SMM Jan 30 News:

As of January 30, the most-traded SHFE zinc contract closed at 25,835 yuan/mt, up 2,525 yuan/mt for the month, a gain of 10.83%. Zinc prices rose significantly in January, hitting a low of 23,410 yuan/mt early in the month and reaching a high of 26,985 yuan/mt by month-end, with the overall price center shifting notably higher. With the Chinese New Year holiday approaching, how will zinc prices perform in February.

Macro perspective. In January, geopolitical conflicts overseas continued to emerge, with persistent geopolitical risks in Iran, Russia-Ukraine, Palestine-Israel, Greenland, and elsewhere, sustaining macro uncertainty. Amid safe-haven demand, liquidity increased, driving gold, silver, copper, aluminum, and other metals to new highs, with zinc prices also refreshing their highest level in over three years.

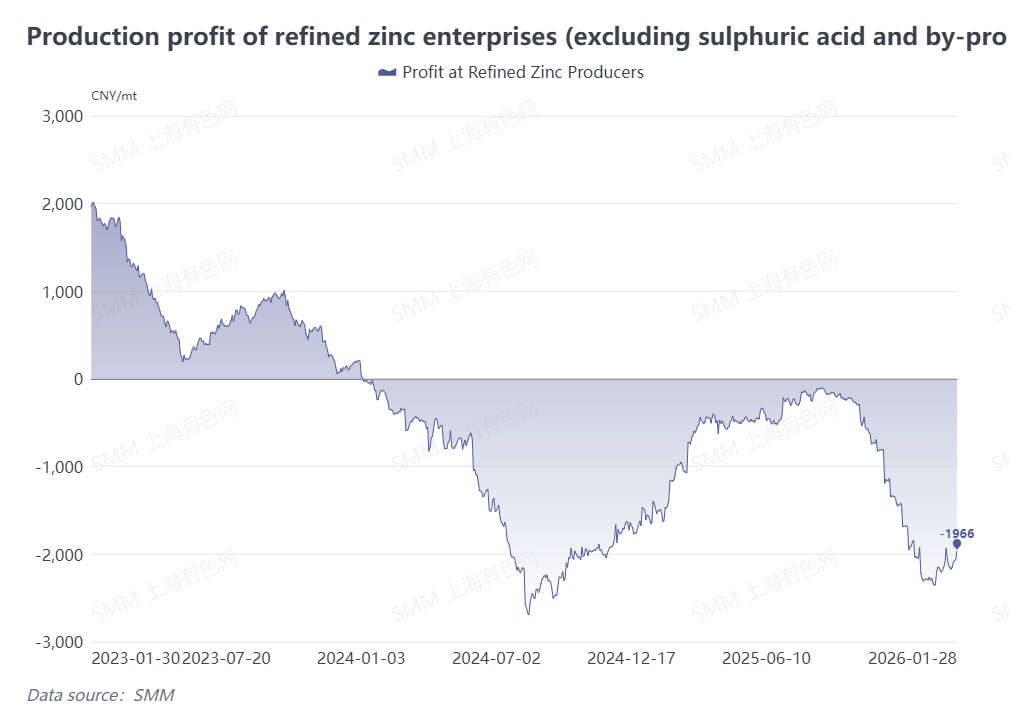

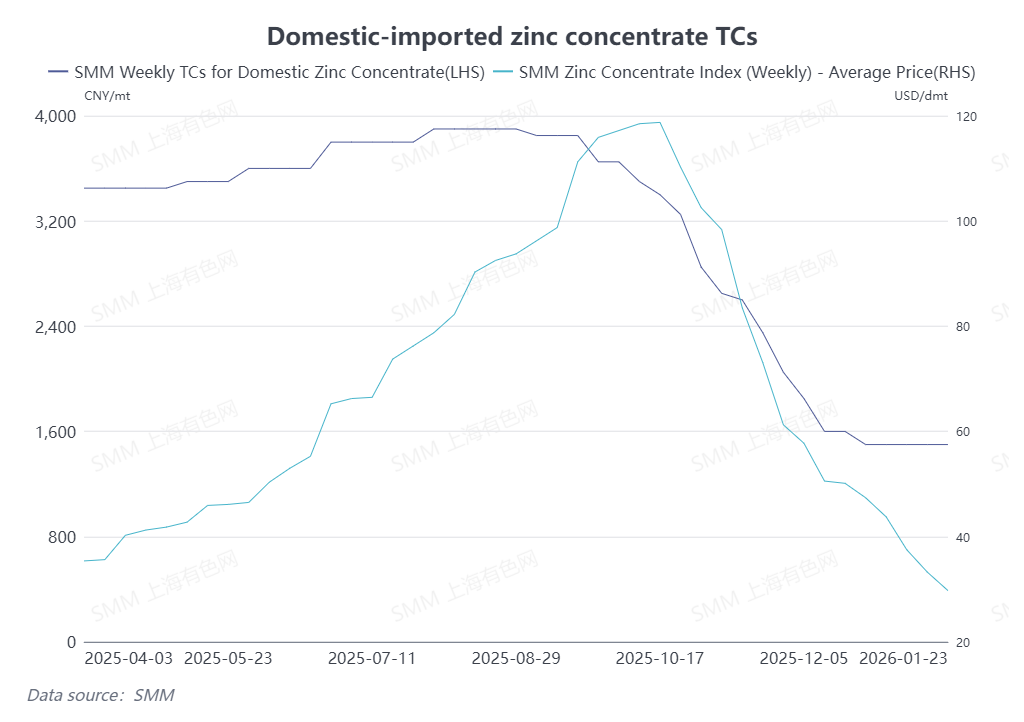

Supply side. According to SMM, domestic zinc concentrate TCs halted their decline in January but remained low. Currently, smelter profits excluding sulphuric acid and by-products are still in the red by around 2,000 yuan/mt. Smelters continued production cuts, and domestic refined zinc output remained low in January. February coincides with the Chinese New Year holiday, during which some smelters will undergo routine maintenance and shutdowns. Refined zinc production is expected to decline MoM, but domestic mines will also halt operations for the holiday. It will still take time for the domestic zinc concentrate supply-demand pattern to ease significantly.

