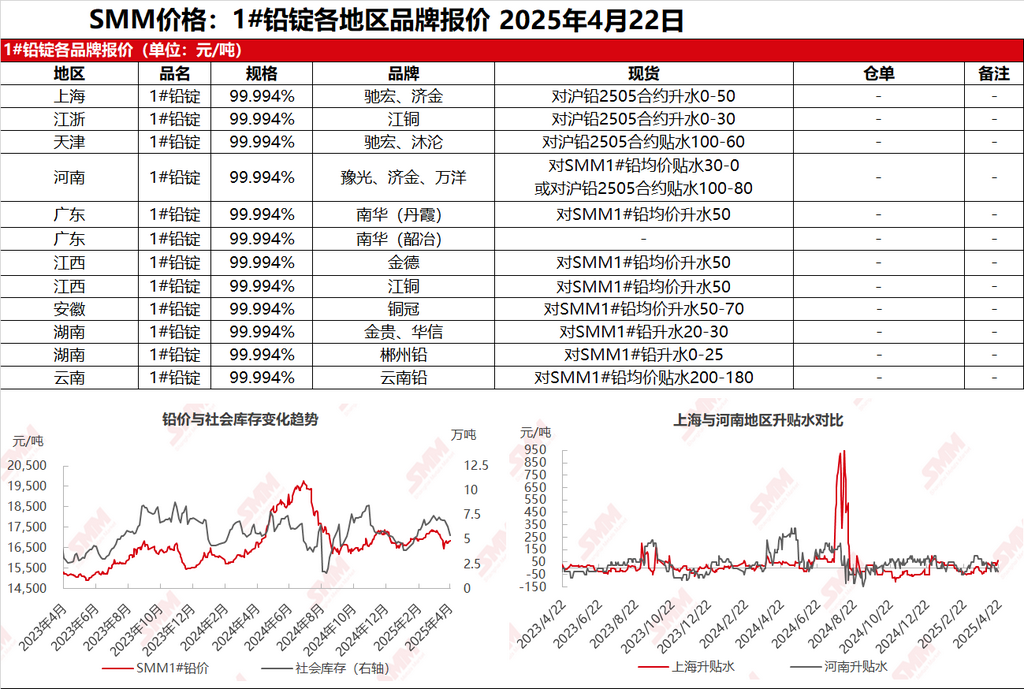

SMM April 22: In the Shanghai market, Chihong lead was quoted at 16,990-17,045 yuan/mt, with premiums of 50-80 yuan/mt against the SHFE 2505 lead contract. Jijin lead was quoted at 16,940-16,995 yuan/mt, with premiums of 0-30 yuan/mt against the SHFE 2505 lead contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 16,940-16,995 yuan/mt, with premiums of 0-30 yuan/mt against the SHFE 2505 lead contract. SHFE lead showed a high-level consolidation trend, with suppliers actively quoting and selling. Warehouse cargo quotations saw a decrease in premiums, while ex-factory quotations for primary lead from smelters in some regions expanded their discounts against the SHFE 2505 lead contract. Downstream enterprises maintained purchasing as needed, with low enthusiasm for inquiries, and some rigid demand shifted to low-priced secondary lead sources.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, smelters mainly focused on shipments under long-term contracts. At month-end, suppliers actively quoted and sold, with primary lead quotations at discounts of 30-0 yuan/mt ex-factory against the SMM 1# lead price. In Hunan, smelters quoted premiums of 0-30 yuan/mt ex-factory against the SMM 1# lead average price, with some suppliers quoting at parity against the SMM 1# lead price. The lead price rise slowed, with smelters and traders actively quoting and selling, some continuing to quote premiums against the SMM 1# lead average price. However, downstream purchases were scattered, and actual spot transaction premiums were difficult to achieve, with a tendency towards discounts.