SHANGHAI, Dec 23 (SMM) - This is a roundup of China's metals weekly inventory as of December 23.

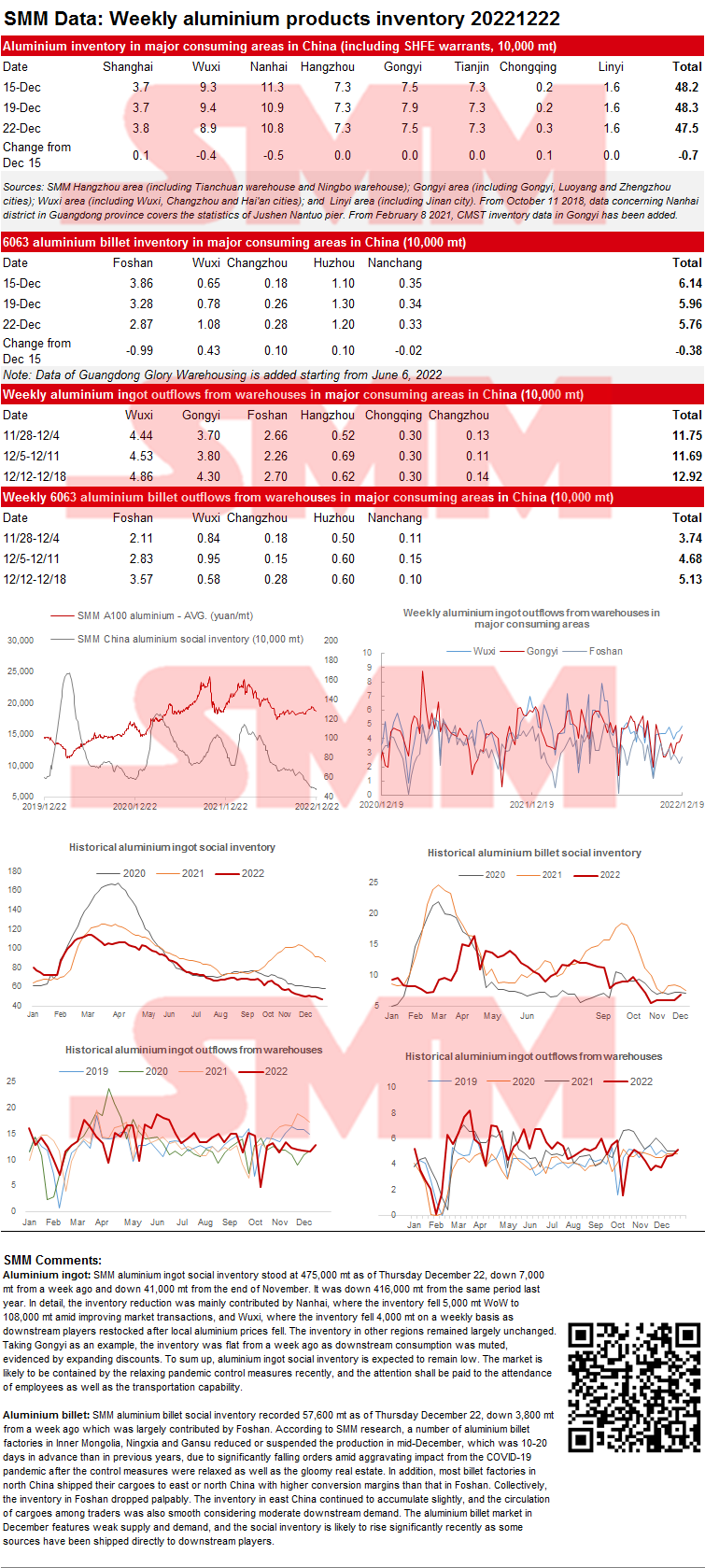

SMM Aluminium Ingot and Billet Social Inventory both Falls

Aluminium ingot: SMM aluminium ingot social inventory stood at 475,000 mt as of Thursday December 22, down 7,000 mt from a week ago and down 41,000 mt from the end of November. It was down 416,000 mt from the same period last year. In detail, the inventory reduction was mainly contributed by Nanhai, where the inventory fell 5,000 mt WoW to 108,000 mt amid improving market transactions, and Wuxi, where the inventory fell 4,000 mt on a weekly basis as downstream players restocked after local aluminium prices fell. The inventory in other regions remained largely unchanged. Taking Gongyi as an example, the inventory was flat from a week ago as downstream consumption was muted, evidenced by expanding discounts. To sum up, aluminium ingot social inventory is expected to remain low. The market is likely to be contained by the relaxing pandemic control measures recently, and the attention shall be paid to the attendance of employees as well as the transportation capability.

