》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

Today is the eighth day of the Chinese New Year. While the festive atmosphere of the Spring Festival lingers, a new journey has already begun. SMM wishes all colleagues in the aluminum industry a prosperous start, thriving business, great fortune in the Year of the Snake, abundant wealth, and soaring careers!

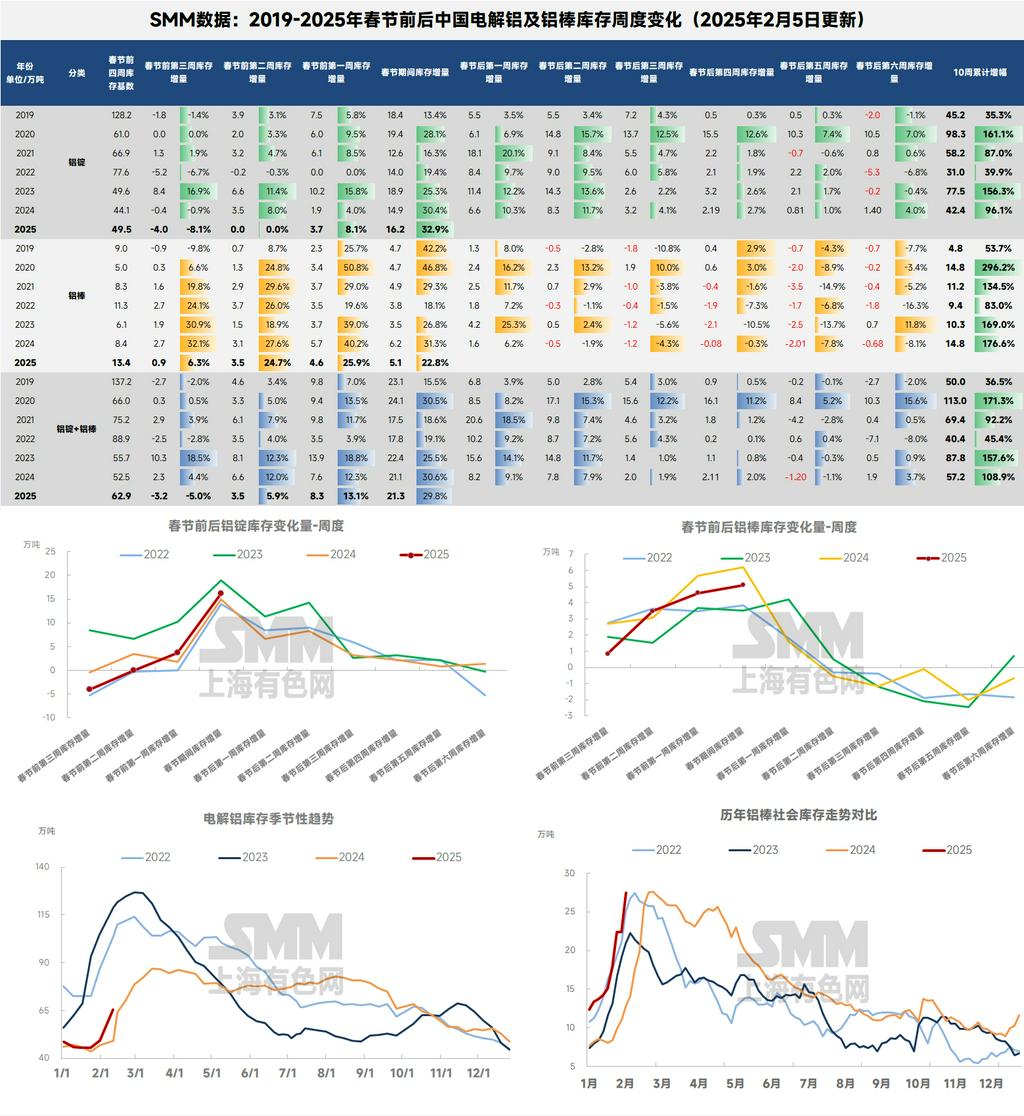

After the eight-day national statutory Chinese New Year holiday, let us focus on the aluminum inventory performance freshly released on the first day after the holiday:According to SMM statistics, as of February 5, 2025, the total domestic aluminum inventory (aluminum ingot + aluminum billet) tracked by SMM stood at 929,000 mt, up 213,000 mt from pre-holiday levels (January 27), an increase of 29.8%, which aligns with expectations.On a YoY basis, the increase of 211,000 mt and growth rate of 30.6% during the same period last year showed little difference, with no anomalies observed. Over the past seven years, the average increase in domestic aluminum inventory during the Chinese New Year holiday was 210,000 mt, with an average growth rate of 24.2%. From this perspective,this year’s aluminum inventory buildup was slightly higher, primarily due to the supply side of aluminum:

According to SMM statistics, domestic aluminum production in January 2025 (31 days) increased by 3.8% YoY but declined by 0.3% MoM. By the end of January, SMM estimated the domestic aluminum existing capacity at approximately 45.71 million mt, with operating capacity around 43.51 million mt. The industry operating rate decreased by 0.04 percentage points MoM but increased by 2.29 percentage points YoY to 95.2%, mainly because aluminum supply in Yunnan since the end of 2024 did not experience production cuts or suspensions, differing from previous years. Currently, domestic aluminum smelters’ operating capacity remains largely stable, with only a minor production cut of 20,000 mt/year for technological transformation at a smelter in Shanxi. The production capacity reduced in Sichuan and Chongqing in December due to losses has no resumption plans yet. SMM will continue to monitor developments.

