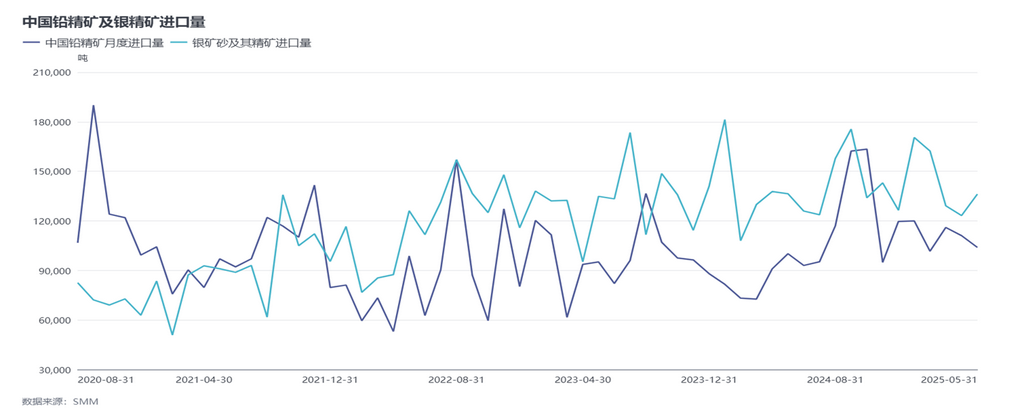

According to customs data, lead concentrate imports in May 2025 were approximately 104,000 mt, down 6.4% MoM but up 3.8% YoY. The cumulative imports for 2025 reached approximately 552,676 mt, marking a 64% increase YoY compared to 2024.

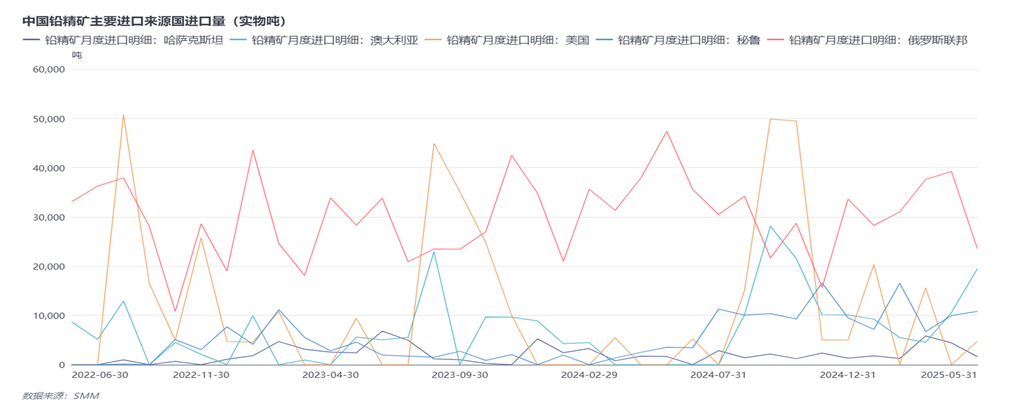

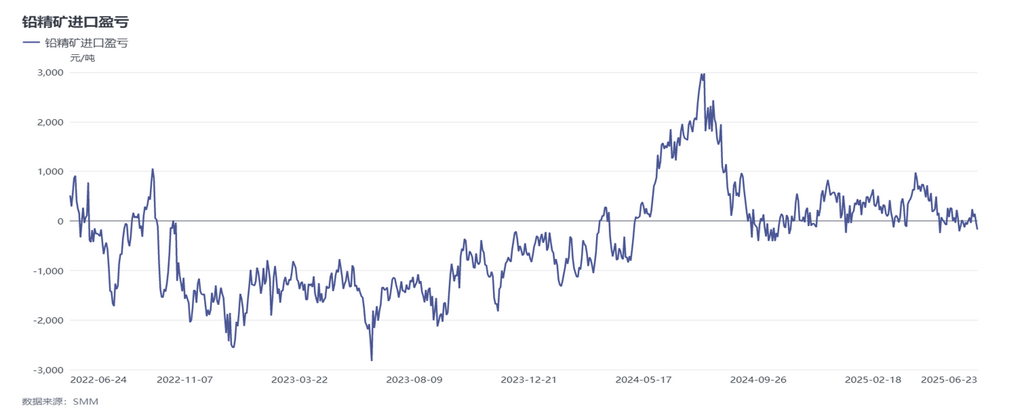

From the perspective of import profit margins, lead concentrate imports in May remained in a state of minor losses, with the import window yet to open. Additionally, in Q1, the supply of lead concentrates from regions such as Australia declined. Coupled with widespread market concerns about the prices of US Red Dog lead concentrates following the tariff hike in Q3, this led to a further decline in tender and bid quotes for lead concentrate TCs. Currently, imported lead concentrates still primarily rely on the trade market or long-term orders from smelters arriving at ports.

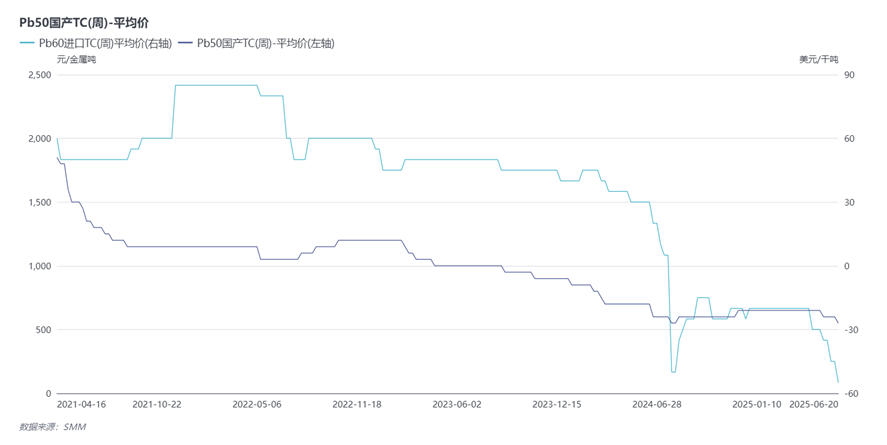

Despite lead concentrate imports increasing by over 60% YoY, silver prices continued to reach new highs in 2025, expanding the domestic and international arbitrage space and encouraging smelters to actively operate to achieve higher by-product revenues and export profits. Domestic lead concentrate supply remained relatively stable. However, due to factors such as lower-than-expected imported ore supply and scarcity of high-grade ore, lead concentrate TCs fell again in June. According to smelters, the current quotes for lead concentrates (pb50TC) with silver content ranging from 1.5-2 kg/mt are 0-200 yuan/mt (metal content), with additional silver refining fees or coefficient pricing still needing to be paid based on market conditions. Looking ahead to H2 2025, the outlook for lead concentrate imports remains pessimistic, and domestic lead concentrate supply is likely to continue in a state of tight balance.