Introduction

With the successful conclusion of 2024, the electrolyzer industry has reached a new turning point. After completing their annual shipment targets, major electrolyzer producers are eagerly embarking on a new journey in 2025. This article provides an in-depth analysis of the domestic electrolyzer industry's development over the past year from multiple dimensions and forecasts the development trends for the coming year.

I. Alkaline Electrolyzers: Market Fluctuations and Competitive Landscape

1. Brief Review of the Alkaline Electrolyzer Market in Q4 2024

In Q4 2024, the domestic market for alkaline electrolyzers achieved a total delivery volume of 1,044.51MW and delivered over 400 units. Compared to the approximately 950MW delivered in Q3, this represents an increase of about 10%. However, the number of units delivered decreased by approximately 20% from over 500 units in Q3. The root cause of this phenomenon lies in the non-standardized specifications of alkaline electrolyzers and the diverse needs of customers.

The main delivery channels for alkaline electrolyzers include green hydrogen projects in Inner Mongolia and Xinjiang, as well as traditional chemical, PV, and gas sectors with scattered usage. The core reason for the increase in delivery volume but decrease in unit numbers in Q4 was the concentrated delivery of green hydrogen projects at year-end and the reduced demand from traditional scattered users. Currently, green hydrogen projects generally adopt alkaline electrolyzers with a standard capacity of 1,000Nm³/h, with a few projects using 2,000Nm³/h units. The increase in single-unit capacity led to a decline in unit numbers while boosting overall delivery volume.

In terms of the competitive landscape, the increase in large-capacity deliveries has allowed top-tier enterprises to dominate the market, posing significant challenges for small and medium-sized electrolyzer enterprises.

2. Annual Review of Alkaline Electrolyzers in 2024

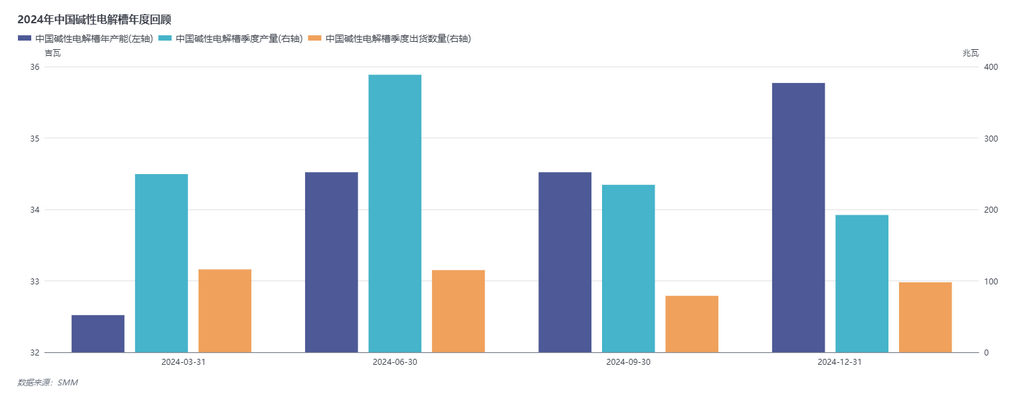

Looking back at 2024, the delivery performance of alkaline electrolyzers was closely tied to the construction of green hydrogen projects. The increase in green hydrogen projects drove capacity expansion and shipment growth among electrolyzer producers. From a capacity perspective, the capacity of alkaline electrolyzers grew from 32.52GW at the beginning of the year to 35.77GW in Q4, with a total annual increase of 3.25GW, primarily concentrated among top-tier enterprises. Although the growth rate slowed, this reflects a more rational investment approach in the hydrogen energy sector amid a challenging macroeconomic environment, with enterprises adopting a cautious attitude toward the long-term development of hydrogen energy.

In terms of delivery volume, the slowdown in green hydrogen project construction and the reduced expansion pace of traditional scattered users due to macroeconomic constraints led to underwhelming delivery performance in 2024. The highest quarterly delivery volume was recorded in Q2, reaching 388.5MW, which was nearly 100% higher than the approximately 200MW delivered in Q3 and Q4. This was mainly due to the time lag between green hydrogen project orders and actual deliveries, as well as the partial release of demand in the traditional scattered market during Q2.

