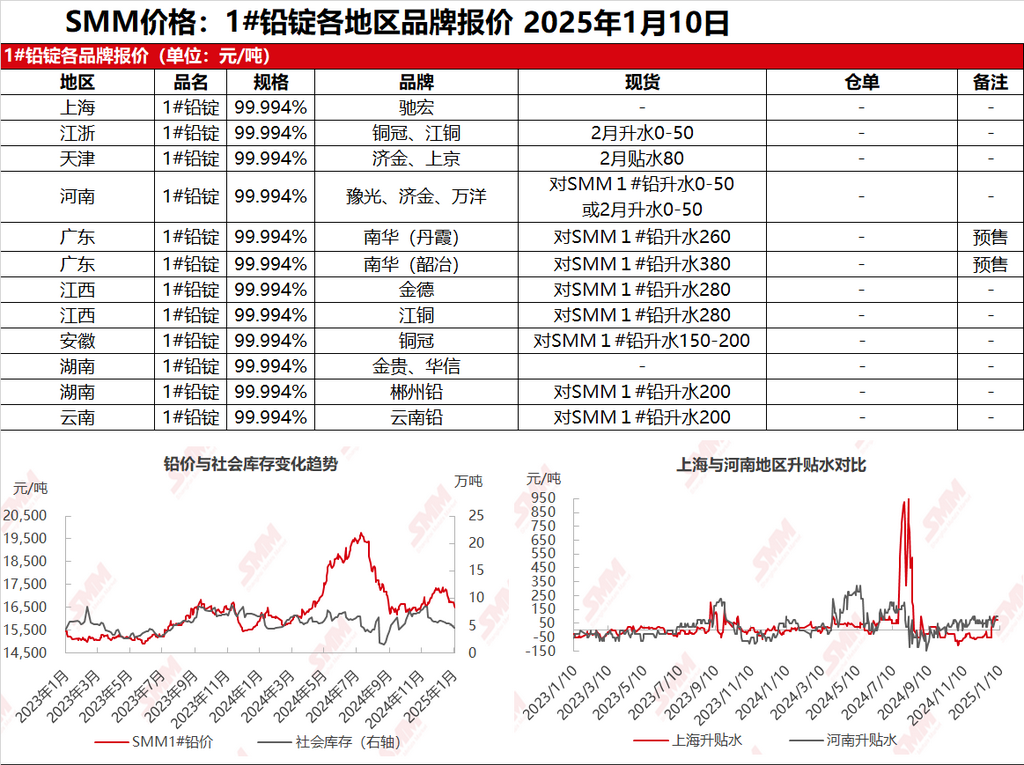

SMM reported on January 10: Quotations in the Shanghai market were scarce; in Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 16,500-16,550 yuan/mt, with premiums of 0-50 yuan/mt against the SHFE 2502 contract. SHFE lead rebounded after dipping, and suppliers quoted prices in line with the market while selling. Regional price differences for primary lead cargoes self-picked up from production sites still existed, and secondary refined lead suppliers stood firm on quotes. Quotations were at premiums of 50-100 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Downstream enterprises bought the dip as needed, with some low-priced cargoes being snapped up, leading to increased spot market trading activity.

Other markets: Today, the SMM 1# lead price dropped by 50 yuan/mt compared to the previous trading day. In Henan, suppliers quoted premiums of 0-50 yuan/mt against the SMM 1# lead average price or premiums of 0-50 yuan/mt against the SHFE 2402 contract, with moderate market transactions. In Hunan, premiums remained at 200 yuan/mt, while in Jiangxi, Yunnan, and Guangdong, primary lead supply had not recovered, maintaining high premium quotations. Downstream buyers were mostly on the sidelines, resulting in sluggish transactions.