》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Metal Spot Prices

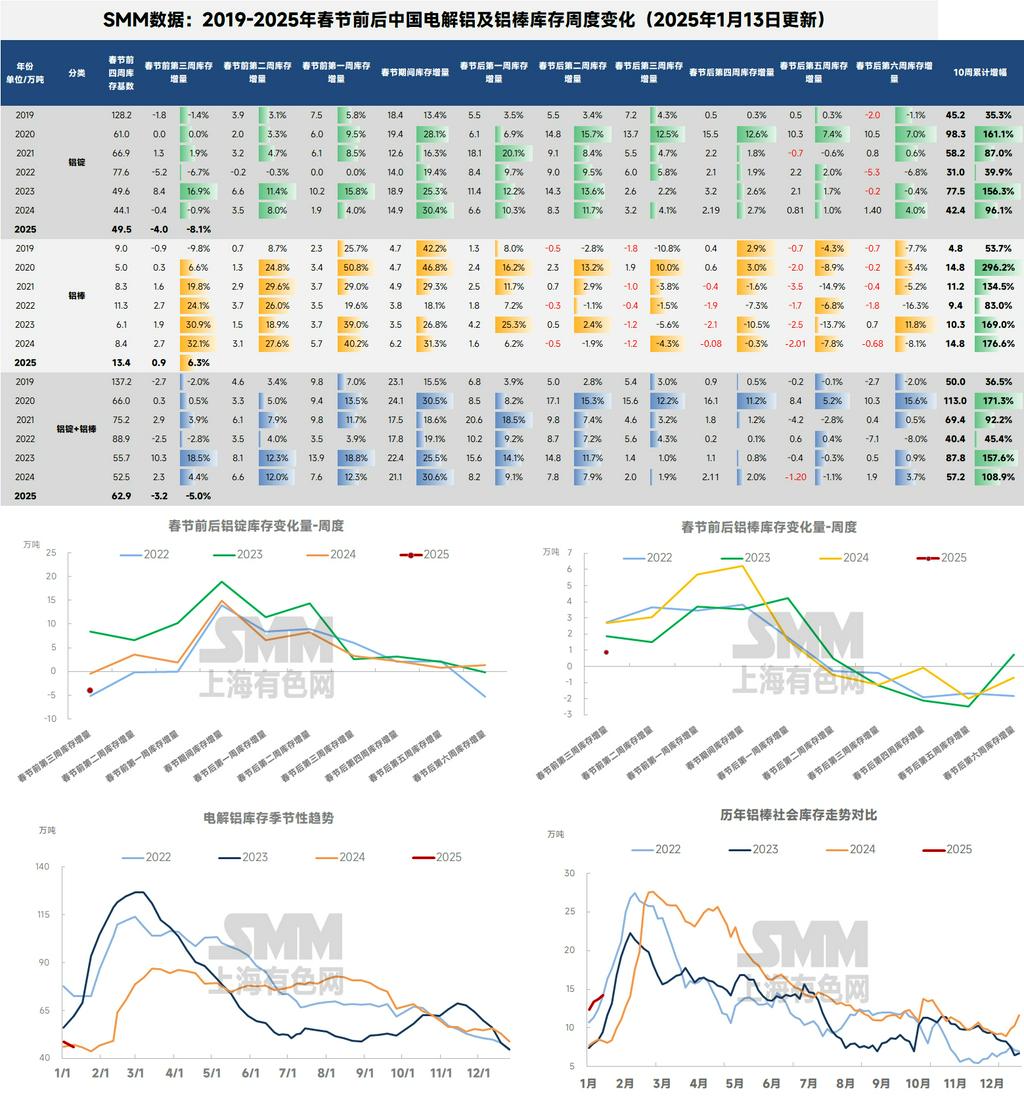

Regarding aluminum ingot inventory, since late December, transportation in Xinjiang has basically returned to normal. Apart from regular in-plant and station turnover inventory, the backlog in Xinjiang has been largely consumed. Entering January, according to SMM statistics, as of January 6, 2025, domestic social inventory of aluminum ingots was 495,000 mt, and the domestic available aluminum inventory was 369,000 mt, up 8,000 mt WoW. This marks the first inventory buildup of domestic aluminum ingots since December 9. On a YoY basis, current domestic aluminum ingot inventory is still 36,000 mt higher than the same period last year. Regarding outflows from warehouses, SMM statistics show that last week, domestic aluminum ingot outflows from warehouses fell sharply by 21,300 mt WoW to 108,600 mt. Although partially affected by the New Year holiday, as some downstream sectors have entered or are about to enter the holiday phase by year-end, the record high outflows in late December seem to have been a "flash in the pan." Over the past two weeks, aluminum ingot outflows have significantly pulled back, returning to normal off-season levels at year-end.

