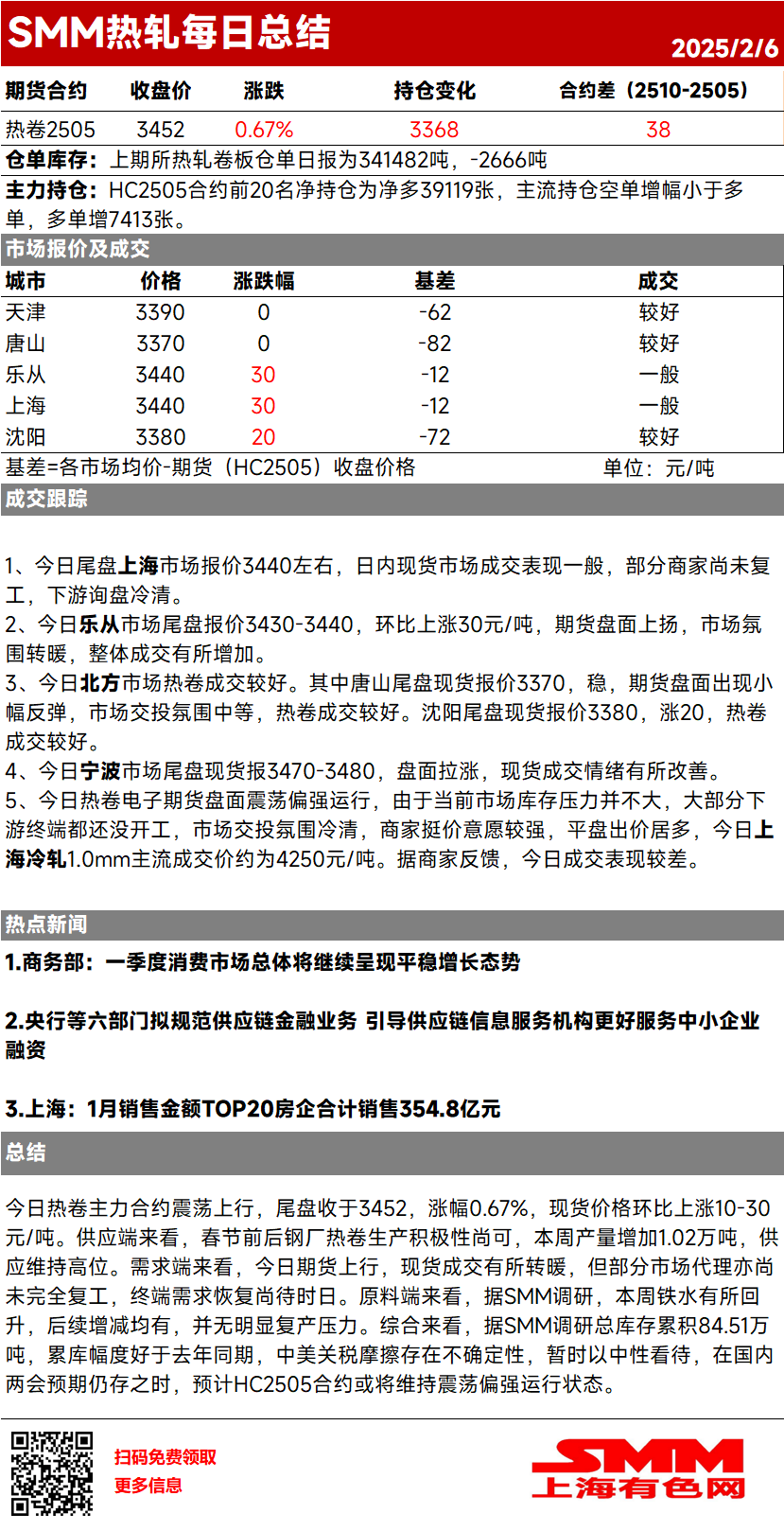

[SMM Hot-Rolled Daily Review] Futures Coil Bottomed Out, Spot Transactions Showed Some Recovery

The most-traded HRC futures contract fluctuated upward today, closing at 3,452 yuan/mt, up 0.67%. Spot prices rose by 10-30 yuan/mt MoM.

Supply side, steel mills showed moderate enthusiasm for HRC production before and after the Chinese New Year. This week, production increased by 10,200 mt, keeping supply at a high level.

Demand side, futures prices rose today, and spot transactions improved slightly. However, some market agents have not fully resumed operations, and the recovery of end-use demand will take time.

Raw material side, according to the SMM survey, pig iron production rebounded this week, with potential increases or decreases ahead, but no significant pressure for resumption of production was observed.

In summary, based on the SMM survey, total inventory accumulated to 845,100 mt this week, with the inventory buildup better than the same period last year. The uncertainty surrounding the US-China tariff disputes is being viewed neutrally for now. With expectations for the domestic Two Sessions still in place, the HC2505 contract is expected to maintain a fluctuating upward trend.

Today, the most-traded HRC futures contract fluctuated upward, closing at 3,452 with a gain of 0.67%. Spot prices rose by 10-30 yuan/mt MoM. Supply side, steel mills maintained moderate enthusiasm for HRC production before and after the Chinese New Year. This week, production increased by 10,200 mt, keeping supply at a high level. Demand side, futures prices rose today, and spot transactions showed some improvement. However, some market agents have not fully resumed operations, and the recovery of end-use demand still requires time. Raw material side, according to the SMM survey, pig iron production rebounded this week, with subsequent fluctuations expected, and no significant pressure from production resumption was observed. Overall, based on the SMM survey, total inventory accumulated to 845,100 mt this week, with the inventory buildup better than the same period last year. The uncertainty surrounding the US-China tariff disputes leads to a neutral outlook for now. With expectations for the domestic Two Sessions still present, the HC2505 contract is expected to maintain a fluctuating upward trend.