Chart-1: Quarterly Statistics of China's Alkaline Electrolyzer Capacity, Production, and Shipments in 2024

3. Discrepancy Between Alkaline Electrolyzer Capacity and Production

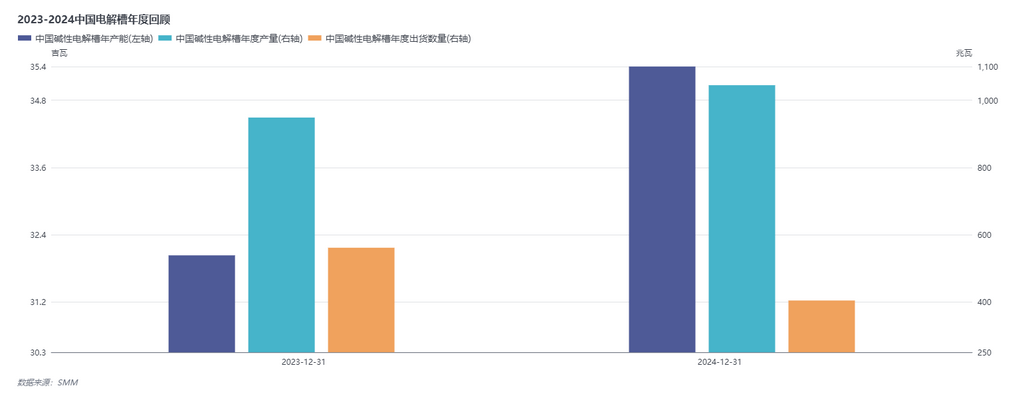

In 2023, the capacity of alkaline electrolyzers was 32.025GW with a delivery volume of 948.25MW. By 2024, capacity had increased to 35.77GW, while delivery volume only reached 1,044.51MW. The significant gap between capacity and production is reasonable within the context of domestic electrolyzer development.

On one hand, the hydrogen production and consumption chains in China are not fully integrated, resulting in limited shipments of electrolyzers, which are primarily supplied to green hydrogen projects through bidding processes. On the other hand, there is still room for improvement in the technical models, power consumption, and hydrogen production efficiency of current alkaline electrolyzers. As a result, manufacturers are building electrolyzer production lines to reserve technical resources in anticipation of gaining a first-mover advantage in the hydrogen energy sector. Furthermore, with the basic integration of green hydrogen application technologies and the planning and filing stages of Chinese green hydrogen projects, the large-scale rollout of green hydrogen projects is imminent, providing a core rationale for electrolyzer enterprises to expand capacity.

Chart-2: Annual Statistics of China's Electrolyzer Capacity, Production, and Shipments, 2023-2024

4. China's Electrolyzer Shipments and Trends, 2020-2024

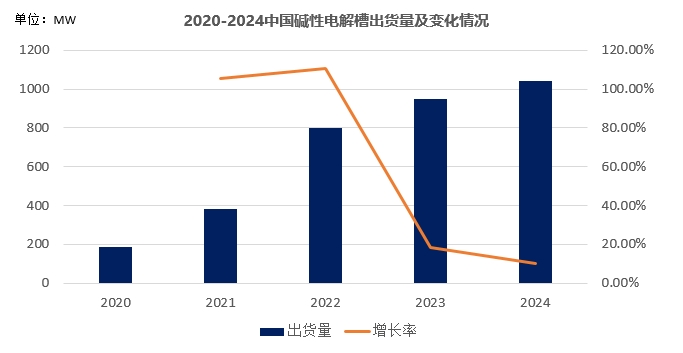

Over the past five years, China's alkaline electrolyzer delivery volume has achieved continuous growth, rising from 185MW in 2020 to 1,044.51MW in 2024, representing nearly a tenfold increase. However, since 2022, the growth rate of alkaline electrolyzers has significantly slowed, dropping from 105.41% in 2021 to 10.15%. This reflects both the continuous development of China's hydrogen energy sector and the inevitable challenges in transitioning from theoretical frameworks to practical applications.

The emergence of green hydrogen projects has opened new opportunities for China's alkaline electrolyzer market but has also intensified market competition. Statistics show that while there are at least 200 enterprises in China with alkaline electrolyzer production technology, fewer than 50 had shipments in 2023-2024, and fewer than 15 delivered in Q4 2024. The top 10 enterprises accounted for 85% of the alkaline electrolyzer market, with established state-owned electrolyzer enterprises securing a foothold in green hydrogen project bids. Small and medium-sized enterprises face significant challenges in breaking this market structure in the short term.

Additionally, demand for alkaline electrolyzers in traditional chemical sectors such as ammonia synthesis and polysilicon production has been affected. The prolonged economic downturn following pandemic restrictions has led to a decline in traditional chemical industries, while low-price competition caused by PV overcapacity and stagnation in capacity expansion among polysilicon producers have contributed to the continued decline in electrolyzer growth rates.

Based on these trends, it is predicted that 2025 will see annual alkaline electrolyzer deliveries of 1,100-1,300MW, with a growth rate of approximately 10%-15%. This forecast is based on the support from H2 2024 green hydrogen projects for 2025 shipments, delivery demand from new projects starting in H1 2025, and small-capacity deliveries driven by electrolyzer replacements in some chemical enterprises. However, if green hydrogen project deliveries face challenges, a YoY decline of 10%-15% is also possible. Overall, 2025 is expected to remain a year of intensified competition and stringent cost-reduction requirements for alkaline electrolyzer enterprises.

