SMM, February 14:

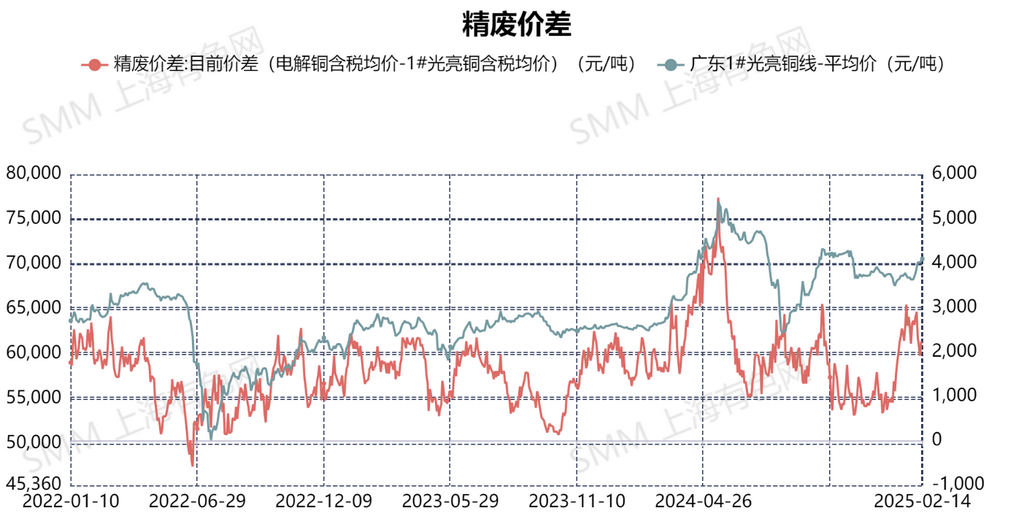

This week, copper prices showed a fluctuating upward trend, with an overall increase of 1,400 yuan/mt. The price range of bare bright copper in Guangdong was 70,300-70,500 yuan/mt, up by 800 yuan/mt. After the Lantern Festival, logistics operations at warehouses across regions have returned to normal. Early in the week, as copper prices pulled back, many suppliers of secondary copper raw materials, concerned about shrinking profits, actively sold off their inventory. Several secondary copper rod enterprises reported daily purchase volumes of 1,000-1,500 mt. However, approaching the weekend, as copper prices rebounded, suppliers of secondary copper raw materials began to control their selling prices and were reluctant to negotiate prices with secondary copper rod enterprises. Despite good post-holiday procurement and sufficient raw material inventory to sustain production, secondary copper rod enterprises were not in a hurry to purchase raw materials at market prices due to high copper prices and weak end-use consumption, which limited new orders. This week, the raw material inventory of sample enterprises for secondary copper was 4,300 mt, an increase of 200 mt from last week's 4,100 mt.

In terms of imported secondary copper raw materials, the US-China trade war has hindered import traders from resuming procurement from the US. In Europe, local restrictions on renewable resource exports have impacted procurement volumes and costs to varying degrees. This week, the overall supply of imported secondary copper raw materials remained at a relatively low level.

This week, the CIF quotation for #1 copper scrap was COMEX 3M copper contract minus 55-60¢/lb, and for #2 copper scrap, it was COMEX 3M copper contract minus 65-70¢/lb. The CIF quotation for US brass scrap had an LME coefficient of 67-67.5%, with a fixed price of $6,050-6,100/mt (limited transactions). The CIF quotation for non-US Cu98.5% wire nodules had an LME coefficient of 96.25-96.5%, while the CIF quotation for non-US bare bright copper had an LME coefficient of 98.5-99% LME.

Looking ahead to next week, even if copper prices pull back, given the current tight supply of secondary copper raw materials, suppliers are expected to stand firm on quotes.