On the supply side of aluminum, entering January 2025, domestic operating capacity of aluminum remained stable. The negative impact of earlier production cuts on output has become evident. SMM reports that no additional production cuts are currently planned. By the end of December, the annualized operating capacity of domestic aluminum remained steady at 43.53 million mt/year. During the month, the casting ingot ratio increased in multiple regions, while the proportion of liquid aluminum decreased by 1.22 percentage points MoM and fell by 1.99 percentage points YoY. Based on SMM's liquid aluminum ratio data, the domestic aluminum casting ingot production in December increased by 8.23% YoY to approximately 1.03 million mt. As the Chinese New Year holiday approaches, downstream demand weakens, and some billet plants have cut production. The proportion of liquid aluminum is expected to further decrease to around 70% in January.

Therefore, the overall supply pressure of domestic aluminum ingots before and after the Chinese New Year cannot be ignored. Although the aluminum price correction in December exceeded expectations in driving spot outflows, the overall domestic aluminum demand remains in an off-season atmosphere. By year-end, some downstream sectors have entered or are about to enter the holiday phase. Meanwhile, aluminum prices below 20,000 yuan/mt may become the norm during the pre- and post-Chinese New Year period, and downstream purchasing interest has gradually waned, making a strong rebound in aluminum ingot outflows unlikely. Regarding arrivals, with Xinjiang's transportation having normalized for some time, concentrated arrivals are expected to peak in the next two weeks, significantly increasing pressure on the spot market and consolidating the inventory buildup turning point. SMM expects that with the initial appearance of the aluminum ingot inventory buildup turning point, domestic aluminum ingot inventory will likely enter a continuous buildup phase in January. Before the Chinese New Year, domestic aluminum ingot inventory may build up to 550,000-600,000 mt. Closely monitor changes in downstream operating rates before the year-end holiday and whether the aluminum price correction continues to drive spot outflows.