Aluminium billet: SMM aluminium billet social inventory recorded 57,600 mt as of Thursday December 22, down 3,800 mt from a week ago which was largely contributed by Foshan. According to SMM research, a number of aluminium billet factories in Inner Mongolia, Ningxia and Gansu reduced or suspended the production in mid-December, which was 10-20 days in advance than in previous years, due to significantly falling orders amid aggravating impact from the COVID-19 pandemic after the control measures were relaxed as well as the gloomy real estate. In addition, most billet factories in north China shipped their cargoes to east or north China with higher conversion margins than that in Foshan. Collectively, the inventory in Foshan dropped palpably. The inventory in east China continued to accumulate slightly, and the circulation of cargoes among traders was also smooth considering moderate downstream demand. The aluminium billet market in December features weak supply and demand, and the social inventory is likely to rise significantly recently as some sources have been shipped directly to downstream players.

Copper Inventory in Major Chinese Markets Dips 5,700 mt from Monday

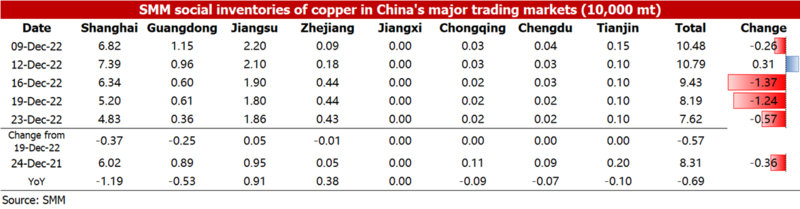

As of Friday December 23, SMM copper inventory across major Chinese markets dipped 5,700 mt from Monday to 76,200 mt, down 18,100 mt from last Friday, a new low since the National Day holiday in 2022. In detail, the inventory in Shanghai dropped 3,700 mt to 48,300 mt, down 11,900 mt from the same period last year when the figure was 60,200 mt, the inventory in Guangdong fell 2,500 mt to 3,600 mt, the inventory in Zhejiang dropped 100 mt to 4,300 mt, the inventory in Jiangxi, Tianjin, Sichuan and Chongqing remained unchanged, while the inventory in Jiangsu rose slightly.

In east China, the arrivals of imported copper were much lower than the shipments flowing out of the warehouses in the region. In Shanghai, the fall in copper prices at the beginning of the week boosted the downstream purchases, while the surging prices in mid-week suppressed the downstream companies’ buying interest. Therefore, the shipments flowing out of the warehouses in Shanghai increased compared with the recent average level. The Guangdong market witnessed zero arrivals of domestic copper and limited arrivals of imported copper, while the downstream companies maintained normal restocking, thus the inventory in Guangdong dropped.

SMM believes that the arrivals of imported copper will not balloon this week when New Year's Day is coming near. The spot transactions will be hindered by the rise in COVID-19-infected cases in China, which will slightly push up the inventory.

Social Inventory of Lead Ingots Declined Nearly 10,000 mt amid Downstream Stockpiling and Export Expectation

