》View SMM Lead Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Database

SMM, February 14:

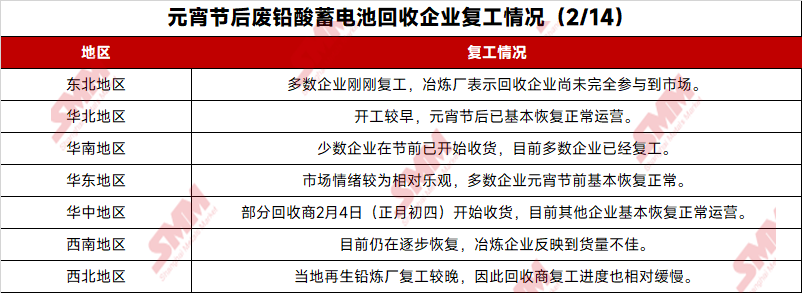

After the Lantern Festival holiday, the resumption progress of battery scrap recyclers varied by region, but the overall recovery trend showed steady growth. Based on the descriptions of secondary lead smelters and waste lead-acid battery recycling companies regarding the resumption progress of battery scrap recyclers in their provinces and nearby areas, as well as the raw material arrivals at smelters, SMM has compiled this article.

In Henan, smelters saw a significant depletion of battery scrap inventory during the Chinese New Year holiday, leading to a widespread shortage of raw material inventory after the holiday. Many smelters experienced substantial production cuts. However, with recyclers gradually resuming operations and raising raw material purchase prices, battery scrap inventory has been replenished, resulting in a slight increase in regional production this week.

Secondary lead smelters in Inner Mongolia and Liaoning reported that due to the still-cold weather, recyclers showed low enthusiasm for resuming work. Additionally, as it is currently the off-season for scrap, the volume of available purchases remains relatively limited.

Secondary lead smelters in Guangdong and Guangxi revealed that battery scrap arrivals were underwhelming, with expectations of further price increases.

It is reported that large secondary lead smelters in Anhui and Jiangsu receive daily arrivals of around 20 truckloads (approximately 600 mt). Under normal production conditions, these enterprises require at least 1,000 mt of battery scrap per day. Medium-to-large secondary lead smelters in Jiangxi stated that raw material arrivals were limited, with current inventory sufficient for only about three days. Both suppliers and recyclers exhibited bullish sentiment and reluctance to sell.

In summary, while battery scrap recyclers have largely resumed production, the main reason for the poor arrivals at secondary lead smelters lies in the off-season for scrap, with limited market supply and suppliers holding back sales in anticipation of higher prices.