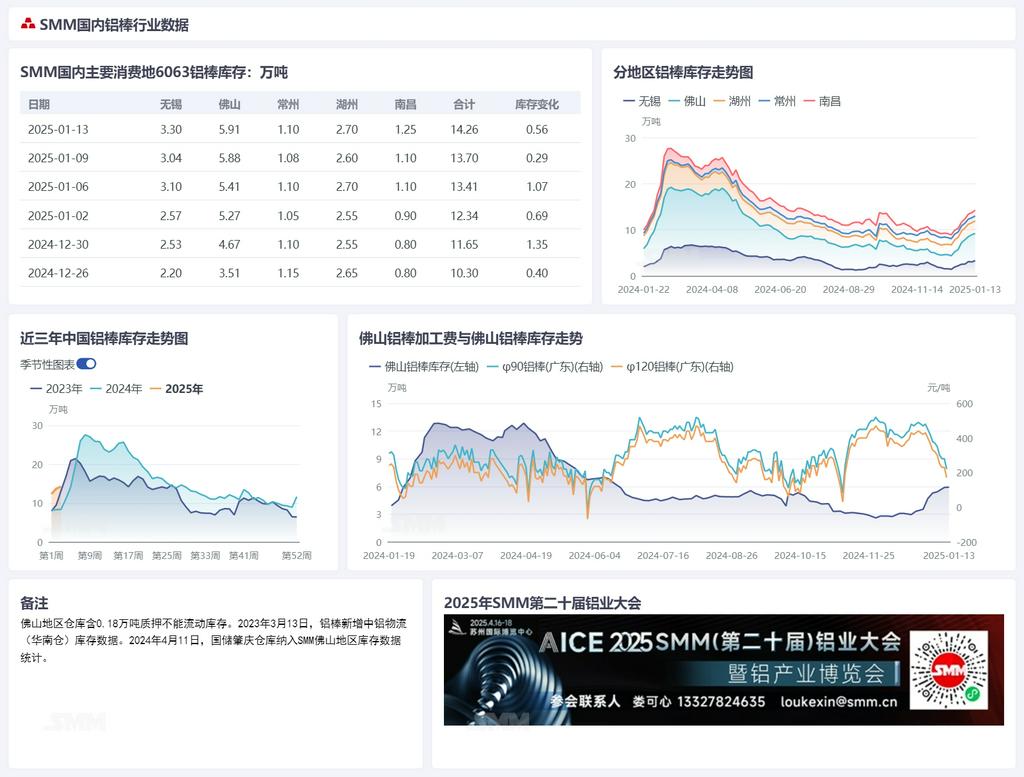

Turning to aluminum billet inventory. On the supply side, according to SMM's recently concluded December survey on primary aluminum billets, domestic primary aluminum billet production in December declined but less than expected. In December 2024 (31 days), total domestic primary aluminum billet production was 1.465 million mt, down 12,000 mt MoM, a decrease of 0.81%, but up 162,000 mt YoY, an increase of 12.4%. The domestic operating rate of primary aluminum billets in December was 56.4%, down 0.4% MoM. Entering early January, as no further reductions in domestic aluminum billet supply have been reported, arrivals remain ample. According to SMM statistics, as of January 6, domestic social inventory of aluminum billets was 134,100 mt, up 10,700 mt WoW. Since the inventory buildup turning point on December 23, domestic aluminum billet inventory has increased by over 10,000 mt weekly. On a YoY basis, the gap with the same period last year has further widened to 51,100 mt. Regarding outflows, last week, aluminum billet outflows from warehouses decreased by 6,600 mt WoW to 35,100 mt. Although affected by the New Year holiday, the subsequent performance of aluminum billet outflows is also unlikely to be optimistic. It remains at a relatively high level compared to the same period over the past three years.

Due to the earlier expansion of the Guangdong-Shanghai price spread, in addition to the regular supply from Guangxi, Guizhou, and Yunnan in south-west China, sources from Ningxia, Xinjiang, and Qinghai in northern China have also entered the South China market, causing the supply-demand pattern of aluminum billets in South China to collapse. Processing fees have rapidly declined and lack support. Consequently, concentrated arrivals were observed over the weekend in Wuxi and Nanchang, where processing fees remain relatively high, with inventory buildup of 5,300 mt and 2,000 mt, respectively. As the off-season atmosphere in the aluminum extrusion sector intensifies, aluminum extrusion operating rates remain in a downward trend, and pre-holiday stockpiling efforts are less than ideal. With downstream manufacturers entering the holiday or pre-holiday phase, the domestic aluminum billet market may face an oversupply situation. Additionally, with significant improvements in Xinjiang's transportation, there is a clear expectation of increased shipments to East and South China. As these shipments continue to arrive in concentration, SMM expects domestic aluminum billet inventory to continue building up in January, potentially reaching 180,000-200,000 mt before the Chinese New Year.

On the demand side of aluminum billets, the domestic aluminum extrusion operating rate recorded 47.0% last week, down 0.6% WoW. Specifically, the off-season atmosphere in construction extrusion has become more pronounced. Year-end rush orders for projects in south-west China in December have been mostly completed, and some leading enterprises reported fewer orders on hand, leading to a significant decline in operating rates. As the Chinese New Year holiday approaches, operating rates are expected to continue falling. For industrial extrusion, orders for automotive extrusion remain stable to positive, mainly due to ongoing downstream demand and stockpiling for the Chinese New Year, allowing related extrusion plants to secure some new orders, supporting their operating rates. In contrast, the off-season atmosphere in PV extrusion is strong, with leading enterprises experiencing a noticeable decline in operating rates. Overall, as the Chinese New Year holiday approaches, some small enterprises have announced order cutoffs and holiday plans, while medium and large enterprises continue normal production. The operating rate of the aluminum extrusion industry is expected to gradually weaken.