Regarding aluminum ingot inventory,according to SMM statistics, as of February 5, 2025, domestic aluminum ingot social inventory tracked by SMM was 654,000 mt, while circulating aluminum inventory was 528,000 mt, up 162,000 mt from pre-holiday levels (January 27), an increase of 32.9%.On a YoY basis, last year’s aluminum ingot inventory buildup during the Chinese New Year was 149,000 mt. This year, both the increase and growth rate of domestic aluminum ingot inventory exceeded last year’s levels. Over the past seven years, the average increase in domestic aluminum ingot inventory during the Chinese New Year holiday was 163,000 mt. This year’s increase is within the average range of recent years, but the growth rate ranks first in the past seven years, exerting some pressure on short-term aluminum prices after the holiday. The primary reason remains the aluminum supply side: in January, domestic aluminum operating capacity remained largely stable MoM, with only a minor production cut of 20,000 mt/year reported in Shanxi, and no resumption news for previously reduced capacity. Due to the holiday, the proportion of casting ingots increased in many regions during the month, while the proportion of liquid aluminum decreased by 2.9 percentage points MoM and 1.0 percentage point YoY. Based on SMM’s liquid aluminum proportion data, domestic aluminum casting ingot production in January increased by 7.3% YoY to approximately 1.13 million mt. Among provinces, Xinjiang, Yunnan, and Inner Mongolia ranked as the top three in casting ingot production.

By region,east China became the main contributor to inventory buildup during the Chinese New Year holiday, primarily due to a relatively small Guangdong-Shanghai price spread before the holiday and a higher Henan-Shanghai price spread compared to the same period last year. As a result, east China became the preferred destination for supplies from Xinjiang and other northern regions.During the holiday, Wuxi’s inventory increased by 85,000 mt to 258,000 mt, compared to an increase of 70,000 mt to 189,000 mt during the same period last year. Gongyi’s inventory increased by 39,000 mt to 91,000 mt, compared to 38,000 mt to 114,000 mt last year. Foshan’s inventory increased by 32,000 mt to 172,000 mt, compared to 28,000 mt to 177,000 mt last year.According to an SMM survey, some aluminum smelters offered varying degrees of discounts to aluminum billet enterprises and other downstream processing plants during the Chinese New Year holiday. As a result, downstream alloy plants in south China reduced production less than those in north China. Foshan’s inventory buildup was still slightly higher than the same period last year, mainly due to differences in Yunnan’s supply compared to previous years.

