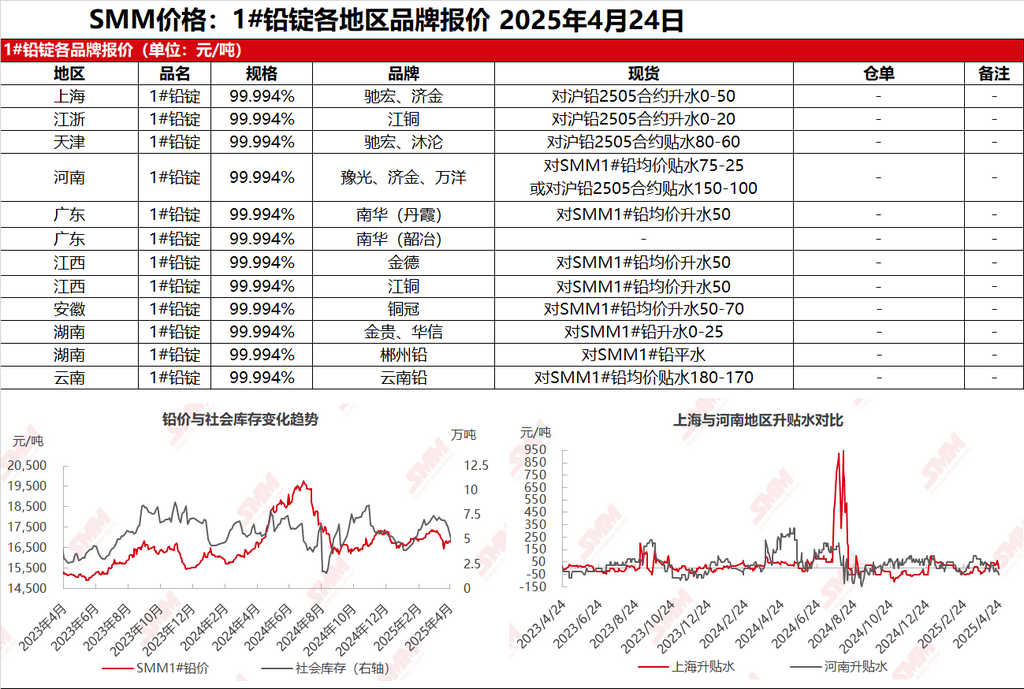

SMM April 24: In the Shanghai market, Chihong lead was quoted at 16,885-16,960 yuan/mt, with premiums of 0-50 yuan/mt against the SHFE 2505 lead contract. Jijin lead was quoted at 16,885-16,930 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE 2505 lead contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,885-16,930 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE 2505 lead contract. SHFE lead pulled back after an initial surge, but prices remained higher than during yesterday's trading session. As the month-end approached, suppliers actively quoted and sold goods, with some offering discounts. The premiums and discounts were generally lower than yesterday, especially for ex-factory primary lead smelter cargoes, which were quoted at discounts of 150-50 yuan/mt against the SHFE 2505 lead contract. In the secondary lead sector, smelters increased production cuts, reducing the supply of secondary refined lead. Mainstream quotations were at discounts of 50-0 yuan/mt against the SMM 1# lead average price ex-factory. Downstream companies maintained a purchasing-as-needed approach, with some large-discount cargoes being traded. Spot market transactions improved regionally.

Other markets: Today, the SMM 1# lead price rose by 25 yuan/mt compared to the previous trading day. In Henan, smelter quotations were at discounts of 75-25 yuan/mt against the SMM 1# lead price ex-factory, while some traders quoted discounts of 150-100 yuan/mt against the SHFE 2505 lead contract ex-factory. In Hunan, smelter quotations were at parity with the SMM 1# lead average price ex-factory, with some transactions recorded. Downstream companies continued to make just-in-time procurement, with low enthusiasm for pre-Labour Day holiday stockpiling. Spot market transactions remained weak.