This week, the total inventory of construction steel continued to increase, albeit at a relatively slow pace. Among them, rebar inventory rose 1.92% WoW, while wire rod inventory increased 1.05% WoW. During the week, favorable macro news boosted the ferrous metals futures, driving up market sentiment. Many steel mills slightly raised prices, and some introduced winter stockpiling policies, significantly improving market purchasing enthusiasm compared to earlier periods. However, as the Chinese New Year approaches, the weakening trend in end-use consumption remains unchanged, leading to a continued increase in the total inventory of construction steel this week.

This week, the total rebar inventory reached 3.9561 million mt, up 74,400 mt WoW (+1.92%, previous value +2.4%), but down 3.1989 million mt YoY (-44.71%, previous value -39.31%).

Table 1: Overview of Rebar Inventory

Source: SMM

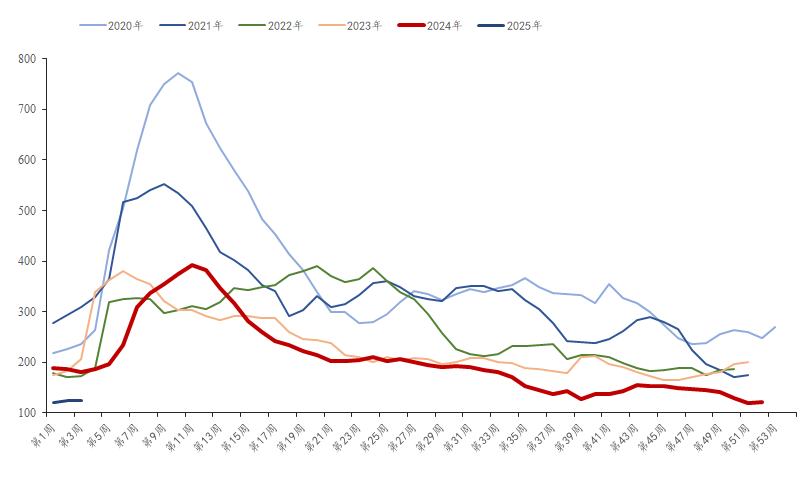

This week, in-plant rebar inventory stood at 1.2493 million mt, down 1,400 mt WoW (-0.11%, previous value +3.5%), and decreased by 725,800 mt YoY (-36.75%, previous value -33.32%). Spot prices followed the futures upward, winter stockpiling sales by steel mills were moderate, and in-plant inventory slightly declined.

Chart-1: Rebar In-Plant Inventory Trends, 2019-2024

Source: SMM

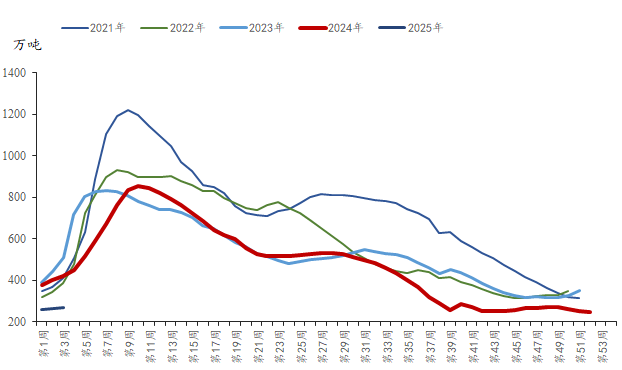

This week, social rebar inventory reached 2.7068 million mt, up 75,800 mt WoW (+2.88%, previous value +1.88%), but down 2.4731 million mt YoY (-47.74%, previous value -41.8%). With the annual Spring Festival travel rush beginning, terminal projects across regions gradually started holiday arrangements, weakening downstream demand. Market resource circulation mainly focused on winter stockpiling, leading to a slight increase in overall spot inventory.

Chart-2: Rebar Social Inventory Trends, 2019-2024

Source: SMM

Looking ahead, according to the SMM survey, sample EAF steel mills are expected to reach their peak holiday period between January 15 and 20, with most entering their annual break next week and resuming operations around the 10th to 15th day of the Chinese New Year. Blast furnace steel mills are seeing fewer new maintenance activities, with production stabilizing. Regarding demand, market traders are expected to gradually begin their Chinese New Year break next week, with post-holiday resumption of terminal projects delayed as workers return to their hometowns during the Spring Festival travel rush, further reducing demand. Only government-backed projects in certain regions will continue construction. With winter stockpiling largely completed, spot prices in the market are expected to stabilize next week, while the inventory buildup of construction steel is likely to accelerate.