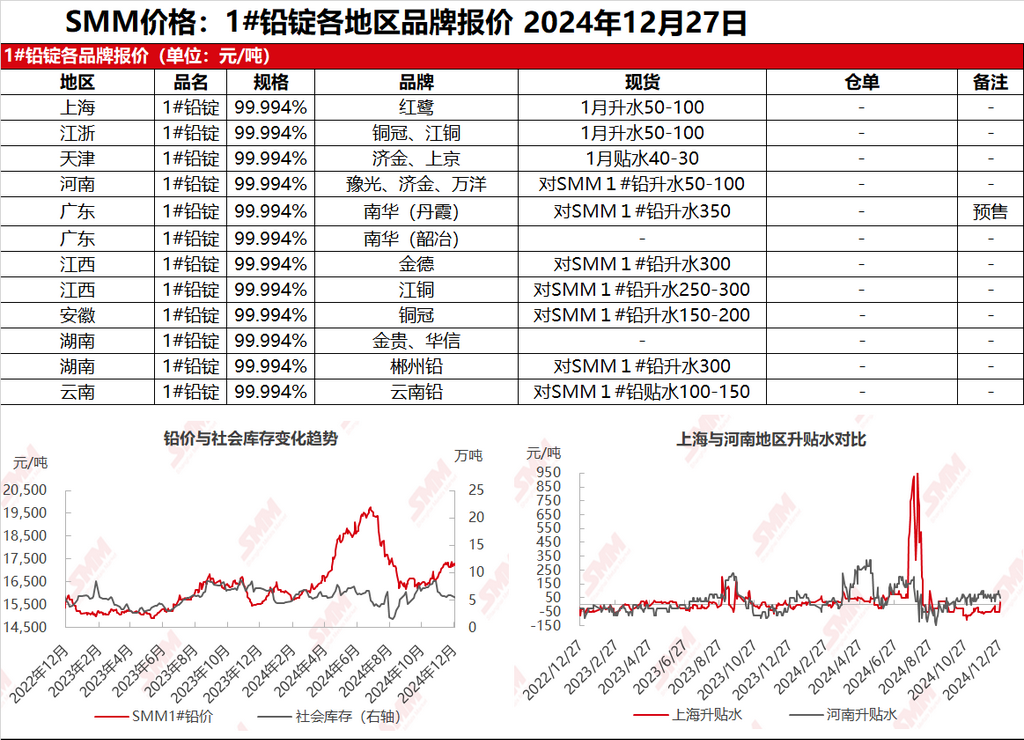

SMM, December 27: In the Shanghai market, Honglu lead was quoted at 17,000-17,100 yuan/mt, with a premium of 50-100 yuan/mt against the SHFE lead 2501 contract. In the Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 17,000-17,100 yuan/mt, with a premium of 50-100 yuan/mt against the SHFE lead 2501 contract. After the opening of SHFE lead, prices continued to decline sharply, quickly breaking below the 17,000 yuan threshold to hit a one-month low. Suppliers' panic sentiment increased, and most quotations shifted to premiums. Some suppliers were reluctant to sell at low prices and adopted a wait-and-see attitude. During this period, the circulation of cargoes self-picked up from production sites by smelters further decreased, and secondary refined lead producers also remained cautious with limited sales. Meanwhile, year-end factors such as account settlements and invoices persisted, leaving downstream enterprises mostly in a wait-and-see mode. Although inquiries increased, transaction activity continued to weaken.

Other markets: Today, the SMM 1# lead average price fell by 250 yuan/mt compared to the previous trading day. As the year-end approached, downstream enthusiasm for raw material stocking remained low, and market transactions stayed sluggish. In Henan, a small volume of spot cargoes was quoted at a premium of 50-100 yuan/mt against the SMM 1# lead average price. In Hunan, smelters had extremely limited circulating cargoes, and after depleting their inventories, they suspended quotations. A few suppliers were reluctant to sell at a premium of 300 yuan/mt against the SMM 1# lead average price. While downstream buyers actively inquired and sought to buy the dip, circulating cargoes remained tight in some regions, and market transaction activity showed no significant improvement.