Weekly Review

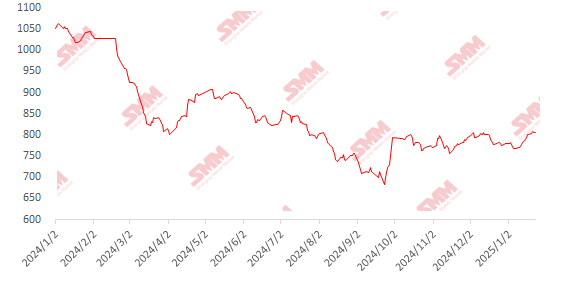

This week, imported iron ore prices fluctuated rangebound. Macro side, at the beginning of the week, US President Trump signed 40 executive orders on his first day in office, but none addressed the steel export tariff issue that the market was concerned about. Additionally, the easing of US-China relations alleviated short-term market concerns, boosting optimistic market sentiment. Fundamentals side, heavy rainfall significantly reduced Rio Tinto's shipments, leading to a 6.7% WoW decline in global shipments, which remained at a seasonal low. Port arrivals also decreased, easing supply pressure on iron ore. Demand side, the resumption of blast furnaces at steel mills drove a continuous increase in pig iron production. Meanwhile, pre-holiday restocking by steel mills was not yet completed, providing support for spot prices. As a result, iron ore prices fluctuated upward this week. At port prices, PB fines in Shandong rose by 5-10 yuan/mt WoW.

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

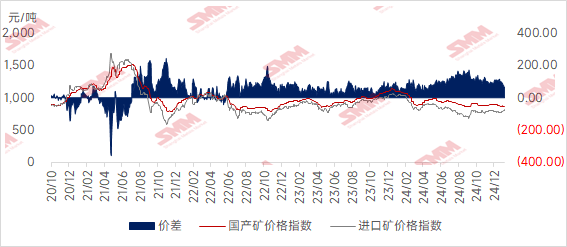

Domestic Ore Prices Showed Mixed Performance This Week; Domestic Ore Prices Are Expected to Have Some Upward Potential Next Week

Domestic Ore Prices Showed Mixed Performance This Week; Domestic Ore Prices Are Expected to Remain Stable with a Weak Trend Next Week. Specifically,prices in Tangshan, Qian'an, and Qianxi in Hebei fell by 5-10 yuan/mt; prices in west Liaoning, Chaoyang, Beipiao, and Jianping decreased by 1-5 yuan/mt; prices in east China increased by 30-40 yuan/mt.

Tangshan MarketThe market continued to fluctuate downward, with local leading steel mills largely completing their restocking of domestic iron ore concentrates, maintaining a strong desire to bargain down prices. Some producers, concerned about the market outlook, focused on selling. Mines and beneficiation plants side, as the Chinese New Year approaches, overall willingness to sell was moderate due to cash flow considerations, making it difficult for current market prices to gain support. Coupled with the recent high-level fluctuations in iron ore futures, local iron ore concentrate prices are expected to fluctuate downward in the short term.

West Liaoning MarketDomestic Oremaintained a relatively stable trend. As the holiday approaches, beneficiation plants in various regions have gradually stopped production and taken holidays. Operating beneficiation plants held firm on their asking prices, while a few traders with stockpiling needs were cautious in inquiries, leading to relatively low prices. The tight supply situation provided some support for local iron ore concentrate prices. Steel mills side, pre-holiday restocking was largely completed, and considering the impact of current steel mill profits, the overall desire to bargain down prices remained strong. The market was in a short-term state of weak supply and demand. Considering the recent high-level fluctuations in iron ore futures, local iron ore concentrate prices are expected to remain stable in the short term.

East China RegionMines and beneficiation plants side, production was mostly normal, with sales matching production and no significant inventory pressure. From a pricing perspective, the average price index of imported ore rose slightly WoW, and local iron ore concentrate prices are expected to have some upward potential in the short term.

Considering both domestic and imported ore prices, imported ore prices rose more significantly than domestic ore prices this week, narrowing the price spread between domestic and imported ore. The price spread is expected to remain stable next week.

Outlook for Next Week

Imported Ore:Affected by the rainy season in the Southern Hemisphere, global shipments are expected to remain at low levels, although port arrivals may see a slight increase. Demand side, as the Chinese New Year approaches, most steel mills are maintaining current production levels, with limited increases in pig iron production. Meanwhile, as pre-holiday restocking has been completed, spot transactions are slowing, leading to minimal price fluctuations. Post-holiday, attention should be paid to pressure in industry chain data and the pace of downstream demand recovery. Overall, the current industry imbalance is relatively small, and the macro environment is mild. Iron ore prices are expected to continue fluctuating upward next week and in the first week after the holiday.

Domestic Ore:Recently, the cost-effectiveness of domestic ore has improved, but as steel mills have gradually completed stockpiling, demand has declined, and the overall desire to bargain down prices remains strong. Domestic iron ore concentrate prices are expected to fluctuate downward with a weak trend overall.

Click to View the SMM Metal Industry Chain Database