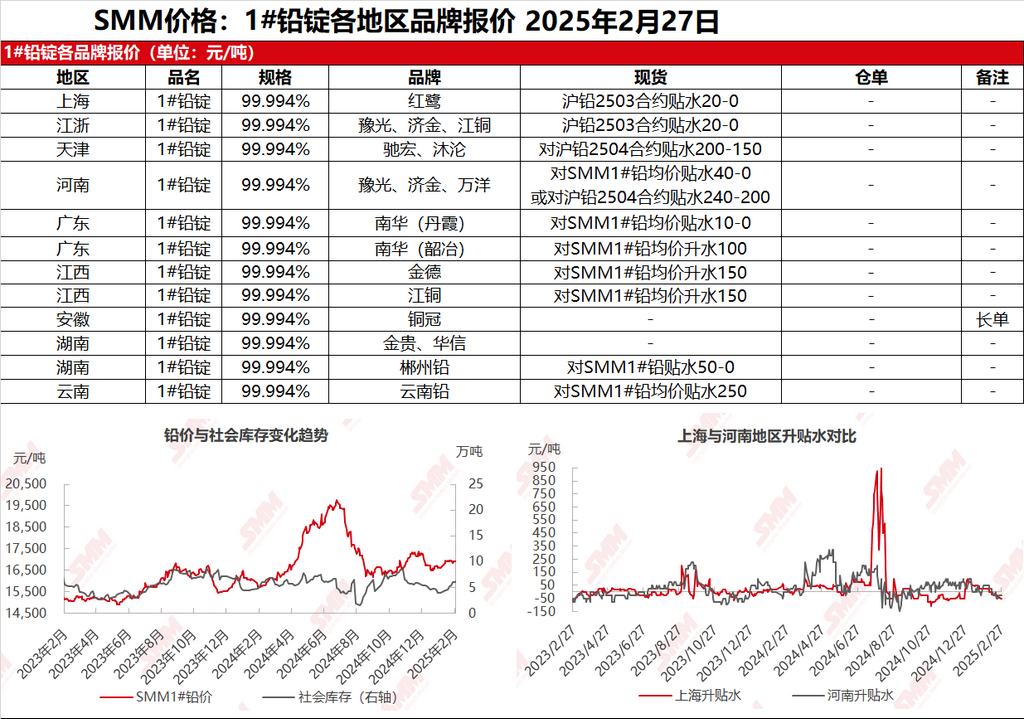

SMM, February 27: In the Shanghai market, Honglu lead was quoted at 17,090-17,110 yuan/mt, with discounts of 20-0 yuan/mt against the SHFE 2503 contract. In Jiangsu and Zhejiang regions, Yuguang, Jijin, and JCC lead were quoted at 17,090-17,110 yuan/mt, with discounts of 20-0 yuan/mt against the SHFE 2503 contract. SHFE lead fluctuated at high levels, and suppliers actively quoted for sales, mostly offering at discounts. Meanwhile, mainstream primary lead smelters provided ex-factory cargoes self-picked up from production sites at discounts of 50-0 yuan/mt against the SMM 1# lead average price, and secondary refined lead was quoted at discounts of 100-0 yuan/mt against the SMM 1# lead average price ex-factory. Some discounts widened compared to yesterday. Downstream enterprises showed moderate enthusiasm after the holiday, with some making inquiries as per usual practice, but actual purchases were limited, and spot order transactions were relatively weak.

In other markets: The SMM 1# lead price remained flat compared to the previous trading day. In Henan, smelters concluded transactions at slight discounts against the SMM 1# lead average price. In Hunan, smelters mainly shipped under long-term contracts, quoting on par with or at slight discounts. In Yunnan, transactions were concluded at discounts of 250 yuan/mt for just-in-need purchases. Lead prices continued to fluctuate rangebound, and downstream demand gradually recovered after inventory digestion, with slightly improved purchasing enthusiasm. However, transactions at premiums remained challenging, and the overall spot market remained sluggish.