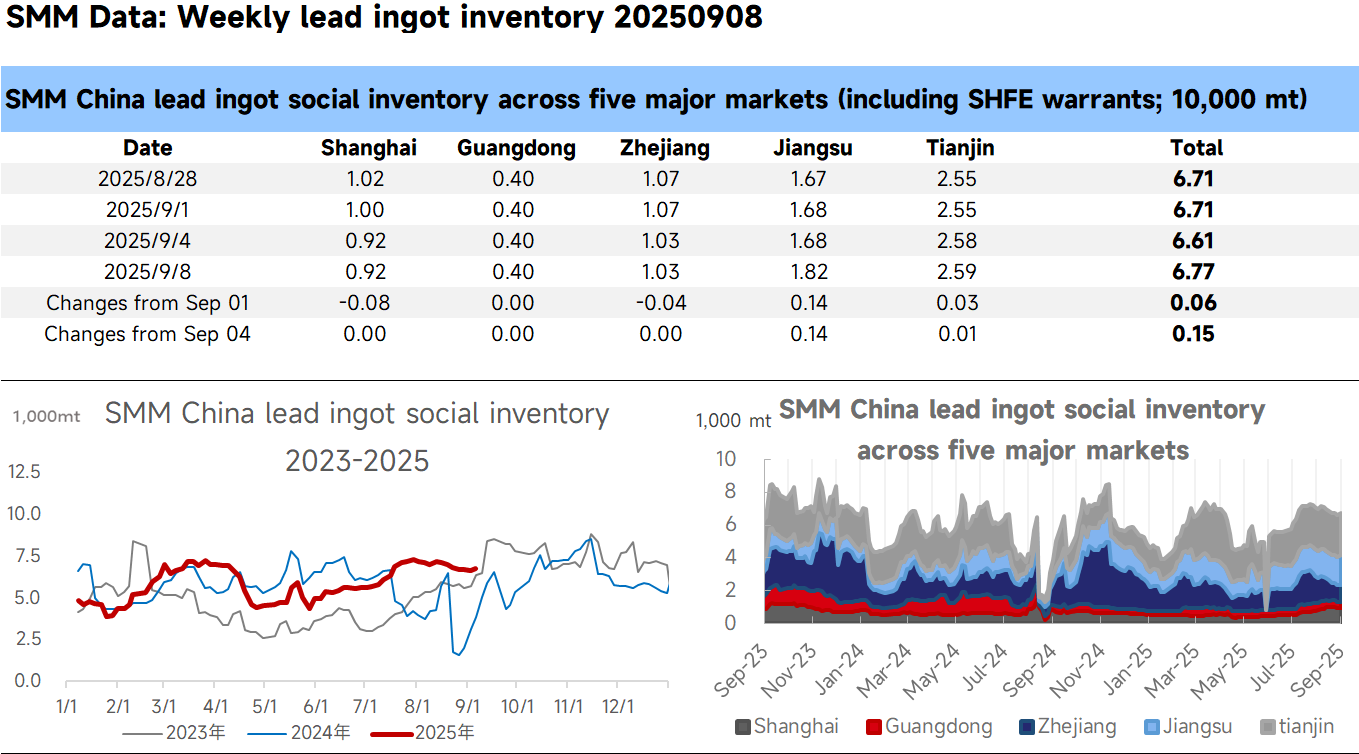

This week, logistics restrictions in North and Central China were fully lifted. On one hand, spot market cargo availability increased, with spot discounts widening—particularly for cargoes self-picked up from production sites in South China, where discounts against the SHFE lead 2510 contract once reached 200-180 yuan/mt ex-works. On the other hand, lead consumption remained weak, with downstream enterprises making just-in-time procurement sporadically, diverting some primary lead from producers' warehouses to social warehouses. Consequently, lead ingot social inventory shifted to a buildup trend. Additionally, this week marked the penultimate week before the SHFE lead 2510 contract delivery, and suppliers' subsequent transfer-to-warehouse activities may sustain the inventory increase.

Data Source Statement: Except for publicly available information, other data are derived from public sources, market exchanges, and SMM's internal database models, processed by SMM for reference only and not as decision-making advice.