This Week's Review

This week, imported iron ore prices rose strongly. A series of macroeconomic data was released this week, including the US December unadjusted core CPI YoY at 3.2%, slightly below expectations, which heightened expectations for an interest rate cut. Domestically, the GDP growth rate for the full year of 2025 reached 5%, slightly exceeding expectations. Meanwhile, Pan Gongsheng, Governor of the People's Bank of China, stated at the Asian Financial Forum that risks in China's real estate market have significantly decreased, and overall market transactions have improved. These positive macroeconomic developments boosted market sentiment. On the fundamentals side, heavy rainfall in the Southern Hemisphere caused Brazil's shipments to drop by 25%, reducing supply. However, despite a slight rebound in pig iron demand driving iron ore demand, steel mills had nearly completed their pre-holiday restocking, leading to reduced purchasing enthusiasm. This suppressed port spot prices for iron ore, narrowing the spot-futures price spread. In terms of port prices, PB fines in Shandong rose by 20-25 yuan/mt WoW.

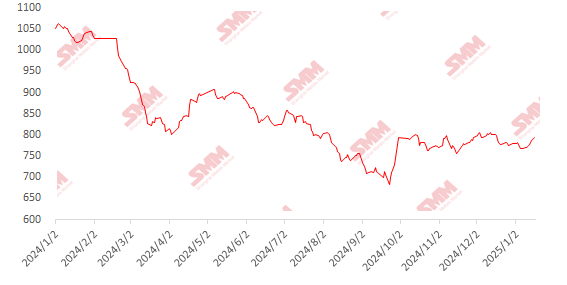

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

Domestic Ore Prices Show Mixed Performance This Week; Domestic Ore Prices Expected to Have Some Upward Potential Next Week

This week, prices in Tangshan, Qian'an, and Qianxi in Hebei rose by 10-15 yuan, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping remained stable. Prices in east China fell by 10-20 yuan.

Tangshan MarketIron ore concentrate transactions were relatively sluggish overall. As the Chinese New Year approaches, more beneficiation plants have halted production for maintenance. Due to high raw material costs, most quotes remained firm. Intermediate traders were cautious about purchasing, considering current inventory and cost issues. Steel mills mainly purchased as needed, with in-plant inventory at relatively low levels. Demand was weaker compared to the same period in previous years, and the market was in a state of weak supply and demand. Considering the recent strong futures market performance for iron ore, local market transaction activity may increase, and local iron ore concentrate prices may have some short-term upward potential.

West Liaoning MarketDomestic ore transactions were weak, with local trade inquiries relatively quiet and mainly focused on long-term contracts. Sentiment was largely wait-and-see. As the year-end approaches, some beneficiation plants are gradually halting production, exacerbating the tight supply of local iron ore concentrate, which provided some support for local prices. Local steel mills continued some restocking operations before the holiday, leading to a temporary improvement in demand. Local iron ore concentrate prices are expected to have some upward potential in the near term.

East China RegionCurrently, beneficiation plants are mostly operating normally, producing and selling as needed, with no significant inventory pressure. From a pricing perspective, the average price index for imported ore rose slightly WoW this week. Local ore prices are expected to have some upward potential next week.

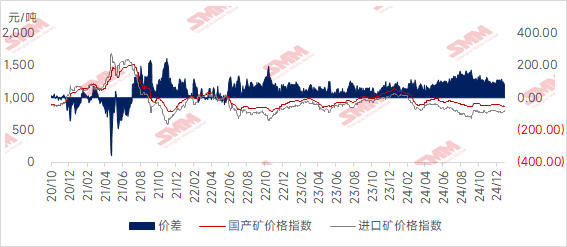

Considering both domestic and imported ore prices, imported ore prices rose significantly this week, narrowing the price spread between domestic and imported ore. The price spread is expected to widen next week.

Outlook for Next Week

For imported ore:Affected by Australian cyclones and the Southern Hemisphere rainy season, global shipments are expected to decline, but port arrivals may still increase slightly. On the demand side, according to SMM's blast furnace maintenance data, the number of blast furnaces resuming production next week is expected to exceed those undergoing maintenance, leading to a larger increase in pig iron production. Considering that steel mills will have largely completed pre-holiday restocking next week, support for ore prices will weaken. Additionally, with Trump's inauguration, market risk aversion has increased. Therefore, iron ore prices are expected to face reduced upward momentum next week, with a risk of pulling back from highs.

For domestic ore:Domestic iron ore concentrate resources remain tight, providing some support for prices. According to SMM's tracking data, pig iron production from steel mills' blast furnaces continues to rise, which may support short-term demand for iron ore concentrate. Domestic iron ore concentrate prices are expected to have some upward potential next week.

》Click to View the SMM Metal Industry Chain Database