》View SMM Copper Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Copper Industry Chain Database

SMM, January 24:

In terms of macroeconomics, earlier this week, Trump officially took the oath of office. His initial tariff policy decisions temporarily eased market sentiment. Although concerns about subsequent uncertainties remain, his current mild statements have alleviated fears of a new round of trade wars. The US dollar index declined in the short term, driving copper prices higher. Meanwhile, the US Fed is highly likely to maintain its current stance during the January FOMC meeting, and the strong US dollar trend may persist in the short term. High US Treasury yields have exerted pressure on equity assets. Despite marginal cooling in inflation, the risk of an inflation rebound remains, leading to a cautious market sentiment. The European Central Bank plans to continue interest rate cuts. Uncertainties in inflation and growth, particularly potential trade frictions triggered by Trump's administration, pose potential risks to the Eurozone economy. In Japan, the Bank of Japan plans to raise its policy rate by 25 basis points to 0.5% this Friday. A weaker yen has contributed to inflation stickiness. Overall, international interest rate differentials continue to narrow. This week, the center of commodities shifted upward, with LME copper rising from $9,150/mt to around $9,300/mt. In China, the continued expansion of domestic demand alongside counter-cyclical adjustment policies has led to a stable and improving fundamental trend. SHFE copper rose from 75,000 yuan/mt to around 75,700 yuan/mt during the week, with relatively small fluctuations overall.

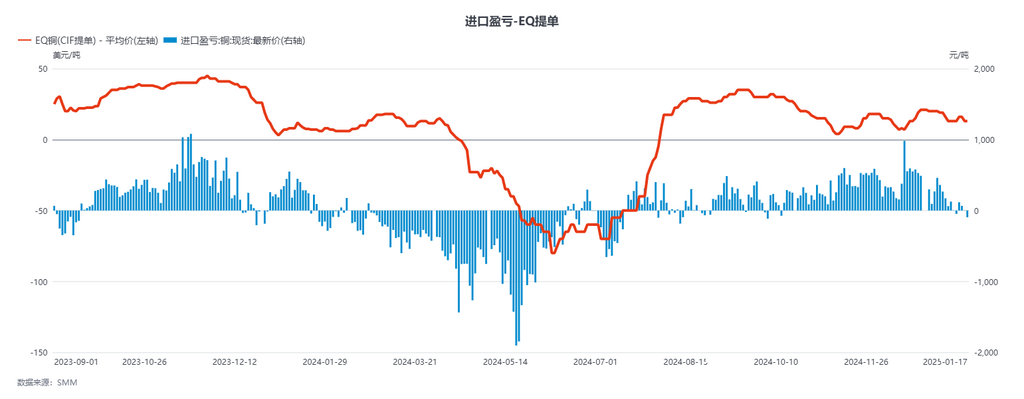

In terms of foreign trade, this week, the import arbitrage window closed as earlier exchange rate fluctuations gradually leveled off. However, the price spread between the Comex most-traded contract and the LME 0-3M contract remained high. Since this price spread is not caused by inventory factors, the import arbitrage window for US dollar-denominated copper remained tightly closed. Suppliers shifted their offers to cargoes arriving in later months, but due to the slow pace of long-term contract declarations and the approach of the Lunar New Year, the actual market activity was subdued. Regarding EQ, there were sporadic offers for cargoes arriving in mid-to-late February, but actual transactions were significantly impacted by the worsening SHFE/LME price ratio. Additionally, according to SMM, some major traders have already redirected shipments to North America, with an estimated volume in transit of 20,000 mt.

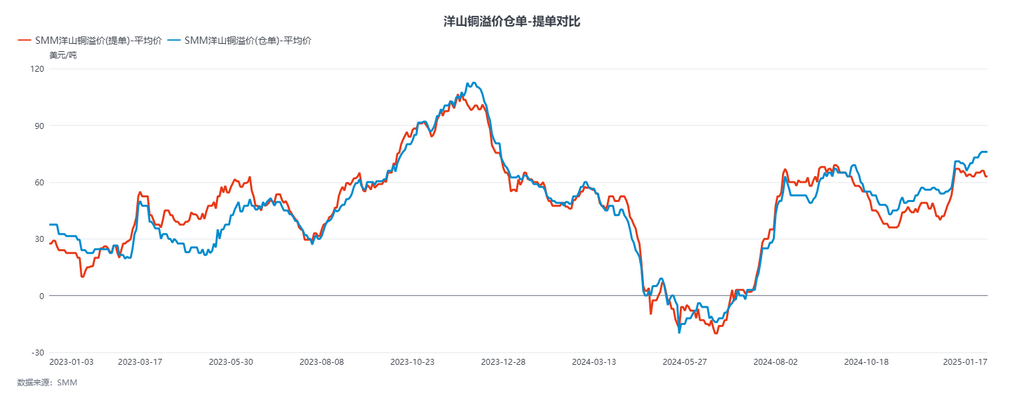

In the domestic market, since January, the high spot premiums in domestic trade have eased. After the delivery of the SHFE copper 2401 contract, spot premiums pulled back slightly, and the rise in copper prices dampened some downstream pre-holiday restocking sentiment. Overall, domestic consumption has slowed this year, as logistics are halting and enterprise orders remain weak.

Looking ahead to next week, the US Fed is highly likely to maintain its current stance during the January FOMC meeting. However, under the pressure of the Trump administration's eagerness for interest rate cuts, the US dollar index still has downside room. The European Central Bank's interest rate cut is almost certain, providing strong short-term support for copper prices. LME copper is expected to fluctuate within the range of $9,250-9,350/mt, while SHFE copper, with only one trading day next week due to the Lunar New Year holiday, is expected to see the most-traded contract fluctuate within the range of 75,500-76,500 yuan/mt. In the spot market, next week is expected to see minimal spot transactions, with almost no market circulation. Spot prices against the SHFE copper 2502 contract are expected to remain in the range of a discount of 100 yuan/mt to a discount of 50 yuan/mt.