SMM February 13, 2025:

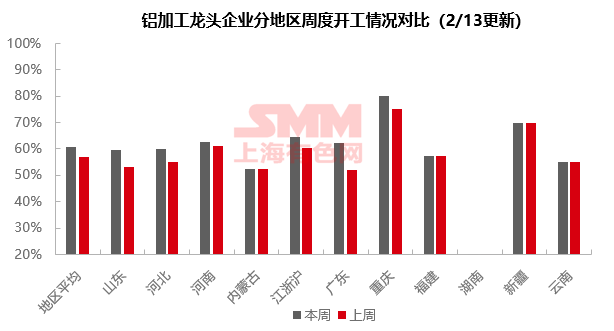

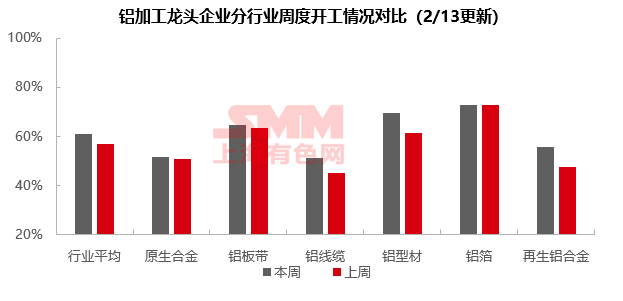

This week, the operating rate of leading downstream aluminum processing enterprises in China maintained a recovery trend, up 4.1 percentage points WoW to 60.8%, driven by post-holiday resumption. By segment, the operating rate of primary aluminum alloy increased slightly by 1% WoW to 51.6%, supported by the early resumption of some customers, with a faster recovery expected after the Lantern Festival. The operating rate of aluminum plate/sheet and strip saw only a slight rebound due to weak restocking willingness from end-users and the off-season impact. The aluminum foil segment remained stable, with air-conditioner foil benefiting from seasonal demand and home appliance subsidy policies, while packaging foil and battery foil faced pressure from overcapacity. Other segments showed significant recovery: the operating rate of aluminum wire and cable rose 6% to 51%, with 230,000 mt of UHV tender orders set to be released, though weak delivery pressure limited the rebound. The operating rate of aluminum extrusion increased to 69.5%, with PV extrusion supported by new policies and improved production schedules, while construction extrusion faced weak orders due to payment cycle pressures. The operating rate of secondary aluminum alloy rebounded sharply by 8.1% to 55.6%, driven by restocking demand from downstream enterprises, though high prices constrained procurement. Overall, post-Lantern Festival, the resumption of aluminum processing enterprises is expected to accelerate, coupled with the approach of the traditional peak season in March. Operating rates across segments still have upside room, but attention should be paid to the recovery of end-use consumption and changes in the export market. According to SMM forecasts, the operating rate of leading downstream aluminum processing enterprises in China is expected to rise by another 1.6 percentage points next week to 62.4%.

Primary Aluminum Alloy: This week, the operating rate of leading primary aluminum alloy enterprises in China recorded 51.6%, up 1% WoW. The operating rates of primary aluminum alloy enterprises this week showed a stable to slightly increasing trend. Some downstream customers in certain regions resumed operations as early as the eighth day of the Chinese New Year, leading to a relatively steady increase in operating performance. However, February remains an off-season for the primary aluminum alloy segment, with some producers adopting a wait-and-see approach and maintaining a slow production pace without significant changes. After the Lantern Festival, as downstream operating rates continue to recover, demand is expected to sustain its recovery, and the operating rate of primary aluminum alloy next week may return to levels near the pre-holiday norm.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises increased slightly by 1.2 percentage points to 64.6%. Although the aluminum plate/sheet and strip market gradually resumed transactions this week, inquiries and orders remained below expectations. On the one hand, the off-season led to weak demand; on the other hand, downstream end-users had sufficient stockpiles before the holiday, resulting in low restocking willingness. Therefore, the operating rate of aluminum plate/sheet and strip only showed a slight rebound this week. Notably, in 2024, China's aluminum plate/sheet and strip exports to the US totaled 161,400 mt, accounting for only 4.7% of China's total aluminum plate/sheet and strip exports. From the perspective of export share, the US tariff hike had a limited impact on the domestic aluminum plate/sheet and strip market. Next week, with the Lantern Festival marking the end of the Chinese New Year holiday and the approach of the traditional peak season in March, the operating rate is expected to rise gradually.

Aluminum Wire and Cable: This week, the operating rate of leading aluminum wire and cable enterprises in China recorded 51%, up 6% WoW. Leading enterprises in the aluminum wire and cable sector have resumed operations after the holiday, while medium and small enterprises are still in the process of resuming. However, due to the low urgency of post-holiday delivery orders this year, operating conditions have not fully recovered. Recently, the first batch of power transmission and transformation and UHV tenders have been underway, with a total of 230,000 mt of conductor orders set to be opened on February 17. SMM believes that in the short term, the aluminum wire and cable industry remains in a recovery phase, with operating performance fluctuating downward. However, as power transmission and UHV orders are finalized, they are expected to support subsequent operations.

Aluminum Extrusion: This week, the overall operating rate of the aluminum extrusion industry in China increased slightly to 69.5%. In the industrial extrusion segment, top-tier enterprises maintained high operating rates, but small and medium-sized processing enterprises in South China reported slow resumption progress, with homogeneous competition leading to vicious competition in processing fees. PV extrusion enterprises showed optimistic expectations, with SMM reporting that the new PV policies, coupled with the end of the off-season, drove seasonal increases in production schedules, and orders on hand are expected to improve. In the construction extrusion segment, leading enterprises resumed operations quickly due to their advantage in orders on hand, but small and medium-sized window and door manufacturers faced pressure from extended payment cycles, resulting in weak new orders. SMM will continue to monitor the progress of terminal real estate project completions, PV installation demand, and changes in automotive aluminum consumption per unit.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises remained unchanged at 72.7%. By product, air-conditioner foil, which is highly seasonal, showed optimistic order recovery due to the approaching peak season and the stimulus of national subsidy policies for the home appliance consumer market. However, products such as food packaging foil and battery foil faced intense competition due to overcapacity from new production in recent years. As the traditional peak season in March approaches, the order volume and operating rate of leading aluminum foil enterprises are expected to continue rising.

Secondary Aluminum Alloy: This week, the operating rate of leading secondary aluminum alloy enterprises rebounded by 8.1 percentage points WoW to 55.6%, driven by post-holiday resumption. By the second week after the holiday, the operating rate of large secondary aluminum enterprises had gradually returned to pre-holiday normal levels, and small and medium-sized enterprises also resumed production after the Lantern Festival. On the demand side, downstream die-casting enterprises saw a mild recovery in orders, with some enterprises showing restocking demand after consuming pre-holiday stockpiles. However, the market has not fully recovered, and high post-holiday prices have led to just-in-time procurement by downstream enterprises. In the short term, the operating rate of the secondary aluminum industry is expected to continue its upward trend, with attention on raw material supply and the pace of downstream demand recovery.

》Click to View the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)