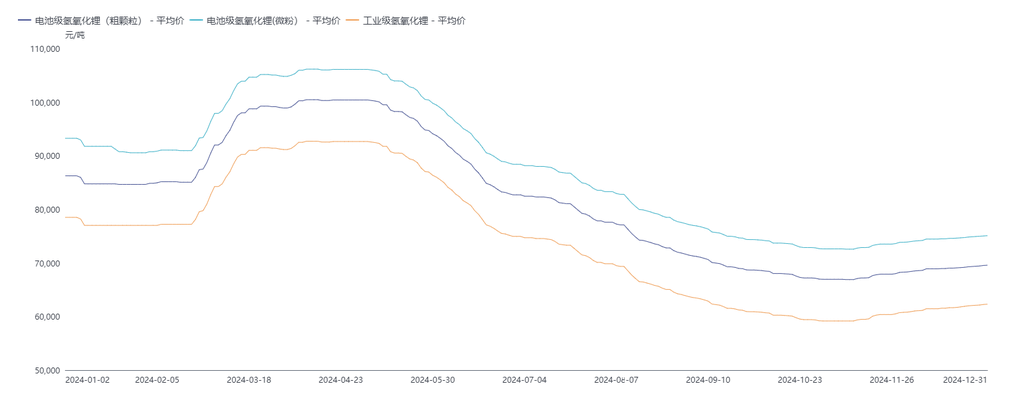

1. Price Review

The performance of lithium hydroxide prices in 2024 can be divided into four phases:

January to mid-February: The supply-demand pattern improved, and lithium hydroxide prices stabilized after a decline.

In January, on one hand, the stabilization of lithium ore and lithium carbonate prices strengthened cost support for lithium hydroxide production, leading to a stronger sentiment to stand firm on quotes among suppliers. On the other hand, some domestic and overseas downstream producers picked up goods in advance before the Chinese New Year, resulting in a trend of deep destocking for lithium hydroxide, which improved the supply-demand pattern and gradually stabilized prices after a rapid decline. In early February, downstream restocking continued, while during the holiday in mid-February, market transactions were nearly stagnant due to logistics suspension, and overall prices remained stable.

Late February to early May: The supply-demand pattern improved, and lithium hydroxide prices rose.

In late February, driven by the rise in lithium carbonate prices, the sentiment of holding back sales among suppliers strengthened, reducing market circulation and stimulating some downstream restocking demand, which pushed up spot transaction prices. March and April continued the upward trend from late February. The sustained rebound in lithium carbonate prices and bullish expectations for the market further strengthened the sentiment to stand firm on quotes among lithium hydroxide suppliers. With long-term contracts accounting for most shipments and spot orders being withheld, market circulation further decreased. Meanwhile, downstream demand recovered well after the holiday, and production schedules increased significantly. Due to low inventory levels and a significant reduction in customer-supplied materials, some cathode producers faced raw material supply gaps and were forced to purchase at high prices, driving up spot prices. By late April, although the supply-demand pattern transitioned to a more relaxed state, pre-Labor Day restocking by some ternary material producers supported prices to remain high and stable until early May.

Late May to early November: Weak demand for high-nickel products deepened the surplus of lithium hydroxide, and prices declined continuously.

Due to persistently weak demand for high-nickel products, coupled with a high proportion of long-term contracts and a significant increase in the proportion of long-term supply for cathode materials, the supply-demand pattern remained weak, and industry inventory continued to rise. Dragged down by falling lithium carbonate prices, lithium hydroxide prices declined continuously. By late October, as lithium carbonate prices rebounded, lithium hydroxide prices slowed their decline at low levels.

Mid-to-late November to December: Supply-side reductions supported prices, and market prices edged up.

With prices at low levels and the widening price spread between lithium carbonate and lithium hydroxide, upstream salt plants showed unprecedented sentiment to stand firm on quotes, raising long-term contract discounts and holding back spot orders, which boosted the center of market transaction prices. Before year-end, production reductions due to maintenance and the flexible production line switch to lithium carbonate further supported the sentiment to stand firm on quotes. Some demand-side players engaged in spot order stockpiling due to the uncertainty of long-term contracts for the new year, pushing prices upward. However, with overall demand remaining weak, the upward momentum was limited, and overall prices showed a slow upward trend.