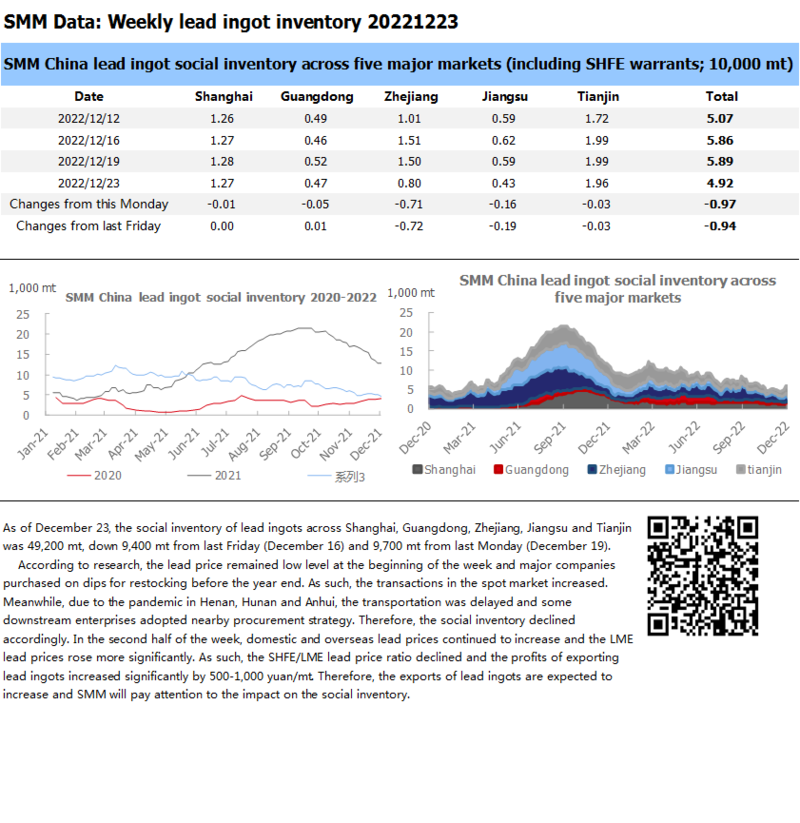

As of December 23, the social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin was 49,200 mt, down 9,400 mt from last Friday (December 16) and 9,700 mt from last Monday (December 19).

According to research, the lead price remained low level at the beginning of the week and major companies purchased on dips for restocking before the year end. As such, the transactions in the spot market increased. Meanwhile, due to the pandemic in Henan, Hunan and Anhui, the transportation was delayed and some downstream enterprises adopted nearby procurement strategy. Therefore, the social inventory declined accordingly. In the second half of the week, domestic and overseas lead prices continued to increase and the LME lead prices rose more significantly. As such, the SHFE/LME lead price ratio declined and the profits of exporting lead ingots increased significantly by 500-1,000 yuan/mt. Therefore, the exports of lead ingots are expected to increase and SMM will pay attention to the impact on the social inventory.

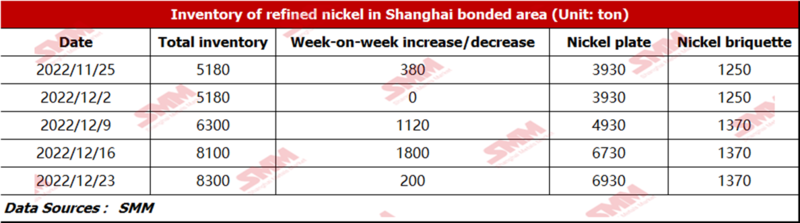

Nickel Inventories in Domestic Bonded Zone Grow Slightly from December 16 amid the Huge Import Losses

As of December 23, bonded zone inventory of nickel stood at 8,300 mt, with the inventory of nickel briquette and nickel plate of 1,370 mt and 6,930 mt respectively. The SHFE/LME nickel price ratio did not rise, and the import losses remained at around 10,000 yuan/mt, limiting the clearance volume of pure nickel this week. Besides, domestic salt factories dumped the nickel briquette owing to its lower cost efficiency. And the domestic demand for nickel briquettes declined. As a result, the bonded zone inventory of nickel plates grew more.

