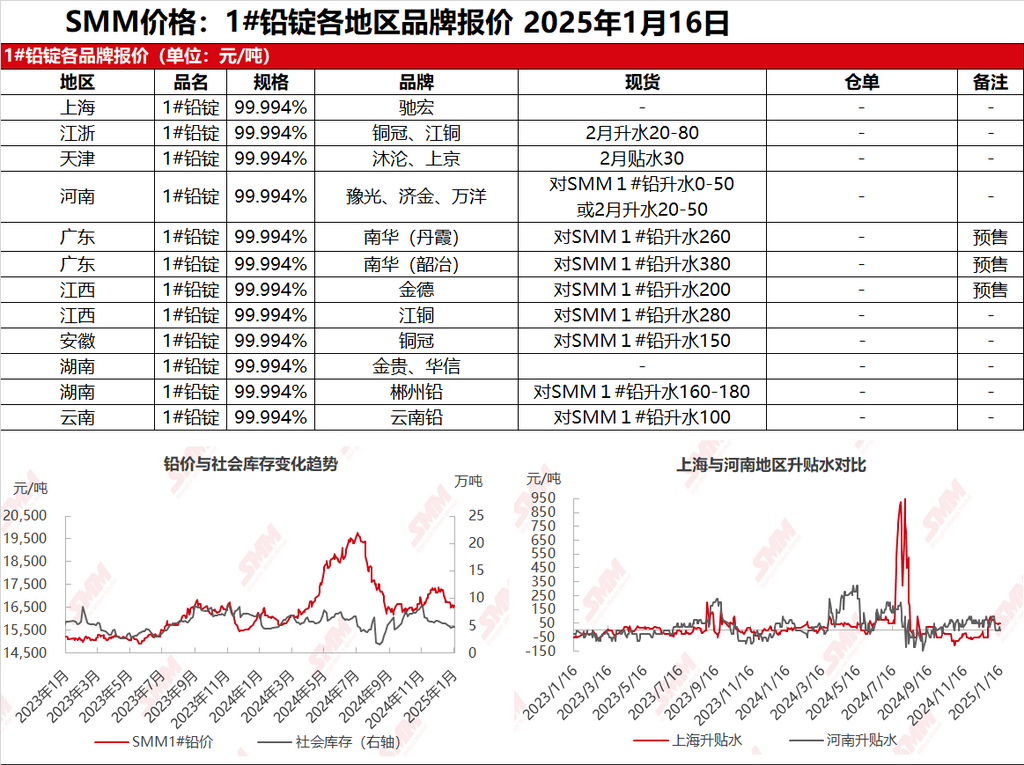

SMM, January 16: Quotations in the Shanghai market were scarce; in Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 16,600-16,660 yuan/mt, with a premium of 20-80 yuan/mt against the SHFE lead 2502 contract. SHFE lead remained range-bound, and suppliers were eager to clear inventory before the holiday, actively quoting for sales. However, due to the limited availability of warehouse warrant cargoes, quotations were scarce, with transactions mainly involving cargoes self-picked up from production sites. Meanwhile, secondary smelters were also actively selling, with secondary refined lead quoted at a discount of 50 yuan/mt to a premium of 50 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Downstream enterprises had mostly completed pre-holiday restocking, leading to weakened purchase willingness, while a small number of enterprises that had not completed restocking continued to restock, resulting in a subdued spot order market.

Other markets: Today, the SMM 1# lead price remained unchanged from the previous trading day. In Henan, transactions were mainly based on long-term contract cargo pick-up, with suppliers quoting near parity with the SMM 1# lead price. In Hunan, premiums remained at 150-200 yuan/mt, with downstream maintaining just-in-time procurement. In Jiangxi, Yunnan, Guangdong, and other regions, primary lead supply had not yet resumed, and a few smelters provided pre-sale quotations. Downstream pre-holiday just-in-time restocking was nearing completion, and transactions gradually turned sluggish.