Since April 2022, the SMM rebar production schedule sample has been expanded to 56 enterprises.

According to the SMM survey data of 56 key steel mills:

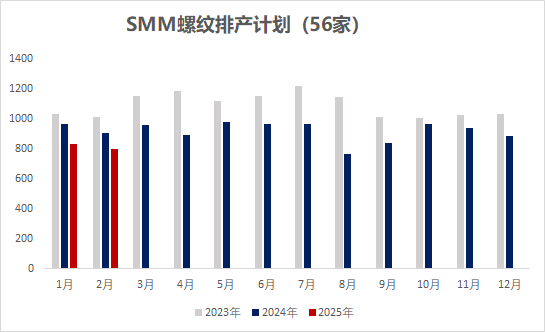

- In February, the planned rebar production was 8.0104 million mt, down 283,900 mt from the actual production in January, a decrease of 3.42%;

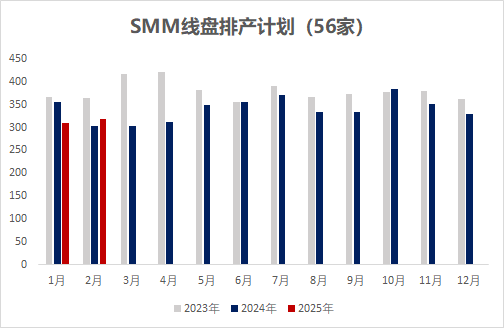

- In February, the planned wire rod production was 3.1817 million mt, up 83,200 mt from the actual production in January, an increase of 2.69%.

Chart-1: Production Schedule of Rebar & Coiled Rebar by Major Construction Steel Mills (56 Enterprises)

Source: SMM

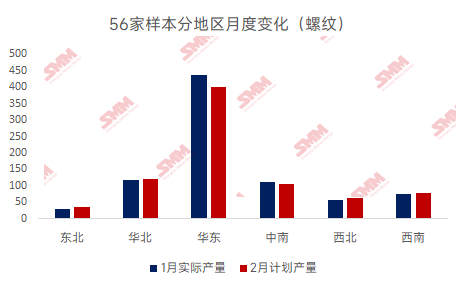

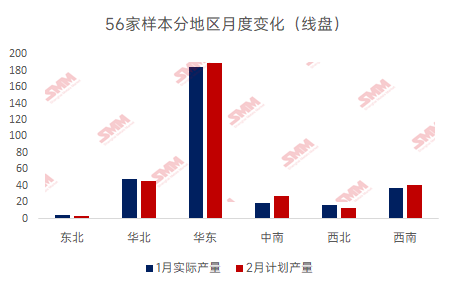

By region (56 enterprises):

North-East China: The total planned rebar production was 347,400 mt, up 40,100 mt WoW, an increase of 13.05%. The total planned wire rod production was 29,700 mt, down 10,300 mt WoW, a decrease of 25.75%;

North China: The total planned rebar production was 1.21 million mt, up 32,000 mt WoW, an increase of 2.72%. The total planned wire rod production was 452,000 mt, down 26,000 mt WoW, a decrease of 5.44%;

East China: The total planned rebar production was 3.997 million mt, down 367,000 mt WoW, a decrease of 8.41%. The total planned wire rod production was 1.89 million mt, up 44,500 mt WoW, an increase of 2.41%;

Central-South China: The total planned rebar production was 1.07 million mt, down 60,000 mt WoW, a decrease of 5.31%. The total planned wire rod production was 270,000 mt, up 77,000 mt WoW, an increase of 39.9%;

North-West China: The total planned rebar production was 620,000 mt, up 55,000 mt WoW, an increase of 9.73%. The total planned wire rod production was 135,000 mt, down 30,000 mt WoW, a decrease of 18.18%;

South-West China: The total planned rebar production was 766,000 mt, up 16,000 mt WoW, an increase of 2.13%. The total planned wire rod production was 405,000 mt, up 28,000 mt WoW, an increase of 2.69%.

Chart-2: Monthly Regional Changes in Rebar Production

Source: SMM

Chart-3: Monthly Regional Changes in Wire Rod Production

Source: SMM

Overall:

In the first half of January, national construction steel prices showed a "V" trend, mainly due to weaker-than-expected favourable macro front and low enthusiasm for winter stockpiling. In the second half of the month, as the Chinese New Year approached, the market gradually closed, demand stagnated, and spot prices stabilized. On the cost side, iron ore prices fluctuated within a narrow range, coke fundamentals remained weak, and steel mill profitability for construction steel was moderate except for some losses in north-west and east China, with profits ranging from (-300-300). In February, blast furnaces under maintenance in north China were gradually resuming production, while some areas in east China continued production control with additional maintenance. Other regions maintained relatively stable production. EAF steel mills resumed production gradually after the Chinese New Year holiday, starting from February 7. The planned February construction steel production showed a decrease in rebar and an increase in wire rod, with a slight increase in daily average production.

