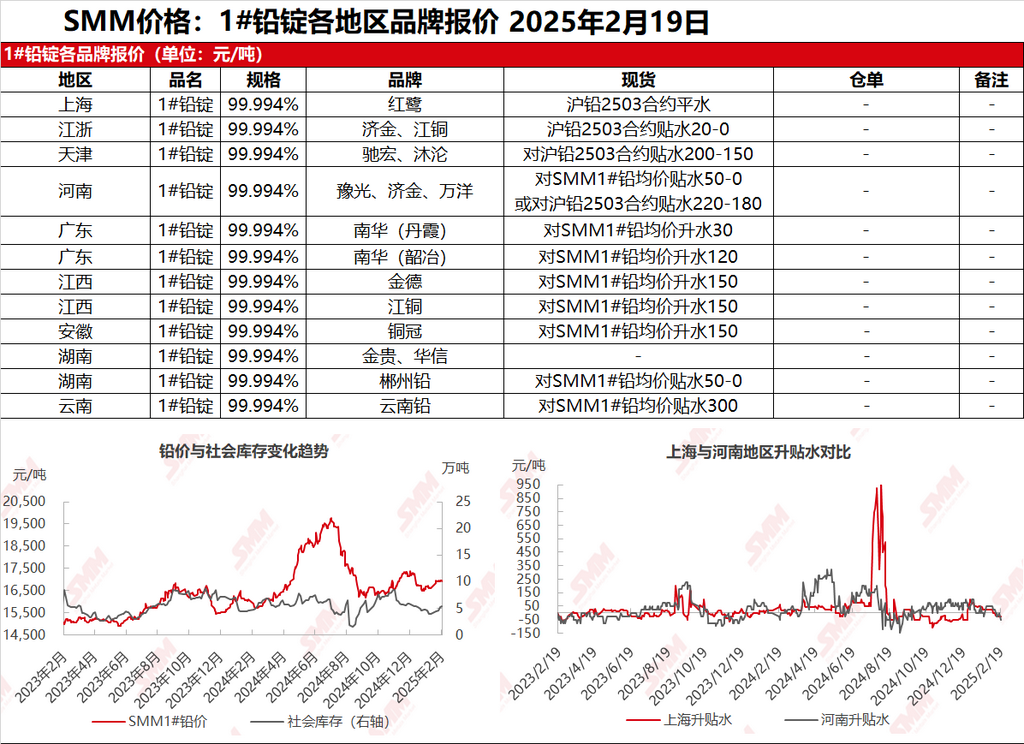

SMM News on February 19: In the Shanghai market, Honglu lead was quoted at 16,975-17,025 yuan/mt, on par with the SHFE 2503 contract; in Jiangsu and Zhejiang regions, JCC and Jijin lead were quoted at 16,955-17,025 yuan/mt, at discounts of 20-0 yuan/mt against the SHFE 2503 contract. SHFE lead remained range-bound in the morning session but plunged sharply at the end of the first trading session, breaking below the 17,000 yuan/mt threshold. Market participants, both upstream and downstream, adopted a more cautious stance. Suppliers kept their premiums and discounts unchanged, and smelters' ex-factory cargo quotations showed little change, with a few even lowering prices further. Meanwhile, secondary lead producers, constrained by costs, became more reluctant to sell at low prices. Secondary refined lead was quoted at discounts of 50-0 yuan/mt against the SMM 1# lead average price, ex-factory. Downstream, battery manufacturers remained cautious, with some probing inquiries but mostly increasing risk-aversion sentiment, leading to only a few transactions for rigid demand.

Other markets: Today, the SMM 1# lead price dropped slightly by 75 yuan/mt compared to the previous trading day. In Henan, smelters quoted discounts of 30-0 yuan/mt against the SMM 1# lead price, while some suppliers quoted discounts of 200 yuan/mt against the SHFE 2503 contract. In Hunan, smelter supply gradually recovered but was mainly shipped under long-term contracts, with suppliers maintaining discounts of 50-0 yuan/mt for transactions. In Yunnan, discounts of 300 yuan/mt were maintained, but downstream purchases were still dominated by long-term contracts, with almost no spot orders. After SHFE lead weakened in the second trading session, downstream buyers generally avoided risks and were cautious in procurement. Some social warehouses saw a slight inventory increase, and the spot market witnessed muted transactions.