Chart-3: Statistics of China's Alkaline Electrolyzer Shipments and Trends, 2020-2024

5. PEM Electrolyzers: Niche but Promising

PEM electrolyzers have remained a relatively niche segment in China. Their high equipment costs and generally low hydrogen production per unit have limited their use in domestic green hydrogen projects. However, PEM electrolyzers find extensive applications in high-tech fields such as medical and semiconductor industries. These sectors demand high hydrogen quality and can afford premium costs, making PEM electrolyzers a preferred choice for hydrogen production.

In 2024, domestic PEM electrolyzer capacity remained steady at around 600MW, with deliveries primarily dominated by established PEM enterprises. PEM electrolyzers accounted for approximately 5%-8% of the total electrolyzer market. Some well-funded green hydrogen projects have adopted a combination of one PEM unit and multiple alkaline electrolyzers, using PEM to drive the operation of alkaline electrolyzers.

Looking ahead, to meet the demands of large-scale hydrogen production, PEM electrolyzers are expected to gradually reduce costs and further improve their hydrogen production efficiency per unit. It is anticipated that 2025 PEM electrolyzer capacity and deliveries will maintain 2024 levels, with a growth rate of 5%-10%. Although PEM electrolyzers remain niche in the domestic market, their potential and development prospects should not be overlooked.

Chart-4: Statistics of PEM Electrolyzer Orders in 2024

6. SOEC and AEM Electrolyzers: Exploring Emerging Technology Pathways

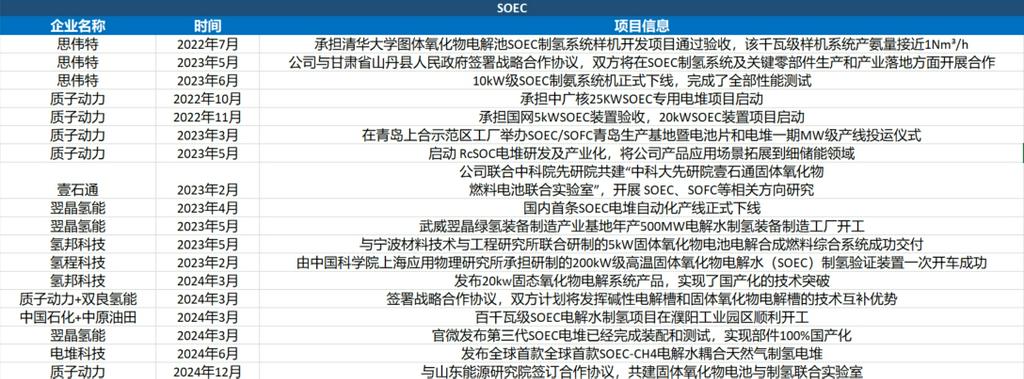

In addition to alkaline and PEM electrolyzers, SOEC and AEM represent two noteworthy technological pathways in the hydrogen production field.

SOEC development has been relatively slow due to application limitations. In 2024, only four enterprises made progress in SOEC. For instance, Stack Technology launched the world's first SOEC electrolyzer coupled with natural gas hydrogen production in June 2024, while Yujing Technology released its third-generation SOEC stack in March. However, the practical application of these stacks is still under testing in real-world scenarios. The development of SOEC technology pathways and application scenarios remains a long-term endeavor.

AEM electrolyzers, on the other hand, have garnered attention for their cost advantages due to the absence of precious metals. In 2024, some electrolyzer enterprises ventured into the AEM field and achieved notable results, with certain AEM products even being shipped to overseas markets. However, given the relatively short development timeline of AEM, the technology has yet to reach the stage of improving hydrogen production efficiency. As a result, AEM is not yet widely applicable in green hydrogen projects that prioritize efficiency. It is expected that at least 3-5 more years of practice will be needed to draw definitive conclusions.

Chart-5: Tracking SOEC and AEM Electrolyzer Technologies

Conclusion

Reflecting on the development of the hydrogen energy industry, particularly in hydrogen production, in 2024, the results are mixed. On one hand, we witnessed the excitement of enterprises launching new products and developing new technologies; on the other hand, we felt the intensifying cut-throat competition and skepticism about whether hydrogen energy is merely a fantasy. However, regardless of external judgments, we cannot deny the importance of hydrogen energy as a clean energy source and its future development potential.

In the new year, let us work together to continue exploring the limitless possibilities of the hydrogen energy industry. If you are interested in the hydrogen energy sector or have any questions or needs, feel free to contact me. As an SMM hydrogen energy analyst, I am willing to communicate and collaborate with everyone interested in hydrogen to promote the development and progress of the hydrogen energy industry.

Written by: SMM Hydrogen Energy Analyst Sofia Xin Shi - 13515219405 (WeChat available). If you are also interested in hydrogen, feel free to contact me for discussions and exchanges.