The average price of SMM 10-12% high-grade NPI fell WoW by 11.5 yuan/mtu to 885.3 yuan/mtu (ex-factory, tax included), while the average Indonesia NPI FOB index price dropped WoW by $1.04/mtu to $109.84/mtu. During the traditional off-season, some procurement demand was released driven by mainstream steel mills, but end-use consumption showed little sign of recovery, and market confidence remained weak, dragging high-grade NPI prices to a five-year low.

Supply side, current high-grade NPI prices have reached the cash cost of Indonesian smelters, upstream iron plants still refrain from offering quotes, showing clear intentions to hold prices firm, with only some spot transactions by traders in the market. Demand side, affected by the off-season, end-use consumption remains sluggish; downstream stainless steel mills have gradually released procurement demand following the announcement of mainstream tender prices, but market demand remains relatively weak. Overall, market activity has improved under the guidance of mainstream steel mill offers. Although high-grade NPI prices are still suppressed by off-season consumption, the decline is expected to slow down.

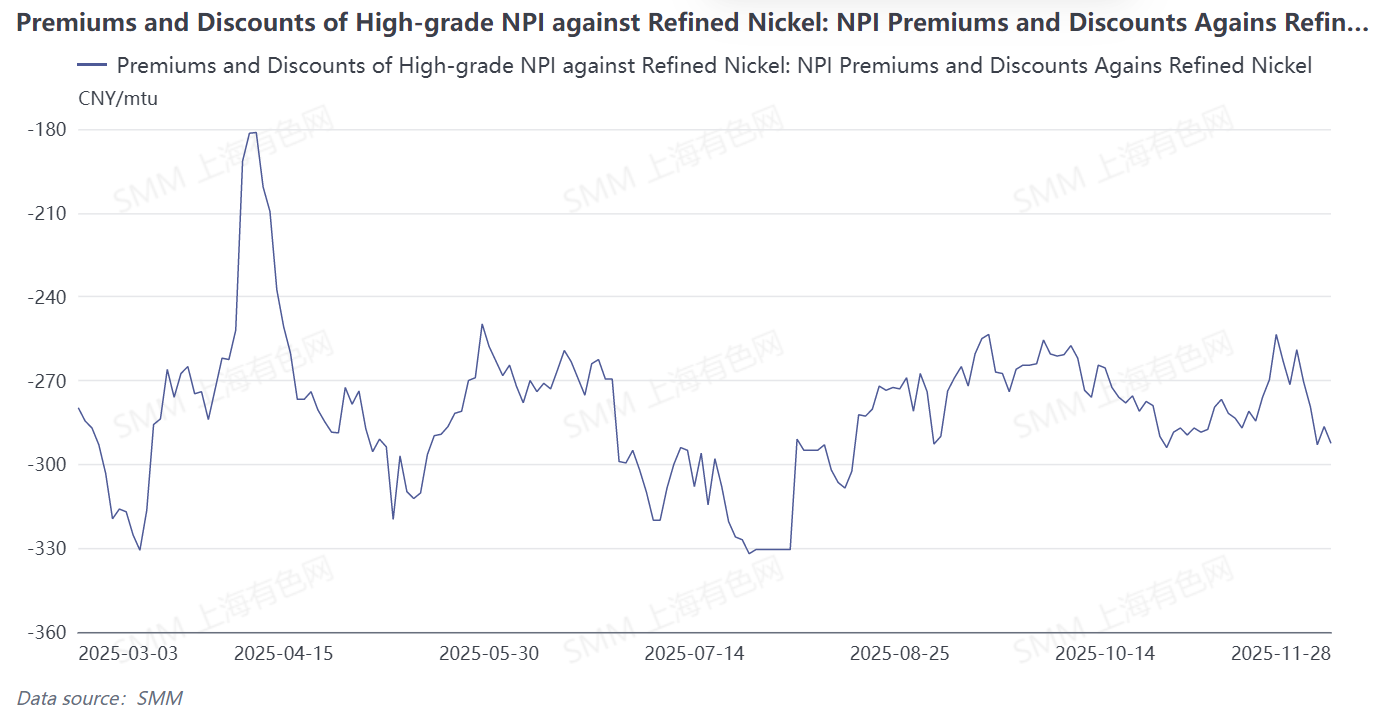

From the perspective of NPI conversion to high-grade nickel matte, the average price of refined nickel increased this week, while high-grade NPI prices continued to decline, widening the average discount of high-grade NPI to refined nickel to 284.4 yuan/mt. High-grade NPI prices are expected to remain in the doldrums next week, refined nickel prices are projected to fall again, and the average discount of high-grade NPI to refined nickel may narrow slightly. However, due to the drag on NPI sales profitability, the volume of NPI conversion is expected to increase somewhat.