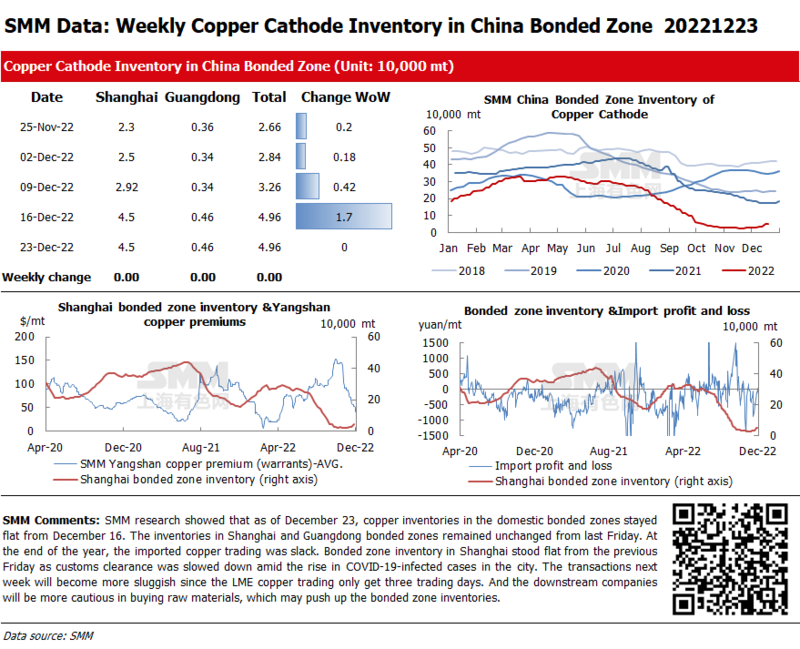

Copper Inventories in Domestic Bonded Zones Stay Flat from December 16

SMM research showed that as of December 23, copper inventories in the domestic bonded zones stayed flat from December 16. The inventories in Shanghai and Guangdong bonded zones remained unchanged from last Friday. At the end of the year, the imported copper trading was slack. Bonded zone inventory in Shanghai stood flat from the previous Friday as customs clearance was slowed down amid the rise in COVID-19-infected cases in the city. The transactions next week will become more sluggish since the LME copper trading only get three trading days. And the downstream companies will be more cautious in buying raw materials, which may push up the bonded zone inventories.

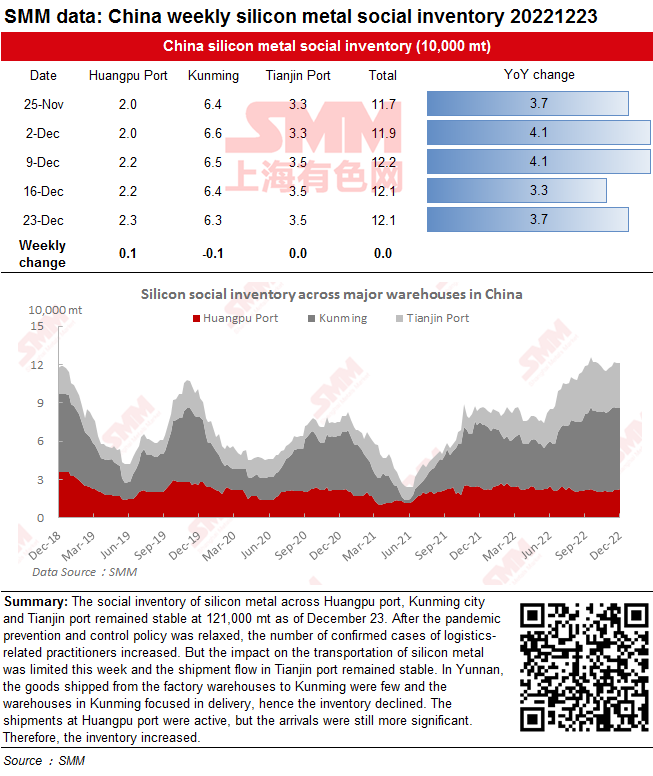

Social Inventory of Silicon Metal Remained Stable

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port remained stable at 121,000 mt as of December 23. After the pandemic prevention and control policy was relaxed, the number of confirmed cases of logistics-related practitioners increased. But the impact on the transportation of silicon metal was limited this week and the shipment flow in Tianjin port remained stable. In Yunnan, the goods shipped from the factory warehouses to Kunming were few and the warehouses in Kunming focused in delivery, hence the inventory declined. The shipments at Huangpu port were active, but the arrivals were still more significant. Therefore, the inventory increased.