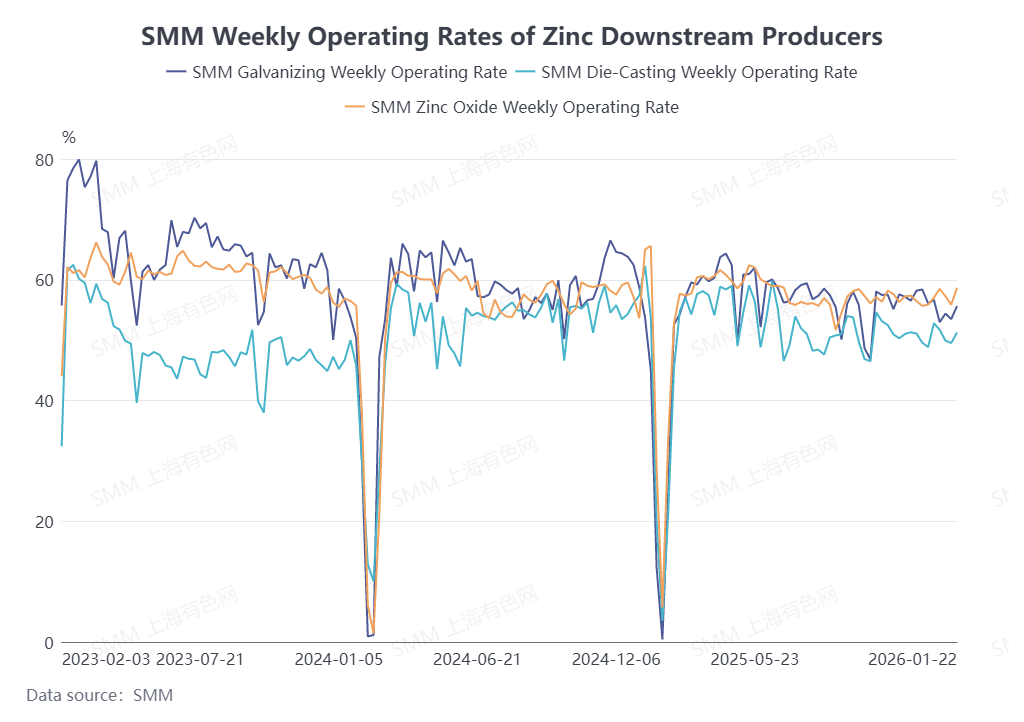

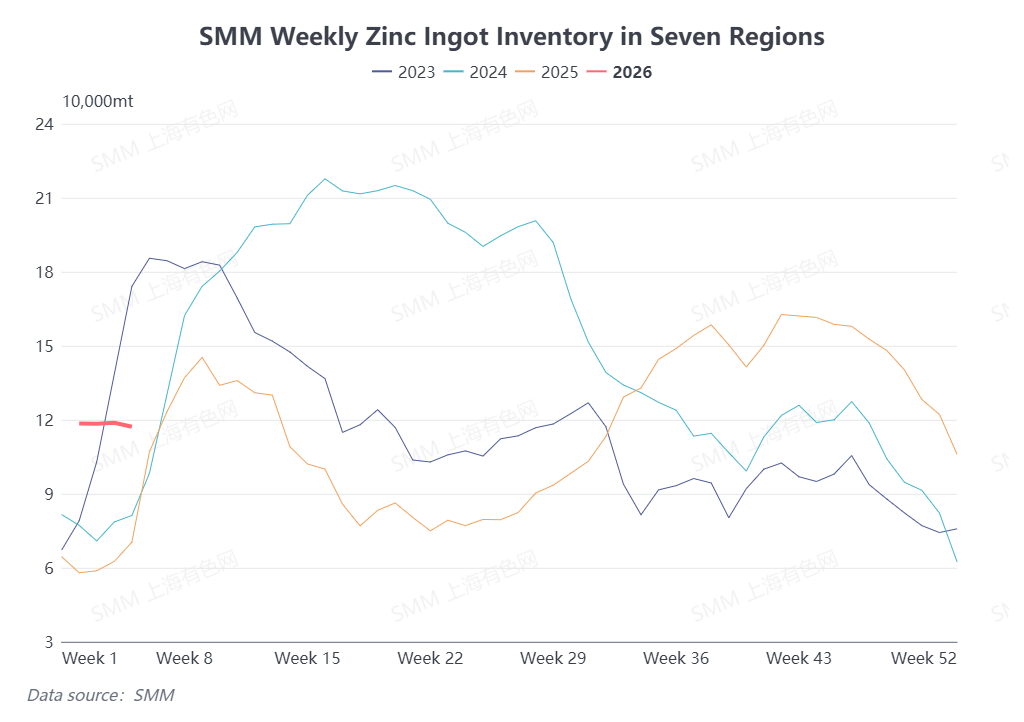

Demand side. As the Chinese New Year holiday approaches, downstream enterprise orders are weak in the early-year off-season. Starting from mid-January, domestic zinc downstream enterprises began taking holidays in succession, with the peak expected around late January to early February. Operating rates for galvanizing, zinc oxide, and zinc alloy sectors are projected to hit yearly lows in February, and weaker demand will reduce support for zinc prices. Additionally, domestic zinc ingot inventory usually builds up during the Chinese New Year period. A significant inventory buildup is expected in February, which is likely to exert some downward pressure on zinc prices.

Overall, January saw weak supply and demand for zinc, but positive macro sentiment and capital inflows boosted prices to an over three-year high. Looking ahead to February, with the Chinese New Year holiday approaching, domestic zinc ingot social inventory is expected to accumulate significantly, weakening fundamental support for zinc prices. However, macro risks remain high, requiring close attention to overseas geopolitical risks and other macro guidance.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)