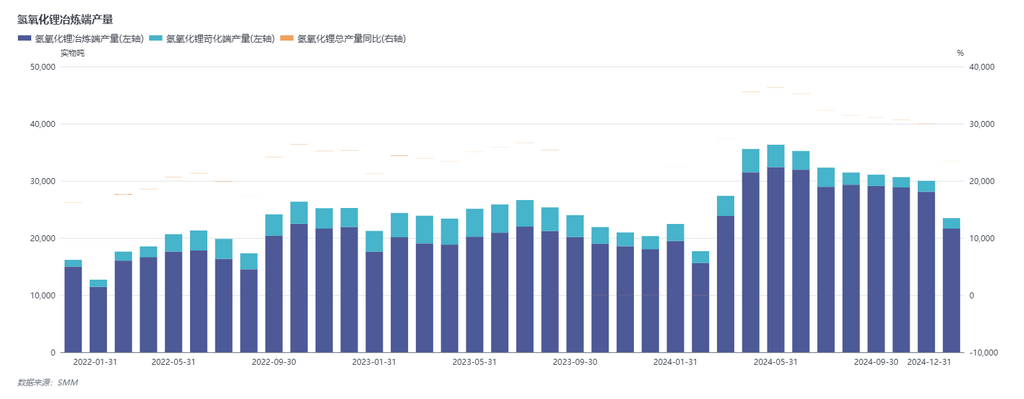

2. Supply-Side Review

In 2024, China's lithium hydroxide production reached 354,000 mt, up 25% YoY. By raw material, smelting contributed 321,000 mt, accounting for approximately 91%, up about 51% YoY. In H1, the release of new capacity from integrated smelters in China brought some incremental production of lithium hydroxide. However, in H2, especially in Q4, the widening price spread between lithium carbonate and lithium hydroxide and weak demand limited the production increase, as more companies switched flexible smelting lines to lithium carbonate. On the causticisation side, production in 2024 was 33,000 mt. The widening price spread between lithium carbonate and lithium hydroxide kept causticisation in a state of losses almost throughout the year, with operating rates of old capacity declining and new production lines ramping up slower than expected, keeping overall production at low levels. From the current CR5 market share changes, the industry concentration of lithium hydroxide producers has reached 79%, relatively high. The market share of integrated lithium chemical plants has increased, further enhancing their pricing power.

According to customs data, China's lithium hydroxide exports in 2024 were approximately 120,000 mt, down 6.7% YoY. Japan and South Korea remained the main export destinations, with exports to South Korea at 83,400 mt, down about 10% YoY, accounting for 70% of total exports. Exports to Japan were approximately 32,000 mt, up about 4% YoY, accounting for 27% of total exports.

On the import side, imports in 2024 were approximately 8,000 mt, up about 1.1 times YoY. Structurally, imports from Chile decreased significantly, while imports from Australia increased notably, mainly due to the ramp-up of lithium hydroxide production lines in Australia by China.

3. Demand-Side Review

In 2024, China's demand for lithium hydroxide was 204,000 mt, up 16% YoY, but the growth rate fell short of expectations. Approximately 96% was used for ternary cathode materials, and 4% for traditional industries. In H1, during March and April, the successive launches of domestic new energy vehicles and price cuts among automakers stimulated car-end demand to grow beyond expectations, boosting orders for mid-to-high nickel cathode producers downstream. However, the price-cutting promotions consumed future demand in advance, and mid-year consumption of high-nickel ternary vehicles fell short of expectations. Meanwhile, cathode producers increased customer-supplied lithium hydroxide volumes and actively adopted destocking strategies to consume customer-supplied raw materials, weakening demand for lithium hydroxide. In H2, the electrification process in major markets like Europe and the US slowed, underperforming expectations, leading to almost no incremental demand for ternary materials. Combined with high inventories of lithium hydroxide at downstream and end-user levels, demand for lithium hydroxide remained weak. At year-end, due to policy uncertainties brought by the US presidential election, Chinese battery manufacturers rushed to export in Q4, resulting in better-than-usual orders for ternary materials. However, this essentially represented an early release of 2025 mid-year demand, which could lead to a pullback in future demand.

4. Supply-Demand Balance

In 2024, lithium hydroxide experienced an inventory buildup, with an annual surplus of approximately 36,000 mt and cumulative sample inventory of about 56,000 mt. Before April, pre-holiday stockpiling on the demand side and supply-side production reductions due to Chinese New Year maintenance and output cuts led to some destocking in the market. After April, with the ramp-up of new production lines by some companies and weakening demand, lithium hydroxide began to see inventory buildup. By November and December, significant production cuts on the supply side and slight demand reductions led to some inventory destocking, but the extent was limited.

II. Outlook for 2025

On the demand side, at the battery cell and battery levels, ternary battery production is expected to decrease toward year-end due to inventory control and expectations of a rush for installations. Moving forward, the continuous implementation of anti-subsidy policies in Europe and the US, along with the erosion of the ternary market by cost-effective lithium iron phosphate car models, will limit the incremental space for ternary power end-users. The weakness in ternary power will transmit upstream to demand for ternary materials, with ternary material production and performance also expected to remain subdued.

On the supply side, by the end of Q4 2024, due to overall weak demand, flexible production lines at lithium chemical plants increasingly switched to lithium carbonate. Combined with high inventories at some lithium chemical plants and production cuts for destocking, supply reductions were significant. Considering the Chinese New Year holiday, maintenance, and shutdown expectations, Q1 2025 production is expected to remain at low levels. Subsequently, production may see a slight increase due to cyclical demand recovery and post-holiday resumption of work. In the long term, with the ternary market at home and abroad remaining weak, annual demand is expected to decline. On the export side, limited overseas demand growth is expected due to anticipated policies from the new US administration in 2025 that may suppress the power market. Additionally, the ramp-up of new overseas capacity and continued inventory buildup of lithium hydroxide at overseas end-users and material plants will limit overseas demand growth for China's lithium hydroxide.

In 2025, lithium hydroxide supply and demand are both expected to decrease, with the market likely to remain in a slight surplus, and overall inventory buildup is expected to increase further. Lithium hydroxide prices are likely to continue declining. Although the persistent sentiment to stand firm on quotes for overseas ore prices and lithium carbonate prices may strengthen cost support for lithium hydroxide, from the demand perspective, the downstream and end-user sectors will continue to face pressure from the lithium iron phosphate system, with a more pronounced weakening trend in demand. The market transaction center is expected to continue its downward trend.