Overview: Shanghai galvanized sheet prices remained stable in January-February, influenced by the off-season in consumption. After entering January, the overall market trading sentiment was not active. However, as the overall inventory pressure was relatively small and steel mill settlement prices were high, market traders showed a strong sentiment to stand firm on quotes, keeping prices stable. With the end of the holiday, downstream manufacturing and construction industries gradually resumed production. How will Shanghai galvanized coil prices trend in February-March?

I. Galvanized Price Review

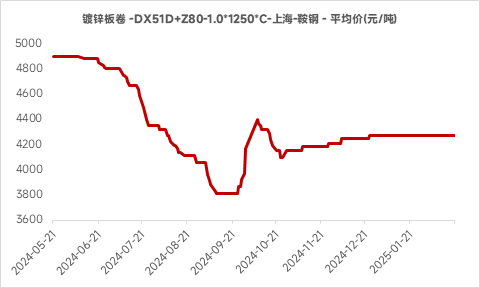

As shown in the chart above, Shanghai galvanized coil prices experienced a slight fluctuation and increase from mid-to-late October 2024 to the high point at the end of December, after which they stabilized. The main reasons were as follows: In September-October 2024, after macro policies fell short of expectations, Shanghai galvanized prices pulled back after a surge. However, in mid-to-late October 2024, the overall supply of galvanized coils was lower than in previous years. With the arrival of the consumption peak season in October, galvanized products continued destocking. After consolidating at the bottom, prices rebounded slightly. Entering January, due to the Chinese New Year holiday, the overall market trading sentiment gradually cooled. However, as the off-season consumption in manufacturing showed resilience, steel mills received relatively good galvanized orders, resulting in relatively small overall pressure. With strong bullish sentiment and high settlement prices, galvanized costs were well-supported. Therefore, during the off-season, prices remained stable.

II. In Terms of Supply

As shown in the chart above, throughout 2024, the operating rate of short-process galvanized steel mills was significantly lower YoY. The main reason was that the growth in galvanized consumption in 2024 was concentrated in manufacturing, with good export performance in home appliances and automobiles. Most of these products used galvanized products from state-owned mills. In contrast, short-process steel mill products were mostly used in the construction industry, where steel usage saw a significant YoY decline in 2024. Although galvanized steel mills gradually resumed production after the Chinese New Year holiday, the overall operating rate remained relatively low. Overall, the supply-side pressure for galvanized products was not significant.

III. In Terms of Demand

Galvanized sheets are mainly used in five sectors: substrates for color coating, real estate, steel structures, automobiles, and home appliances.

Home Appliance Industry: In terms of demand, according to the latest report on the three major white goods released by ChinaIOL, the total production schedule for air conditioners, refrigerators, and washing machines in February 2025 was 29.14 million units, up 30.6% YoY. By product, household air conditioner production was 15.93 million units, up 35.6% YoY; refrigerator production was 6.32 million units, up 29.2% YoY; washing machine production was 6.89 million units, down 21.3% YoY.

Automotive Industry: In January 2025, the operating rate of the automotive industry was 86.6%, up 6.9% YoY. However, the industry's prosperity weakened this month. Affected by the Chinese New Year, enterprises gradually went on holiday at the month-end, and the production pace of automakers nationwide slowed. However, some enterprises reported continuing production during the holiday to rush to meet deadlines due to excessive backlog orders. SMM estimates the operating rate of the automotive industry to be approximately 83.6% in February and 86.3% in March.

Construction and Infrastructure Industries: In January 2025, the operating rate of the construction industry was 45.9%, down 11.7% YoY. This month, affected by weather and the Chinese New Year, workers returned to their hometowns for the holiday, and many construction projects across the country were suspended. Only a few indoor construction projects remained operational, and the national construction pace continued to slow, with the operating rate further declining. SMM estimates the operating rate of the construction industry to be approximately 40.1% in February and 71.3% in March. In January 2025, the operating rate of the infrastructure industry was 56.6%, up 3.3% YoY. Despite the seasonal impact this month, especially the off-season in construction demand before the Chinese New Year, which led to a MoM decline in the operating rate of infrastructure projects across the country, the overall market showed YoY recovery. The construction pace of infrastructure projects in various regions remained stable. SMM estimates the operating rate of the infrastructure industry to be approximately 48.3% in February and 77.0% in March.

In summary, the consumption of downstream industries for galvanized products is expected to continue recovering in March. However, the construction industry remains in a YoY declining trend, while manufacturing and infrastructure consumption are expected to remain stable.

IV. Conclusion

For Shanghai galvanized coil prices in February-March, the current galvanized coil market is in a state of weak supply and demand, with no significant supply-demand imbalance. Meanwhile, the slow recovery of downstream consumption for galvanized coils in March, coupled with the inactive market trading sentiment and the decline in construction industry consumption, limits the upward momentum for galvanized prices. Overall, Shanghai galvanized coil prices are expected to continue fluctuating at high levels in February-March, under the pattern of tight supply-demand balance and strong cost support.