Meanwhile, according to an SMM survey, Gongyi received a concentrated influx of shipments during the Chinese New Year holiday, primarily from north-west China, including Xinjiang. During the holiday, major aluminum-producing regions supplying Gongyi (such as Xinjiang, Qinghai, and Inner Mongolia) experienced varying degrees of production cuts or suspensions at downstream processing plants, leading to higher casting ingot production. Before the holiday, Gongyi’s inventory was relatively low, prompting smelters to focus on restocking Gongyi during the holiday. Actual inventory in Gongyi should be higher, as some warehouses still have a large number of boxes piled up at stations, and inventory is expected to continue growing. However, there are also reports that post-holiday in-transit volumes to Gongyi are relatively manageable. Overall, Gongyi’s aluminum ingot inventory is expected to see a short-term rapid increase after the holiday, but the duration of this increase will likely be brief.

SMM believes that February is a period of inventory buildup for domestic aluminum ingots. Based on currently available data, information, and historical trends, domestic aluminum ingot inventory is expected to increase rapidly in the first half of February as downstream sectors remain on holiday before the Lantern Festival. In the second half of the month, as downstream operations resume post-holiday, the pace of inventory buildup is likely to slow significantly. Over the past seven years, only in 2021 did destocking occur in the fifth week after the holiday, with half of the years seeing destocking in the sixth week. Last year’s destocking inflection point was even further delayed.SMM expects that, with the anticipated “Golden March and Silver April” traditional peak season for downstream sectors and the gradual normalization of downstream operations, the first post-holiday destocking is likely to occur by the sixth week after the holiday or earlier. The domestic aluminum ingot inventory inflection point is expected to appear around mid-March, with the Q1 inventory peak likely reaching 850,000-900,000 mt. SMM will continue to monitor post-holiday downstream resumption and aluminum ingot in-transit conditions.

Regarding aluminum billet inventory,according to SMM statistics, as of February 5, 2025, domestic aluminum billet social inventory tracked by SMM was 275,000 mt, up 51,000 mt from pre-holiday levels (January 27), an increase of 22.8%.On a YoY basis, last year’s aluminum billet inventory buildup during the Chinese New Year was 62,000 mt. This year, both the increase and growth rate of domestic aluminum billet inventory were lower than last year. Over the past seven years, the average increase in domestic aluminum billet inventory during the Chinese New Year holiday was 47,000 mt. This year’s aluminum billet inventory buildup exceeded the recent average, while the growth rate was within the average range of recent years.

However, the growth rate ranks first in the past seven years, exerting some pressure on short-term aluminum prices after the holiday. The primary reason remains the aluminum supply side: in January, domestic aluminum operating capacity remained largely stable MoM, with only a minor production cut of 20,000 mt/year reported in Shanxi, and no resumption news for previously reduced capacity. Due to the holiday, the proportion of casting ingots increased in many regions during the month, while the proportion of liquid aluminum decreased by 2.9 percentage points MoM and 1.0 percentage point YoY. Based on SMM’s liquid aluminum proportion data, domestic aluminum casting ingot production in January increased by 7.3% YoY to approximately 1.13 million mt. Among provinces, Xinjiang, Yunnan, and Inner Mongolia ranked as the top three in casting ingot production.