By region:

North-East China: Steel mill profits ranged from (-100-100). Some mills resumed production after maintenance, increasing rebar output, while others continued selling billets externally due to stagnant local demand. Planned February rebar production increased slightly.

North China: Steel mill profits ranged from (100-300). Construction steel profitability in the region was moderate, but some mills had not yet resumed production after the holiday. Downstream real estate demand was limited by funding constraints. Planned February production in the region showed an increase in rebar and a decrease in wire rod, with a slight overall increase.

East China: Steel mill profits ranged from (-100-200). Some areas continued production control with poor profitability, and additional maintenance was scheduled. Overall, planned February construction steel production in the region decreased MoM.

North-West China: Steel mill profits ranged from (-300-0). High production costs led to poor profitability. Blast furnaces and rolling lines in the region remained under maintenance, with plans to resume production in late February. Planned February construction steel production in the region increased slightly.

Central-South China: Steel mill profits ranged from (0-100). The region saw both new maintenance and production resumption in February. Maintenance mainly affected rebar, while resumed production focused on wire rod. Planned February construction steel production in the region showed a decrease in rebar and an increase in wire rod, with a slight overall increase.

South-West China: Steel mill profits ranged from (-50-100). New capacity in the region stabilized production, with planned February construction steel production increasing slightly compared to January.

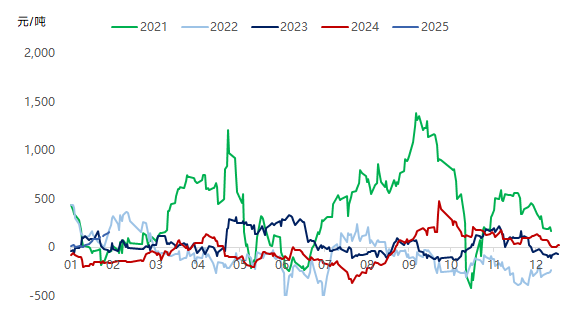

Chart-4: Real-Time Profit Trends of Rebar Production Since 2020

Source: SMM

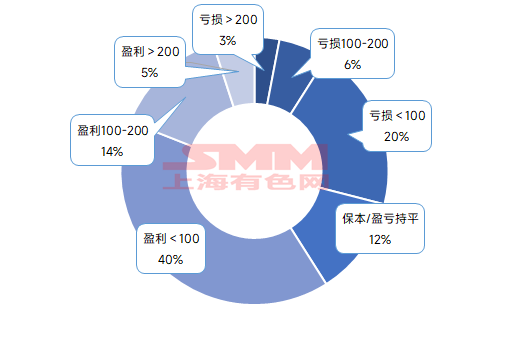

Chart-5: Marginal Profit of Rebar Production at Sample Steel Mills in Early February

Source: SMM

Looking ahead: In terms of work resumption, most market merchants across regions are expected to resume operations before the Lantern Festival. Downstream end-use demand, constrained by the availability of workers, is expected to recover gradually after the Lantern Festival. Additionally, project funding availability is expected to decline slightly YoY. EAF steel mills are expected to resume production gradually, with most resuming by mid-February. Due to cost constraints, operations may focus on off-peak electricity production. On the supply side, some blast furnaces at blast furnace steel mills are expected to resume production after maintenance, while new maintenance is also planned. Daily average construction steel production in February is expected to increase slightly compared to January. Regarding inventory, according to the SMM survey, national rebar inventory in the first week after the holiday was 6.6117 million mt, up 2.1327 million mt from pre-holiday levels, a WoW increase of 47.62%, but down 32.64% YoY on a lunar calendar basis, remaining at a low YoY level. On the demand side, downstream end-use demand is expected to recover gradually around the Lantern Festival. Current low production and low inventory levels provide some support for spot prices. Market confidence is bolstered by expectations for the Two Sessions and strong fundamentals in the iron ore market. However, the strength of downstream demand recovery remains to be seen. February construction steel prices are expected to show an inverted "V" trend, with limited upward and downward space.