SMM January 20 News:

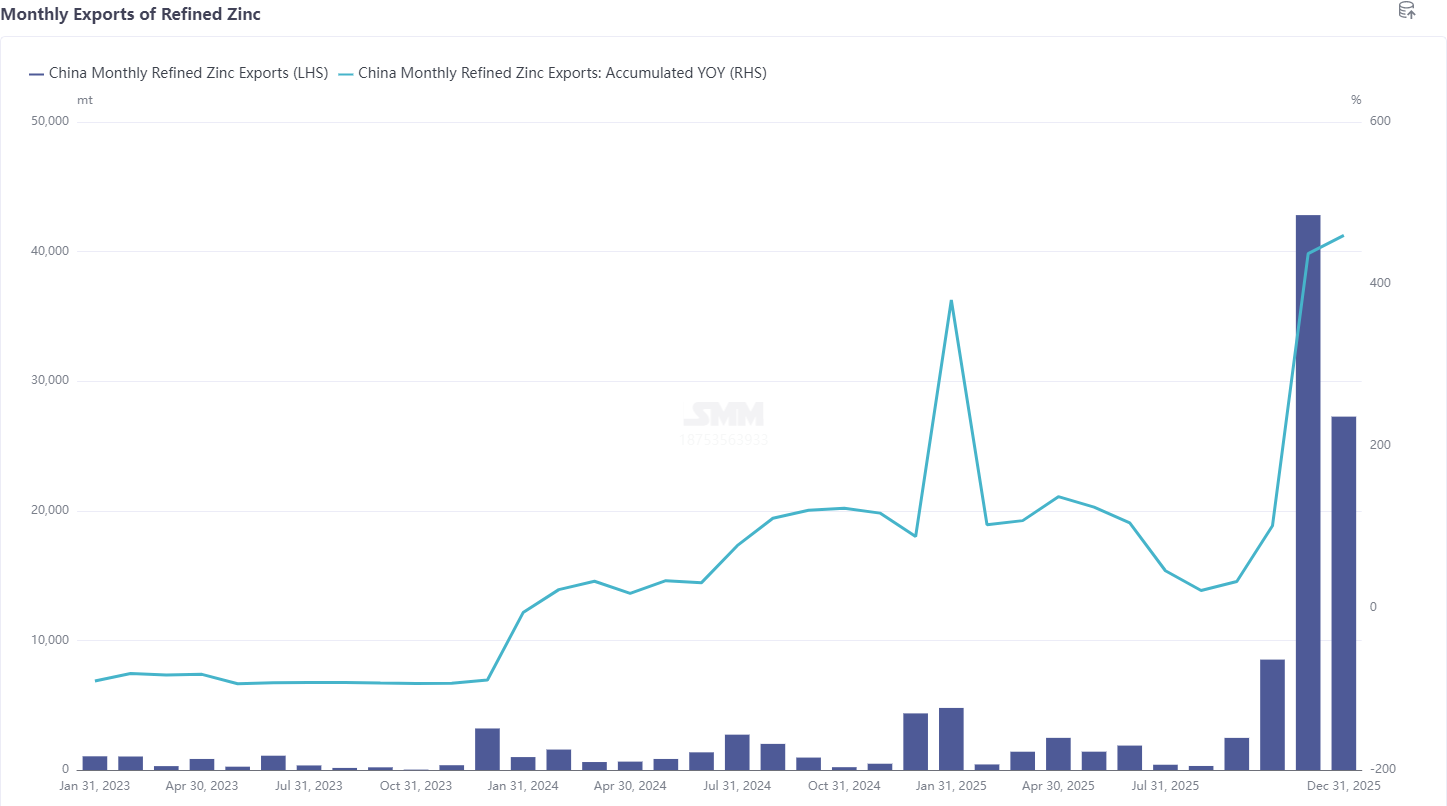

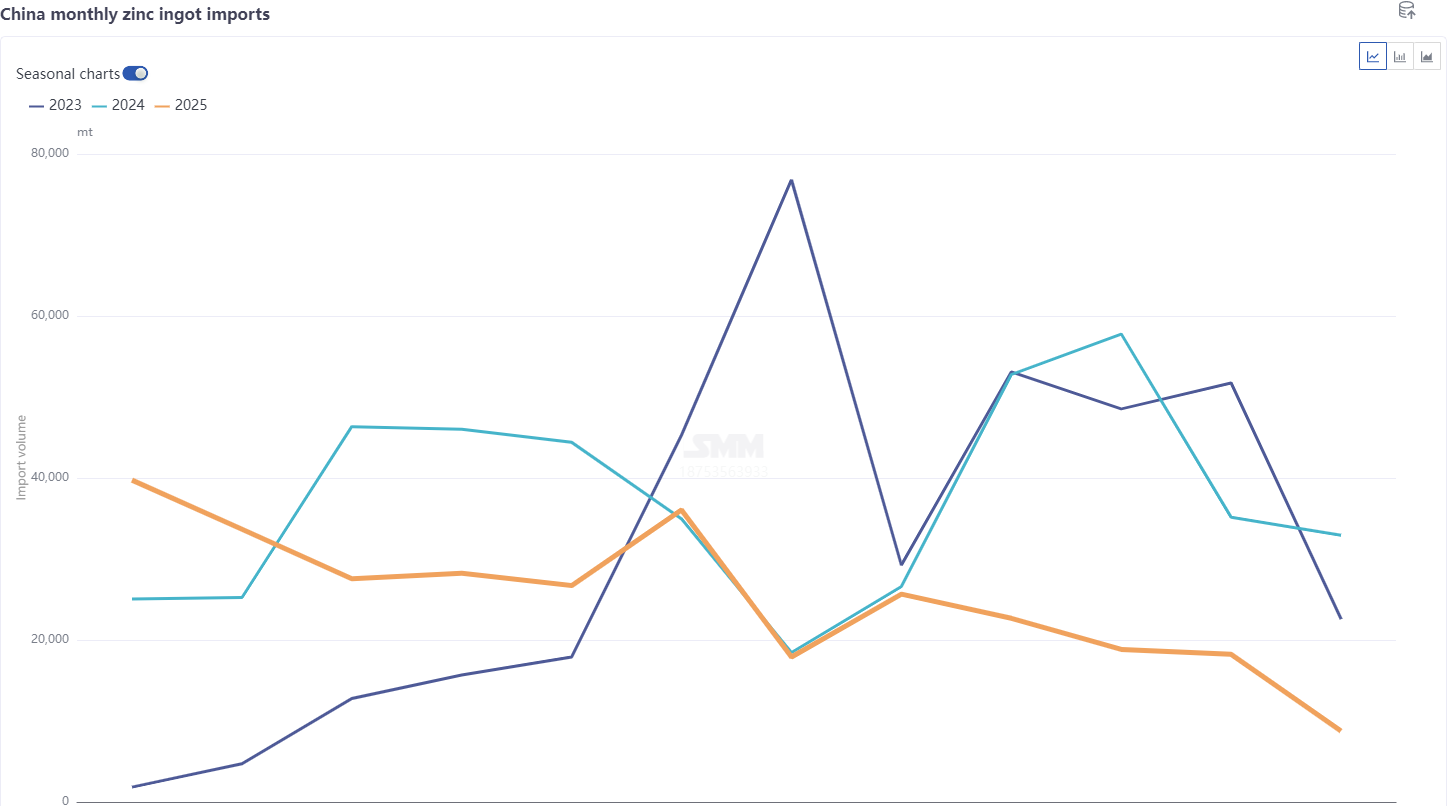

According to the latest customs data, China's refined zinc imports in December 2025 totaled 8,700 mt, down 9,500 mt or 51.94% MoM, and fell 73.4% YoY. Imports from January to December amounted to 304,000 mt, a cumulative decrease of 31.78% YoY. Exports of refined zinc in December were 27,200 mt, resulting in a net export volume of 18,500 mt for the month.