Regarding aluminum ingot inventory,according to SMM statistics, as of February 5, 2025, domestic aluminum ingot social inventory tracked by SMM was 654,000 mt, while circulating aluminum inventory was 528,000 mt, up 162,000 mt from pre-holiday levels (January 27), an increase of 32.9%.On a YoY basis, last year’s aluminum ingot inventory buildup during the Chinese New Year was 149,000 mt. This year, both the increase and growth rate of domestic aluminum ingot inventory exceeded last year’s levels. Over the past seven years, the average increase in domestic aluminum ingot inventory during the Chinese New Year holiday was 163,000 mt. This year’s increase is within the average range of recent years, but the growth rate ranks first in the past seven years, exerting some pressure on short-term aluminum prices after the holiday. The primary reason remains the aluminum supply side: in January, domestic aluminum operating capacity remained largely stable MoM, with only a minor production cut of 20,000 mt/year reported in Shanxi, and no resumption news for previously reduced capacity. Due to the holiday, the proportion of casting ingots increased in many regions during the month, while the proportion of liquid aluminum decreased by 2.9 percentage points MoM and 1.0 percentage point YoY. Based on SMM’s liquid aluminum proportion data, domestic aluminum casting ingot production in January increased by 7.3% YoY to approximately 1.13 million mt. Among provinces, Xinjiang, Yunnan, and Inner Mongolia ranked as the top three in casting ingot production.

By region,east China became the main contributor to inventory buildup during the Chinese New Year holiday, primarily due to a relatively small Guangdong-Shanghai price spread before the holiday and a higher Henan-Shanghai price spread compared to the same period last year. As a result, east China became the preferred destination for supplies from Xinjiang and other northern regions.During the holiday, Wuxi’s inventory increased by 85,000 mt to 258,000 mt, compared to an increase of 70,000 mt to 189,000 mt during the same period last year. Gongyi’s inventory increased by 39,000 mt to 91,000 mt, compared to 38,000 mt to 114,000 mt last year. Foshan’s inventory increased by 32,000 mt to 172,000 mt, compared to 28,000 mt to 177,000 mt last year.According to an SMM survey, some aluminum smelters offered varying degrees of discounts to aluminum billet enterprises and other downstream processing plants during the Chinese New Year holiday. As a result, downstream alloy plants in south China reduced production less than those in north China. Foshan’s inventory buildup was still slightly higher than the same period last year, mainly due to differences in Yunnan’s supply compared to previous years.

Meanwhile, according to an SMM survey, Gongyi received a concentrated influx of shipments during the Chinese New Year holiday, primarily from north-west China, including Xinjiang. During the holiday, major aluminum-producing regions supplying Gongyi (such as Xinjiang, Qinghai, and Inner Mongolia) experienced varying degrees of production cuts or suspensions at downstream processing plants, leading to higher casting ingot production. Before the holiday, Gongyi’s inventory was relatively low, prompting smelters to focus on restocking Gongyi during the holiday. Actual inventory in Gongyi should be higher, as some warehouses still have a large number of boxes piled up at stations, and inventory is expected to continue growing. However, there are also reports that post-holiday in-transit volumes to Gongyi are relatively manageable. Overall, Gongyi’s aluminum ingot inventory is expected to see a short-term rapid increase after the holiday, but the duration of this increase will likely be brief.

SMM believes that February is a period of inventory buildup for domestic aluminum ingots. Based on currently available data, information, and historical trends, domestic aluminum ingot inventory is expected to increase rapidly in the first half of February as downstream sectors remain on holiday before the Lantern Festival. In the second half of the month, as downstream operations resume post-holiday, the pace of inventory buildup is likely to slow significantly. Over the past seven years, only in 2021 did destocking occur in the fifth week after the holiday, with half of the years seeing destocking in the sixth week. Last year’s destocking inflection point was even further delayed.SMM expects that, with the anticipated “Golden March and Silver April” traditional peak season for downstream sectors and the gradual normalization of downstream operations, the first post-holiday destocking is likely to occur by the sixth week after the holiday or earlier. The domestic aluminum ingot inventory inflection point is expected to appear around mid-March, with the Q1 inventory peak likely reaching 850,000-900,000 mt. SMM will continue to monitor post-holiday downstream resumption and aluminum ingot in-transit conditions.