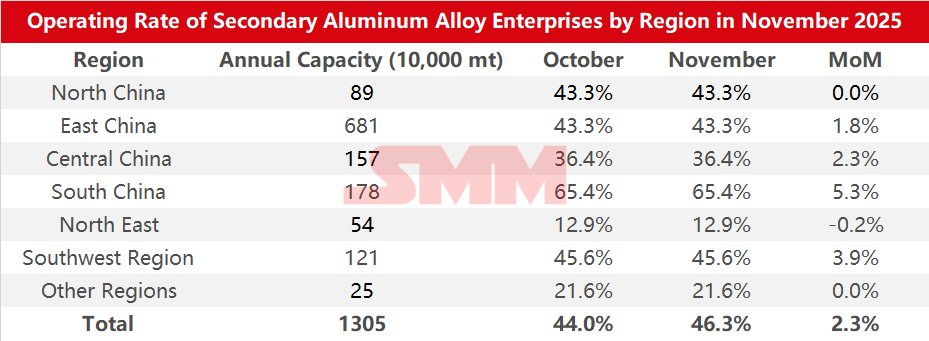

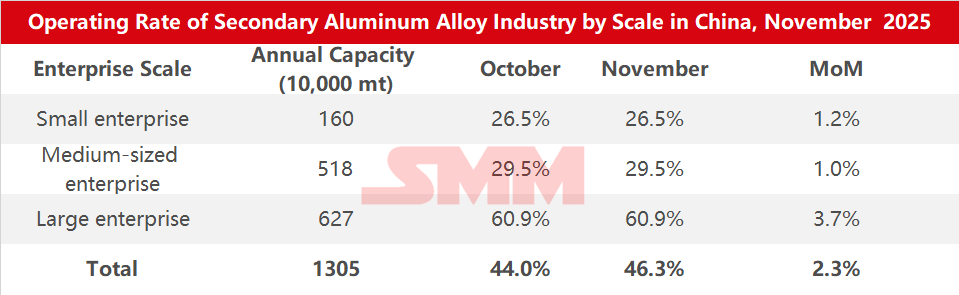

Survey Data on Operating Rates of Secondary Aluminum Alloy Enterprises by Region and Scale in November 2025:

According to SMM survey statistics, the operating rate of the secondary aluminum industry in November 2025 rose 2.3 percentage points MoM to 46.3%, up 2.7 percentage points YoY.

The drivers for the increase in the operating rate in November included:

1. Seasonal production recovery: The disruption from the holidays subsided, and after the Double Festival holidays, domestic secondary aluminum enterprises gradually resumed normal production pace.

2. Structural recovery in end-use demand: Particularly, top-tier enterprises, mainly driven by automotive orders, accelerated capacity release, effectively boosting the overall industry operating level.

However, the release of industry capacity still faces multiple practical constraints, resulting in the increase in the operating rate falling short of market expectations. On one hand, raw material-side pressure remains high, the tight supply situation in the aluminum scrap market has not eased, and coupled with raw material prices fluctuating at highs, enterprise procurement costs remain elevated. Some small and medium-sized secondary aluminum enterprises, constrained by raw material shortages, find it difficult to further expand capacity. On the other hand, policy uncertainties in regions such as Jiangxi and Henan suppress enterprise production enthusiasm, leading some local secondary aluminum enterprises to maintain cautious operations, such as remaining idle or implementing production cuts.

In December, relatively stable demand will continue to support the industry operating rate at a relatively high level. However, factors such as decreased winter dismantling volume and reduced import resources may lead to persistently tight aluminum scrap supply, leaving limited room for further growth in raw material inventory. Additionally, high aluminum scrap costs, combined with significant price increases for copper auxiliary materials (recent copper prices broke through 92,000 yuan/mt and repeatedly hit new highs), keep the comprehensive cost of secondary aluminum alloy under pressure. Meanwhile, potential risks of losses, expectations of regional environmental protection-driven production restrictions, and uncertainties in tax policies may further constrain capacity release. Overall, the industry operating rate in December is expected to drop back slightly from highs.