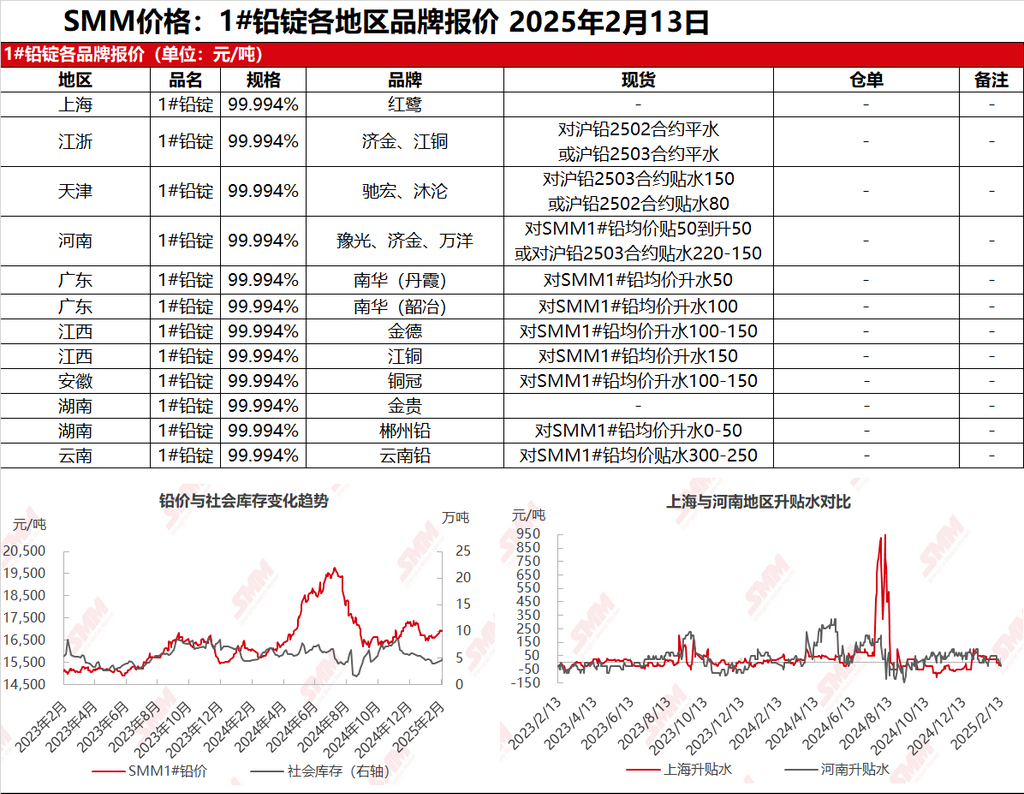

SMM reported on February 13: Quotations in the Shanghai market were scarce; in Jiangsu and Zhejiang regions, JCC and Jijin lead were quoted at 17,080-17,140 yuan/mt, either on parity with the SHFE 2502 contract or on parity with the SHFE 2503 contract. SHFE lead remained in a high-level consolidation trend, and suppliers actively shipped goods. Some quotations saw expanded discounts again, mainly for cargoes self-picked up from production sites by smelters, quoted at discounts of 50 yuan/mt to premiums of 50 yuan/mt against the SMM 1# lead average price on an ex-factory basis, with premiums in South China further reduced. In the secondary lead market, smelters shipped goods in line with market trends, and secondary refined lead was quoted at discounts of 120-50 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Downstream enterprises gradually inquired and negotiated prices, with some significant differences in price negotiations, leading to relatively improved market activity.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, suppliers quoted discounts of 180-200 yuan/mt against the SHFE 2403 contract, with downstream buyers actively negotiating prices. Some trades were concluded at discounts of 50-0 yuan/mt. In Hunan, smelters quoted premiums of 0-50 yuan/mt, while in Guangdong, premiums were further reduced after supply recovery. In Yunnan, discounts remained at 300-200 yuan/mt, with declines still dominated by long-term contract cargo pick-up. Cautious sentiment prevailed, with most buyers hesitant to purchase due to fears of price drops, and spot order transactions were generally sluggish.