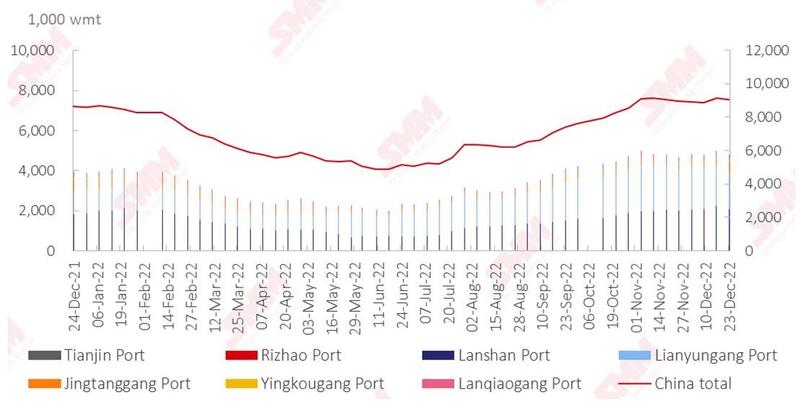

Nickel Ore Inventories at Chinese Ports Down 81,000 wmt WoW

As of December 23, inventory of nickel ore across Chinese ports dipped 81,000 wmt to 9.04 million wmt compared with last Friday. The total Ni content stood at around 71,000 mt. Port inventory of nickel ore across seven major Chinese ports stood at 4.81 million wmt, 181,000 wmt lower than last week. On the supply side, nickel ore shipments from the Philippines were restricted in the rainy season, tightening the market supply of nickel ore. On the demand side, pessimism filled the stainless steel market as the prices trended lower. Accordingly, the NPI plants could not accept high nickel ore prices, and they were less willing to produce, which could not boost the nickel ore imports. SMM believes that the port inventory of nickel ore will drop slowly.

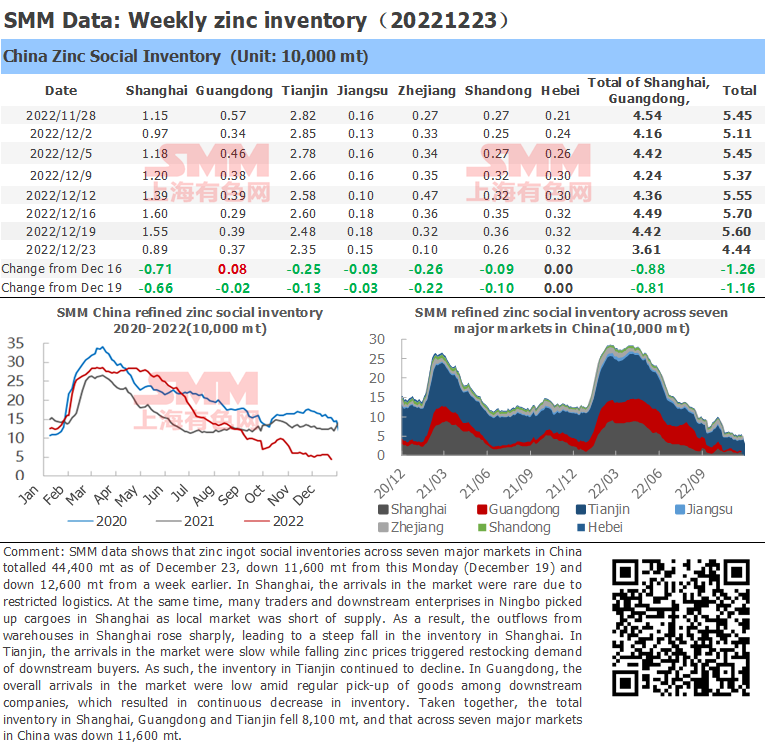

Zinc Ingot Social Inventory Down 11,600 mt from Monday

SMM data shows that zinc ingot social inventories across seven major markets in China totalled 44,400 mt as of December 23, down 11,600 mt from this Monday (December 19) and down 12,600 mt from a week earlier. In Shanghai, the arrivals in the market were rare due to restricted logistics. At the same time, many traders and downstream enterprises in Ningbo picked up cargoes in Shanghai as local market was short of supply. As a result, the outflows from warehouses in Shanghai rose sharply, leading to a steep fall in the inventory in Shanghai. In Tianjin, the arrivals in the market were slow while falling zinc prices triggered restocking demand of downstream buyers. As such, the inventory in Tianjin continued to decline. In Guangdong, the overall arrivals in the market were low amid regular pick-up of goods among downstream companies, which resulted in continuous decrease in inventory. Taken together, the total inventory in Shanghai, Guangdong and Tianjin fell 8,100 mt, and that across seven major markets in China was down 11,600 mt.