SMM January 17 News:

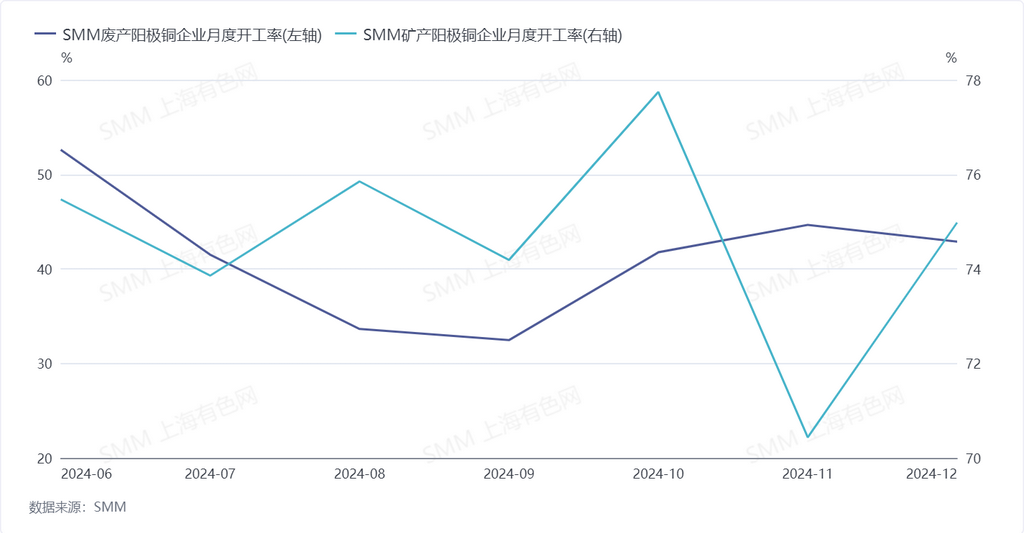

According to SMM, the operating rate of copper anode producers in December 2024 was 55.2%, up 0.66 percentage points MoM. By raw material, the operating rate of copper anode producers using ore was 74.98% (up 4.54 percentage points MoM), while that of copper anode producers using scrap was 42.88% (down 1.77 percentage points MoM). (This refers only to non-self-used copper anodes.)

The increase in the operating rate of copper anode producers using ore in December was mainly due to production recovery after maintenance at some enterprises and capacity ramp-up at others. Meanwhile, the decline in the operating rate of copper anode producers using scrap was attributed to two factors: first, the downward shift in copper price center in December, which heightened the sentiment of holding back cargoes among secondary copper suppliers; second, the previous suspension of operations at Malaysian ports, which reduced the availability of imported cargoes. The rise in procurement costs for copper scrap raw materials further led to a decline in the production of copper anodes using scrap.

SMM expects the overall operating rate of copper anode producers to decrease by 6.20 percentage points MoM to 49.00% in January 2025. Among them, the operating rate of copper anode producers using ore is expected to rise to 83.20% (up 8.22 percentage points MoM), while that of copper anode producers using scrap is expected to drop to 27.71% (down 15.17 percentage points MoM).

The growth in the operating rate of copper anode producers using ore in January is still mainly due to production recovery after maintenance at some enterprises. For copper anode producers using scrap, the significant decline in the operating rate in January is primarily due to the Chinese New Year holiday, during which most of these enterprises will gradually suspend operations from late January. Additionally, from the perspective of secondary copper raw materials, the uncertainty surrounding trade policies as Trump is about to take office has led traders to suspend imports of US secondary copper raw materials since late November, and the import volume of copper scrap in January is expected to decline. Furthermore, during the transitional phase of the "reverse invoicing" policy, some enterprises have adopted a wait-and-see attitude. Overall, domestic copper anode production in January is expected to show a significant decline.