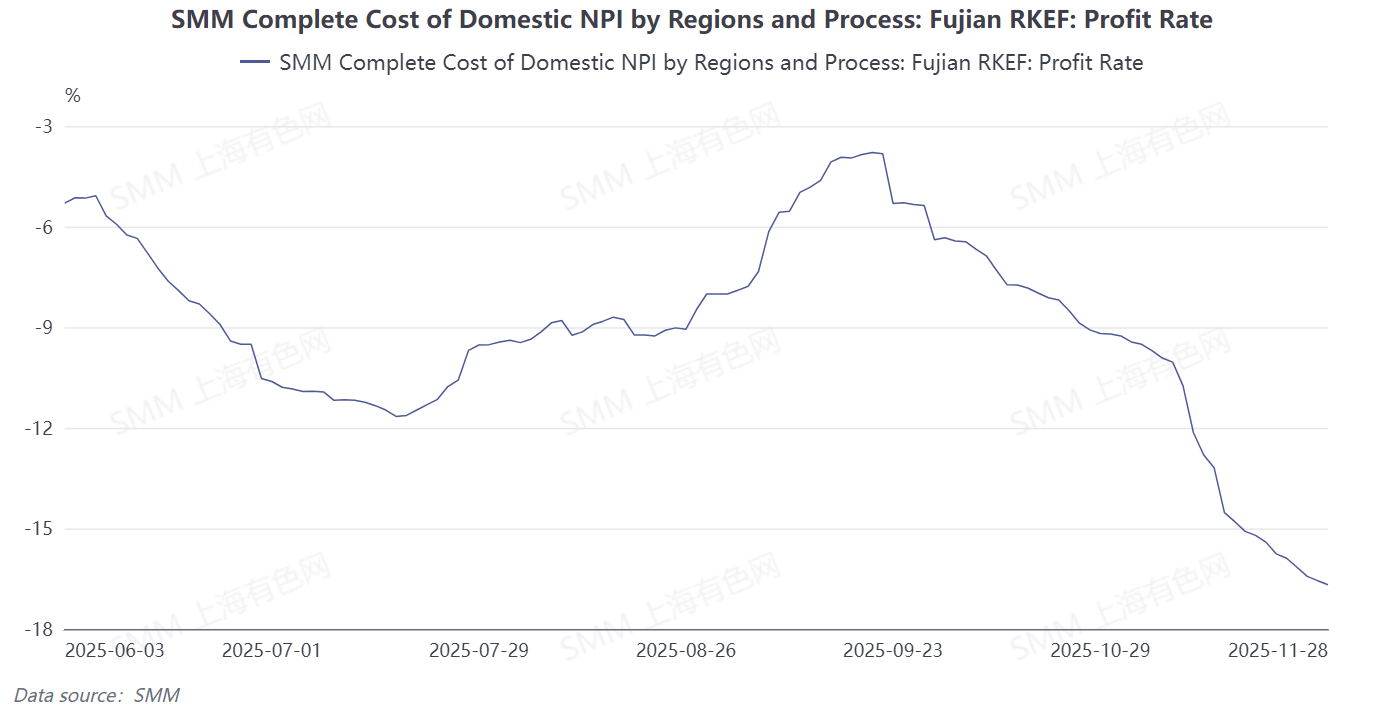

Cost side, high-grade NPI smelter margins continued to decline this week, based on nickel ore prices from 25 days ago for cash cost calculation. Raw material side, ore prices from the Philippines and Indonesia held steady during the week, while auxiliary material prices also remained flat, keeping high-grade NPI production costs firm. Meanwhile, as high-grade NPI prices continued to trend lower, smelter margins remained under pressure. Looking ahead to next week, raw material side, ore prices are expected to hold steady, while auxiliary material prices may drop back slightly. With production costs edging down, high-grade NPI prices are expected to remain in the doldrums, and smelter margins are likely to continue being dragged down.