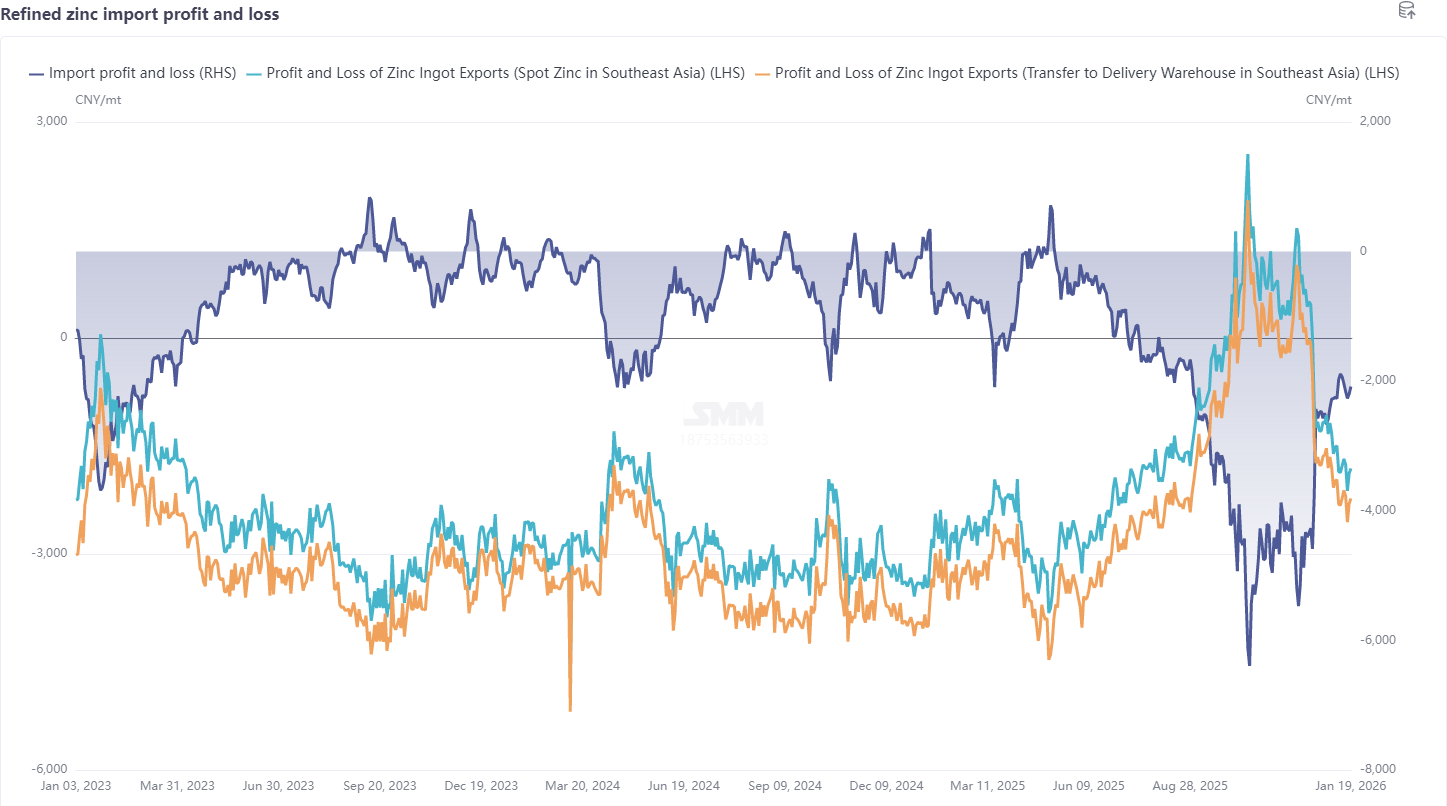

By country, the top three sources of refined zinc imports in December were Kazakhstan (6,300 mt, 72.26%), Iran (1,400 mt, 15.96%), and Australia (700 mt, 8.17%). Overall imports declined as the export window closed. Refined zinc exports remained high in December, with the top three destinations being Taiwan, China (13,500 mt, 49.37%), Singapore (3,500 mt, 12.87%), and Hong Kong, China (3,000 mt, 10.97%). Overall, as the SHFE/LME zinc price ratio adjusted, the refined zinc export window gradually closed in the middle of the month, and the import loss narrowed to around 2,500 yuan/mt.

Entering January, geopolitical instability increased, tariff disputes resurfaced, precious metals surged, and under capital rotation, base metals and ferrous metals successively hit record highs, while the stock market also exhibited "bull market" characteristics, driving zinc prices to fluctuate upward. Fundamentals side, LME Cash-3M returned to a contango structure, LME inventory increased to over 100,000 mt, and structural risks weakened. Additionally, although heavy rains occurred in Australia, South Africa, and other regions in January, there has been no impact on zinc concentrate production and transportation so far. Moreover, LME announced that it will no longer accept warrant registrations for KZ-SHG 99.995 and YP-SHG starting April 14, 2026. However, according to market feedback, KZ has resubmitted an improvement plan, and coupled with limited deliveries of South Korean zinc ingots to LME warehouses in recent years, the overall impact is relatively limited. Domestically, against the backdrop of the domestic zinc concentrate off-season, TC remained low. However, considering the opening of the zinc concentrate import window and some recovery in smelter raw material inventories, domestic TC mainly stopped falling and stabilized, while overseas TC is expected to have slight downside room. With the conclusion of smelter maintenance, January production is expected to increase slightly MoM to 569,400 mt. On the consumption side, affected by rain, snow, and haze, demand has already entered the off-season, with some enterprises starting holidays around month-end January to early February. Social inventory entered a phase of inventory buildup, and overall, supply and demand were both weak. However, from the perspective of macro sentiment and capital enthusiasm, domestic performance was stronger than overseas, with the domestic-to-overseas ratio remaining high, though not sufficient to open the import window. Overall, both imports and exports were closed, and January refined zinc exports are expected to decrease significantly, with imports mainly under long-term contracts, returning refined zinc to a net import status.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM's internal database model, for reference only and do not constitute decision-making advice.