Weekly Review

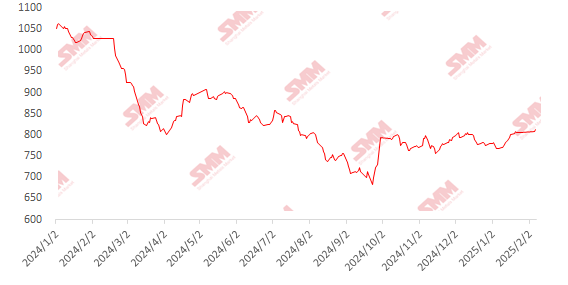

This week, imported iron ore prices showed a fluctuating trend. Macro side, several countries announced increased tariffs on steel, escalating the global trade war and intensifying market concerns over potential obstacles to future steel exports, leading to a pessimistic sentiment. Fundamentals side, cyclones and heavy rains in Australia continued to impact shipments from main ports, significantly reducing iron ore supply and easing supply pressure. Although pig iron production decreased slightly this week, the total inventory of the five major steel products remained low, and steel mill profits were moderate, providing room for future pig iron production increases. The tug-of-war between longs and shorts was intense, with futures prices fluctuating. Post-holiday, steel mills actively restocked, supporting spot prices, and the spot-futures price spread narrowed. Port prices in Shandong saw PB fines rise by 5 yuan/mt WoW.

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

Domestic Iron Ore Prices Rose Slightly This Week; Prices Are Expected to Fluctuate Next WeekThis week, prices in Tangshan, Qian'an, and Qianxi in Hebei rose by 1-5 yuan/mt, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping increased by 5-10 yuan/mt. Prices in east China rose by 1-5 yuan/mt.

Tangshan RegionIron ore concentrates prices were influenced by price adjustments from local leading steel mills, with the delivery-to-factory price for 66-grade dry basis with tax at 970-980 yuan/mt. However, only a few suppliers made shipments, as most held back due to thin profits. The operating rate of local mines and beneficiation plants remained low, exacerbating the tight supply of iron ore concentrates. Additionally, local steel mills strongly suppressed raw material prices, making it difficult for procurement prices to meet suppliers' expectations, resulting in a sluggish overall market.

West Liaoning RegionThe iron ore concentrates market was relatively quiet, with prices remaining relatively stable. The 66-grade wet basis price excluding tax was 700-710 yuan/mt. Mines and beneficiation plants were affected by the spring holiday and low temperatures, with some mines expected to resume operations after the Lantern Festival, and concentrate production workshops likely to gradually resume after early March. Overall, the supply of iron ore concentrates in the region remained tight. Steel mills showed weak purchase willingness, mainly purchasing as needed. Coupled with current transportation difficulties and a shortage of circulating trucks, the overall market transactions were sluggish.

East China RegionCurrently, production is proceeding as planned, with production and sales aligned, and no significant inventory pressure. Mines and beneficiation plants, except for certain areas in Shandong, have mostly resumed normal production. Some iron ore concentrates from the region are flowing to Hebei, but shipment volumes remain low and are expected to gradually normalize after mid-month.

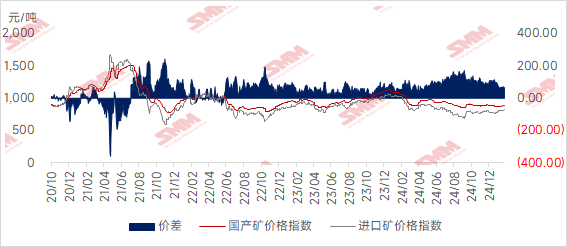

Considering both domestic and imported ore prices, prices for both rose slightly this week, with the price spread between domestic and imported ore remaining stable. The price spread may narrow next week.

Outlook for Next Week

Imported Ore:The impact of Australian cyclones is expected to end this weekend, leading to a significant recovery in iron ore shipments. However, due to previously low shipment levels, port arrivals are likely to remain low. Meanwhile, pig iron production is expected to increase slightly, coupled with domestic steel mills' restocking demand, driving overall iron ore demand growth. Port inventories may decline, providing support for ore prices. As the Two Sessions approach, market expectations for macro policies are strengthening, but the steel tariff issue may continue to affect sentiment. Amid the tug-of-war between longs and shorts, iron ore prices are expected to fluctuate considerably next week.

Domestic Ore:Overall,the cost-performance advantage of domestic ore has strengthened, and with weak supply, low-priced resources are hard to find. Resistance to price declines is significant in many regions, and local iron ore concentrate prices are expected to fluctuate at high levels next week.

Click to View the SMM Metal Industry Chain Database